A 20%+ Decline in the S&P is Becoming a Scenario

A 20%+ Decline in the S&P is Becoming a Scenario

Closing down 2% today off it's highs, the NASDAQ and tech stocks get the brunt of the hit

This shouldn’t be traded upon and this should be considered a scenario. A scenario that’s becoming likely based on what the Fed Minutes released today. However, markets change daily/weekly and scenarios change over time. If the Fed backs off, we will likely see an aggressive reversal.

In today’s publication, I am going to talk about the Fed Minutes and what this means for markets. It is VERY important to mention that this is not meant to be a fear provoking article but a continuation of the publication I posted back in November, before growth stocks began correcting:

It’s a macro economic first publication designed to provide something to consider when adjusting for risk in your portfolio. I encourage all investors to carefully consider the arguments presented here.

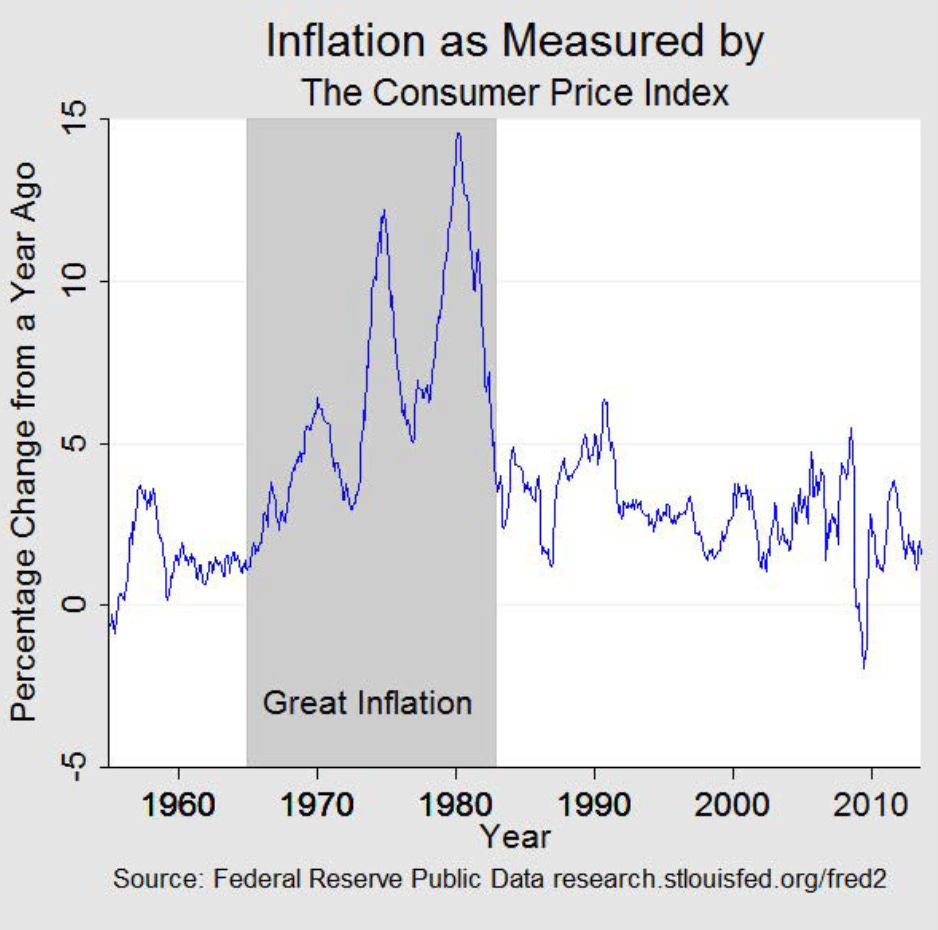

A Policy Response Similar to the 1970’s - Demand Destruction

I am going to be referencing the source above from federalreservehistory.com when talking about a period we know of as “The Great Inflation”.

In 1964, inflation was around 1% and it had been relatively low for awhile. However, through federal policy changes to “achieve maximum employment” (sound familiar?) the Federal Reserve began instituting policies that created a large expansion in money supply. Even today, many economists will debate the specifics behind why inflation started but a forgone conclusion can be attributed to the breakdown of the Bretton Wood System and Fed policy that created too much liquidity in the system.

From 1964 - 1978 there were multiple policies enacted by congress to curve hype inflation but all proved to be a failure. In turn, they were forced to make a difficult choice. In 1979, Paul Volcker took place as the chair of the Fed. He instantly rose rates when he got into office. The policy was to combat inflation at the inevitable demise of the job market. In other words, provoke a recession creating demand destruction to get inflation under control.

