A Recession is Coming and So is a Large Market Crash

All Leading Indictors are There

As part of an ongoing series, I began doing this roughly in November 2021 when I published this article.

Following, I published a following article after it became clear that stocks did indeed begin to crash. Specifically, growth stocks.

On January 14th, I was nearly spot on calling the top on the NASDAQ with this article

Following this, I posted an article about a looming recession.

Then, the last I posted was in middle of February right before the final leg down in the NASDAQ

But now, the markets are ready for what I believe comes next. I believe we’re positioned for a big move. All leading indicators are flashing red and this is where to look.

Leading Indicators

Yes, my stance is changing as I’ve come to realize something is missing. For awhile, I couldn’t quite fully understand the market rotation as main stream media only covered interest rates and the Ukraine/Russian war. But, it’s becoming clear that something bigger is going on. The general theme and indicators is bearish, very bearish, like 2008 style kind of bearish. But, I will provide what exactly to look for at the end if this thesis changes. More or less, I am beginning to believe we are heading toward a recession and what makes me the most concerned… The Fed can’t bail us out this time.

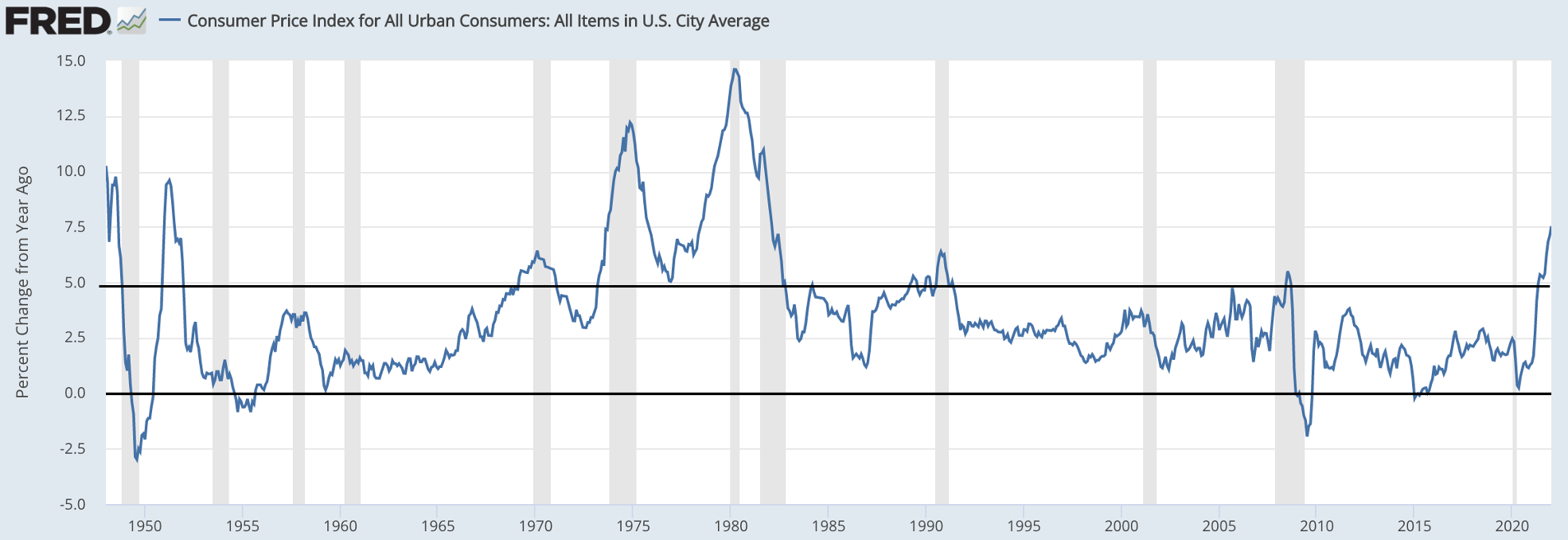

Inflation

This is the primary problem in all of this. But more importantly, the inflation problem is almost entirely out of the Federal Reserves control. Now, inflation is being cause by U.S. Government policy (oil), the Russia/Ukraine war, and continued supply chain disruptions. In other words, a recession is nearly becoming a certainty.

Above, you can see that nearly every time inflation has run above 5% we have a major economic recession. The only time we didn’t have a recession (right away) was in the 1950’s. But, it was followed by a recession within 2 years.

This isn’t what concerns me though, my concern runs much deeper.

Since 2008, you can see that we have done extraordinarily well avoiding any economic disruption with only the COVID-19 pandemic (artificially created). The reason why we have avoided this was through the Fed’s use of QE. Essentially, every time we began becoming concerned about the economy, the Federal Reserve would print money and stimulate the economy.