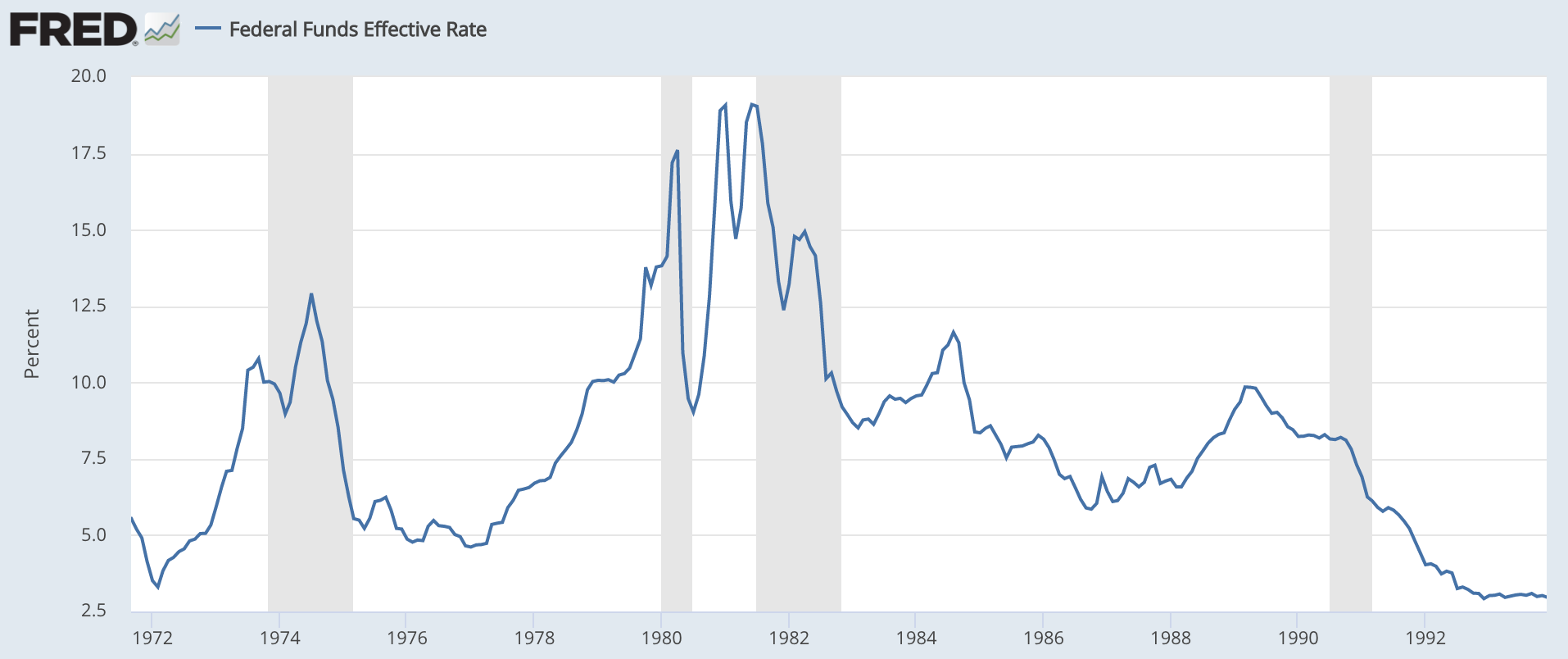

The Federal Funds Rate of the Late 1970’s, early 1980’s

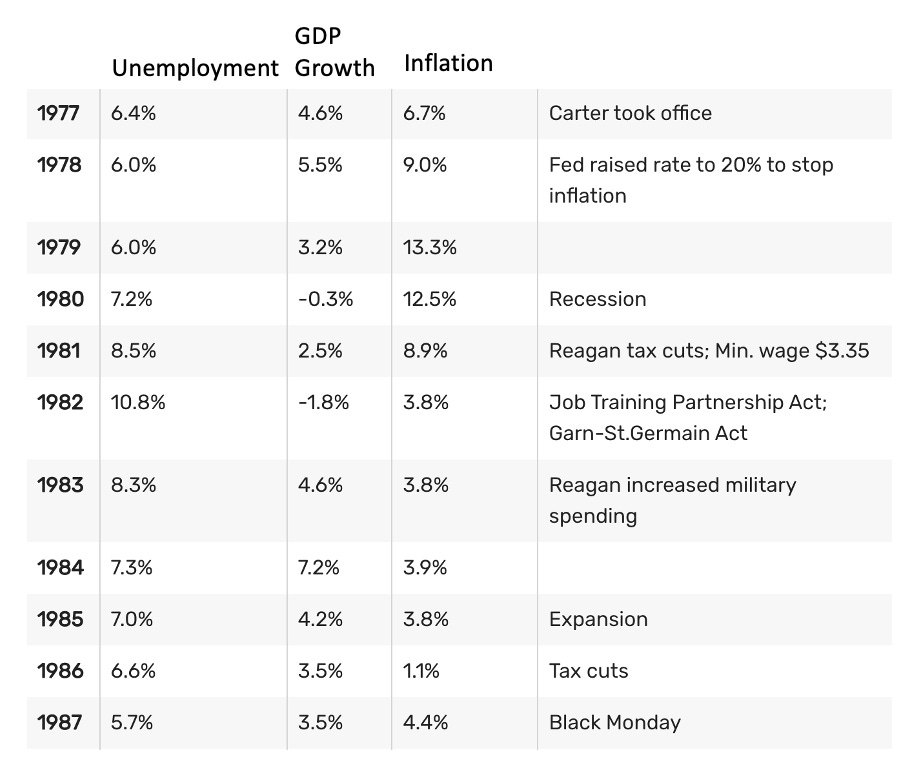

Unemployment, GDP, and Inflation Rate 1977 - 1987

What you can see here is that the American economy saw two recessions in the early 1980’s and unemployment reaching up to 10.8% in 1982 with -1.8% GDP growth. Essentially, the interest rates raised to 20% in 1978 created unemployment by tightening liquidity. It is important to note that it was December 1978, meaning it began to apply more to the 1979 economy, provoking a recession in 1980. After the recession of 1980, we saw inflation began to abate only to see another recession in 1982 and inflation finally under control.

The S&P 500 From 1970 - 1984

The positive thing about using interest rates to combat inflation, it worked. The bad, it drained liquidity from the system that would otherwise be used to invest into stocks. There were two major stock market crashes with a 10 year time frame. The first decline reaching 45% and the second decline reaching 29% from top to bottom. In other words, this fiscal policy killed stock market investor returns for 12 years. The beginning of the secular bear market happened when interest rates where raised to 12% the first time.

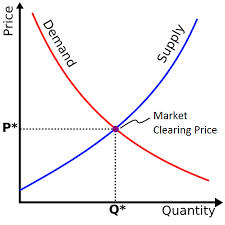

If you’re wondering why raising interest rates create economic turmoil, raising unemployment and creating market down turns. It’s all correlated between contracting credit (economic) growth by making the cost of capital, and debt, more expensive. When buying a car that has 3% interest vs buying a car that has 12% interest, there’s a significant difference between your monthly payment (your affordability of that). This essentially creates a ripple effect around the entire economy, tightening demand. It creates demand destruction.

By creating less demand through interest rates, this means that supply will exceed demand which will lower prices. Think of the little red line moving downward on the above graph. On the contrary to this, if you create excess liquidity (money) in an economic system, you provide the consumer with easier money. Think of the little red line moving upward. When you do this, demand increases which raises prices. Prices going up is just another word for inflation, making the value of the dollar (or the purchase power of it) go down.

What the Fed Minutes Outlined Today

After reading the Fed minutes today, it became clear that the Fed is becoming hyper focused on combating inflation. This is a problem, because this is historically how the Fed has created bear markets through out history. The thinking is always the same. The Federal Reserve over shoots easy money policy, in turn they think they’ve gone too far, and they over shoot the response through excessive tightening.

I want to point you back to the image above that outlays interest rates. The shaded areas are recessionary periods, do you notice something? Nearly every single time when the Fed raised interest rates it was followed by an economic recession. Specifically when it went too far. In the late 90’s, interest rates were raised deliberately to slow down the bubble that was forming. In 2008, interest rates were raised again only to be followed with the one of the largest stock market declines in history, a true Bear Market.

When we look at the recent minutes, this changed everything and the future outlook of the markets. Heading into the past week or so, we originally knew the Fed was going to increase the rate of taper to $30B/month with the potential likelihood of 2-3 rate hikes in 2022, depending on inflation. In response, it appeared that the markets seemed to accept this and we began to see a stabilization along with a massive bifurcation between small caps (risky stocks) and large caps. A correction became likely but, not a secular bear market or 20%+ decline.

Referring to my tweet above, one sentence changed everything, “Almost all participants agreed that it would likely be appropriate to initiate balance sheet runoff at some point after the first increase in the target range for the federal funds rate”. This means that they are likely to not only end QE and raise rates but also do quantitative tightening! Are they crazy?! Obviously it says it is data dependent which means they’re going to follow inflation and job trends. But, if inflation doesn’t abate soon, they will raise rates and let assets run off their balance sheet at the same time.