Since 2008, this QE is what has pulled us out of potential recessions when the economy got fragile. You will notice the asset column expanded rapidly in both 2008 and 2020 to prevent a global economic collapse. But the problem with this is that QE contribute’s to inflation. If we have major economic problems now, how is the federal reserve supposed to prevent another down turn?

They can’t, otherwise they risk creating a hyper inflationary environment and extreme stagflation.

To make things simple, we are not equipped with the current conditions and tools to combat economic struggles.

Oil, Commodities & The Economic Cycle

Both oil and inflation are hidden taxes. This means they tighten the consumers pocket book without the government directly contributing it. More importantly, it is also a leading indicator to major economic recessions.

Oil appears destined to reach the $150 mark and, today, it is driven by U.S. federal government policy. If the Biden administration continues to bottle neck U.S. domestic oil production and SANCTIONS Russia’s oil, this is the nail in the coffin. It becomes a cascade of events at this point. But you may ask yourself, why is high priced oil a leading indicator of recessions?

It’s all about demand, spending and a consumers cost of living. If the cost to transport yourself to and from work, or to drive really anywhere, becomes too high, the consumer has less money to spend on goods/services.

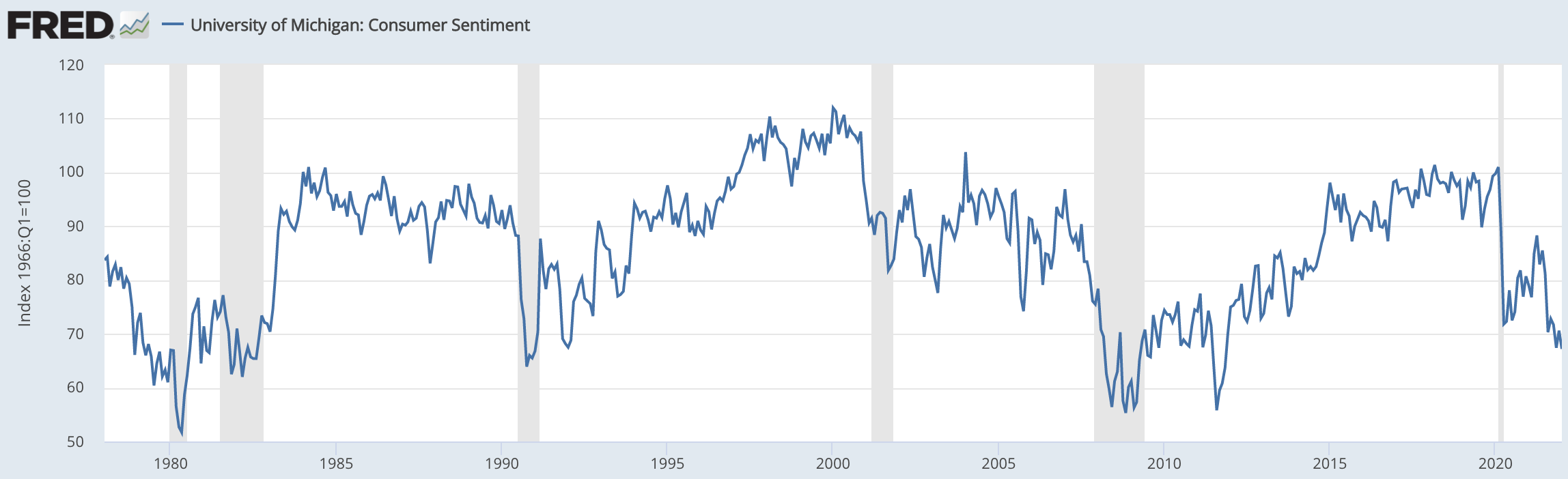

The Consumer

This is where we’re going to tie in inflation, the price of oil and the American consumer. As mentioned above, the cost has living has become too high while wage growth has risen slower than inflation. With inflation alone, this puts a lot of strain on the economy. However, when you factor in the other hidden tax in the form of oil, there’s a big problem. This is best reflected in the consumer sentiment survey held by the University of Michigan.

You can notice that sentiment drops before recessions and usually bottoms during an economic slow down. When you look at todays levels, it’s consistent with previous economic recessions and in some cases lower. In other words, this is a leading indicator of what is to come.

When you constrain the consumers pocket book with high prices in the form of inflation, see minimal wage growth and then couple this with high oil prices, we have a big problem. Think of it like this, if a consumer has $1,000 a month extra they may spend their money on going out, on goods, etc. This essentially fuels economic growth. But, when you decrease the value of that $1,000 by 7% - 8% (in some cases higher) then they have less buying power. Then we add the basic need for transportation, we have a cascading effect because this impacts:

Airline tickets

Business travel

Recreational travel

Basic transportation needs, etc

In addition to traveling, it also raises the cost of goods for shipping. In our situation, we already have supply chain problems, then you add energy problems to this. This creates inflation in areas the Fed cannot control. The only thing the Fed can do to combat this is raise interest rates which creates a form of demand destruction. The reason why it “destroys” demand is that it makes the cost of capital (lending) more expensive. Think of it like this:

When you go to buy a car, would you rather have the interest rate at 3% or 5%? What is the impact of a monthly payment that’s $100 more a month? Can you afford ‘less’ vehicle at this point? Are you likely to just fix up an old clunker rather than buy a new car?

The Bond Market

Perhaps the most telling, certain, sign of all is the yield curve. What we are witnessing is an aggressive flattening. What this tells us is that economic outlook is not as certain in the short term while the long term secular trends in the next 10 years remain constant.

The 2 year is more indicative of Fed policy and near term economic strength and the 10 year can be thought of as the structural changes that are happening in the economy. The reason why this is arguably one of the most important indicators is that the bond market is considered “smart money” (think banks, hedge funds, large investors, etc.) who typically work in a different environment of macroeconomics.

I trust what the bond market is signaling. If the yield curve inverts, it’s a certainty we are close to an economic recession.

The Equity Markets

The business/market cycle is flashing signals we haven’t seen since 2008. Yes, I know it’s extreme to compare this but hear me out.

When you think about what equities are doing the best right now, we see Gold, Commodities, Oil, and defensive stocks. This is consistent with the market top we usually see in the graph above. In 2007/2008 we also saw gold perform extremely well heading into the recession and during the next few years after.

The price action leading into the great recession reminds me a lot of what we are experiencing today.

The Biggest Risk that’s Present Today

During 2008, we managed to escape economic collapse during this time. The reason why, we (as Americans) passed the infamous “Wall Street Bail Out” to bail out the banks. Although unpopular with the American public, this prevented the collapse of the banking system, or, a repeat of what happened in 1929. Since then, the Federal Reserve has been using its “tools” on the balance sheet to artificially expand or slow the economy to prevent inflation or recession. This is best depicted in its balance sheet in the image below.

Notice in the image how, during 2008, the Federal reserve doubled their assets. Essentially, what they did was finance U.S. government debt and this U.S. debt created fiscal stimulus that cascaded throughout the economy. They basically used an inflationary force to offset a deflationary force. The deflationary force, in this sense, is a contraction of credit and an economic recession. The inflationary force is U.S. government spending & QE.

You can notice that they used the same philosophy in 2020 with the COVID-19 pandemic as well

But there’s a big problem today. During the pandemic, they printed too much and spent too much. In addition, COVID created a few other challenges not otherwise thought of. It decreased globalization (deflationary force), decreased global labor supply and fueled a dangerous asset bubble, which has popped.

We are in a situation where we have rampant inflation that is being caused by COVID disruptions as well as war disruptions from Ukraine/Russia. This prevents the Fed from acting and preventing an economic recession, possibly a depression.

The Fed cannot act today because if it does, it can continue to add fuel to the fire of inflation when it’s already public enemy #1. This means that the Federal Reserve cannot intervene in the likely event that is an economic contraction and credit contraction within the U.S. & global economy. Basically, the risk is high for economic problems.

What Can Reverse this Scenario

The way I see it, a majority of our issues stem from one single factor; oil. Oil is what is leading CPI inflation upwards and creating pricing increases across the board (obviously supply chains as well). The way I see it, in the unlikely event that Joe Biden reverses his energy policy and unleashes the power of American production, this is likely to continue with the war only making it worse. There are two things that can reverse course for the energy crisis:

Russia backs off Ukraine and sanctions are lifted from Russia

Joe Biden aggressively incentivizes U.S. energy production to levels last seen, maybe higher, in the Trump administration

For this week, this is what I’ll be paying attention to. If this energy crisis is not resolved, we are likely headed toward a snap in the global economy and a contraction unlike we have seen for a very long time. A major S&P decline is also very likely in this event as well, much larger than where it is today.

Obviously, price action will tell all because we don’t know what we don’t know. The data we have access to as individual investors is not as sophisticated as the data the larger institutions have. They will see a reversal in this course weeks/months before many retail investors will.

Summary

This isn’t meant to instill fear, it’s meant to share my thoughts and the leading indicators I am paying attention to. In many ways, we are already seeing an economic slow down and every time you look at the gas prices, they are going up. I encourage investors to have a risk management strategy going into the next few months.

I do hope I am wrong.

Stay Tuned, Stay Classy

So what to do now?

Thanks for the article. This terrible and completely unnecessary war is costing lives and might push the economy over the edge. What is your strategy now? Sell? Big hedges?