There is NO DOUBT this will create a massive shock to the financial system as rates, risk assets and historically high valuations will need to instantly find a new balance.

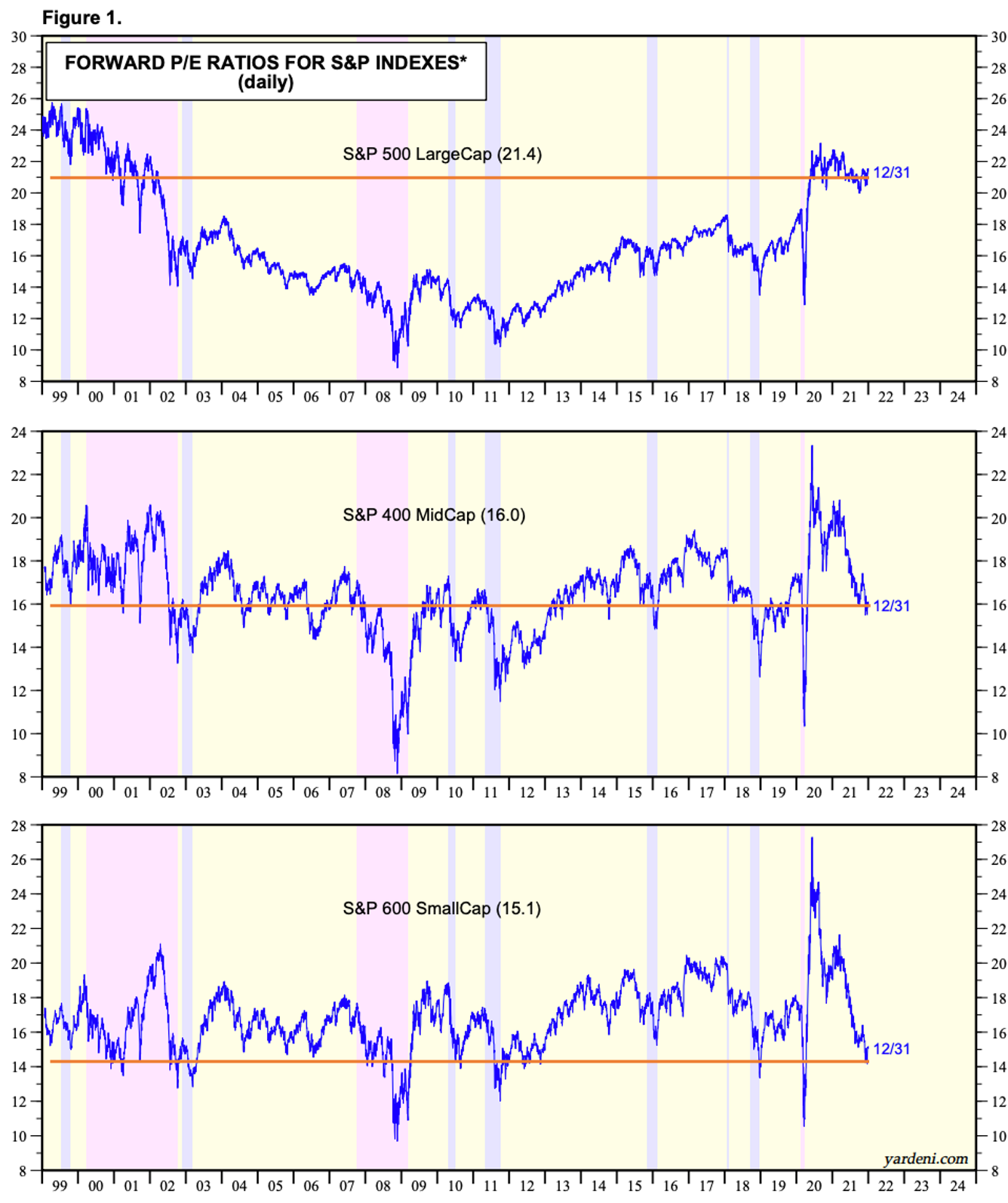

In certain environments, this wouldn’t be a very large concern. However, there’s one thing that I am extremely concerned about and that’s large cap valuations. This is a big problem when you’re able to draw comparison to the 1999.com bubble. This means that multiples could contract in large caps stocks down to a more normal forward P/E, which is 14x - 16x. The current average forward multiple in the S&P 500 is 21. This implies a near 30% contraction in FORWARD valuation multiples for the broad market index. If the S&P sells off, everything will sell off and we could hit bear market levels and possibly further. Also, no, small caps are not safe with historically low valuations. Smally’s can trade down further but they do present the best risk/reward.

Let’s Summarize this Thesis

To bring everything home and explain exactly what this publication is trying to say, the perfect storm is brewing and it needs to be understood by investors. This perfect storm is being driven by:

Historically bubble-like valuations in large caps and heavily weighted stocks (AAPL forward P/E is 30+, normally it trades at 10-15)

Raising interest rates & ending QE, which historically creates corrections in the market at the very least. If we look at 2015, a few years ago, we can see there were 2 major corrections back to back where the index dropped after QE ended. Imagine, QE just ended and the index sold off nearly 20%, they weren’t raising rates at this time. It then sold off again, 20%, before the first rate hike in early 2016. Eventually, resuming the uptrend.

Quantitative tightening, the icing on the cake. In late 2018, the Fed tightened monetary policy too much which created a Bear Market in September - December. They began “balance sheet run off” January 2018 where we saw a major correction of nearly 20%, once again. While letting their balance sheet run off, the Fed also raised rates at this same time. Couple this with international turmoil with China and trade wars, this was too much for markets. It sold off till the Fed reversed policy and became more dovish, not raising interest rates again and actually cutting them in 2019.

The thesis is that, based on the Fed minutes, they want to end QE, raise rates and let the balance sheet run off within a few months span! There is no doubt that this will stress the financial system as this is too much too fast. Before thinking about raising rates after the 2008 financial crisis, they didn’t raise rates until 2015 after cutting them to zero in 2008, basically 7/8 years later. 3 years after that they began to do QT. In all circumstances where the Fed changed policy to tighten liquidity, markets sold off nearly 20% and now they want to do all three hawkish policies within a few months of each other. We are talking about aggressive, restrictive, and hawkish policy that we haven’t seen since 1979/1980 to combat inflation.

For perspective, this will help paint a picture what a 20%, 30% and 40% decline would look like in the S&P 500.

For the past two years, there’s a scenario where we will see confirmation of the narrative of a “Fed Fueled Bubble” that found its way in growth stocks, like the NASDAQ. But, because of the Large Cap valuations and tightening monetary policy, just like during the 1999 bubble (where valuations this high were last seen) everything could come down to historically normal valuations.

This is a scenario, not a certainty. I am wrong a lot but I don’t stay wrong and I always follow the data. My previous market prediction were based on the fed being more accommodative then 2-3 rate hikes, ending QE, and quantitative tightening (balance sheet roll off).

The next section will be for members only as it will discuss my portfolio moves and strategy on how I plan to profit from knowing this. If you like this content, please consider subscribing for access to the below and all future publications around this type of material.

My Portfolio Strategy

Like I mentioned above, I based my previous knowledge on a more accommodative approach from the Fed for 2022. I make all my decisions based on 2 market principles:

Earnings drive markets and stocks higher, long term

Liquidity (Fed) determines price in the short term and can create boom/bust cycles

I assure you, every market correction and cycle can be attributed to those two principles throughout market history.

I was incorrect about my previous hypothesis about ARKK over performance, this boom/bust cycle must unwind and that’s exactly what the fed is doing with this policy change. This is most apparent in high growth stocks, Jamin Ball does an excellent analysis on cloud stock valuations. We should consider the historical average of 10x - 15x to come into perspective based on contracting market liquidity from the fed. Valuations are still historically elevated.

Because of this, I have officially hedged my portfolio with an ARKK short. I am 100% short, meaning I have every dollar of equity tied up in a leveraged short position. In addition, I have cleared up a majority of my high growth tech stocks that are unprofitable. My current cash allocation is 10% - 15% and I may continue to raise more cash in some of my stocks. I do plan on investing at the bottom of this thing.

I am comfortable holding names like PUBM, APPS, BRLT, DLO and GLBE because they are all profitable with many, many years of growth ahead of them. I also think a few, like PUBM, APPS, and BRLT, are trading at their floor. However, we will see. Profitability will matter in 2022.

Navigating a monetary tightening climate is never easy. I do not think we’ve seen the end of it. The big dogs still have to fall next and they will, in time.

It is important to say I don’t know what I don’t know and I spend hours learning about new developments every day, which is always what I share with you guys. These new developments have caused me to change my market outlook and I am more content being SHORT in this market (due to fed policy) than long and definitely not leveraged long.

A scenario where I see all of this changing is if the Fed reverses course, which will give a strong bid to growth stocks and the market as a whole. I will certainly keep you all updated and I will see you at the bottom of this thing, there will be fortunes made in opportunistic Bear Markets.

Stay tuned, stay classy

Dillon