BluSuit's Investing Philosophy

BluSuit's Investing Philosophy

Transparency is everything, that's why I'm sharing this with you

Learning about stock picking philosophy from other great investors has arguably been more important to me than the frame work they use. The reason why is that a framework can often be flawed if one does not fully understand the ‘why’ of a particular “box” that needs to be checked. If it wasn’t for other investors willing to share their thought process and approach to investing, I wouldn’t be where I am today at 30 years old pursuing a visible path to financial freedom.

Estimated time to read: 15 Minutes

BluSuit, the company I founded, is dedicated to sharing financial strategies, tools, framework, and business research to help ALL investors make money. As retail investors, it is our duty to help each other grow and learn from successes and failures. I, at my core, believe there is more than enough money for all of us to be millionaires and financially independent. We just have to put in the work.

My approach to stock picking is a combination of growth investing, value investing, technical analysis and fundamental analysis. Would I consider myself a trader? In some ways yes and in some ways no. I think a better term would be a portfolio manager and active investor. I believe some people would call it G.A.R.P., or growth at a reasonable price. The reason why I do this is relatively simple, I believe picking the best businesses at good prices yield market beating returns.

My focus is on growth stocks and the best businesses that have a long runway for growth. All I care about is catching a business in its most rapid stage of growth, with the anticipation of holding it for years. When I say, “the best businesses” this term can be a source of debate because everybody thinks their stocks are the best. The first thing to know is that this is subjective and not objective. More importantly, a story can change rapidly. If you’re wrong, don’t stay wrong. The business environment changes fast and the decisions/opinions you make should change just as fast, if not faster.

Before I begin digging in to the key pillars of BluSuit’s investing philosophy, I’d like to take a moment and bring you toward a news letter I recently received. Mentioned news letter: Stock Squawk by Parrot @ParrotStock.

I thought this was extremely relevant to the this planned publication. In summary, processes and strategies are developed and evolve over time. By no way do I think BluSuit’s investing process is the best but it’s what works for me to beat the market. Your process may be different.

The goal of this news letter serves two purposes. The first; experienced investors can benchmark their process and philosophy. It’s often helpful just to hear a different perspective. The second; new investors that are still developing their process have the ability to see if there are characteristics of this philosophy that could potentially work for them long term.

Revenue and Earnings Growth

Many familiar with my work won’t find this as a surprise. When I first hear about a company, or receive a tip from someone, I check the revenue growth. If a business isn’t growing revenue or hasn’t grown revenue yet, I will usually dismiss it. If I don’t dismiss it, I’ll keep it on my watch list to see how the story develops long term.

Many investors want the best story and many stocks will run based on “potential”. The problem with this is that it doesn’t matter how great of a technology a company has, the story doesn’t matter (long term). Stocks must have some sort of fundamental framework to fall back on or you may find yourself on the losing side of a pump and dump trade. A company must have sales and revenue.

I am not saying pump and dump’s don’t work, but I do know that 90%+ of the time most of these businesses rally up and eventually come crashing down days/weeks later. More importantly, I have seen countless high tech, next gen, companies with ground breaking products only to never live up to their potential because they cannot sell and they miss price their product. Investors, long term, need some sort of fundamental return. This fundamental return is called earnings.

Earnings are also called net-income, or profit. This profit is exactly what share holders receive in return. Let me give two examples:

Scenario 1: I have a lemonade stand and I have been operating it for awhile. Currently, I am selling about $500 of lemonade a week. Of that $500, the business is making (net income) about $100. I have a problem though, I want to expand my business. I know that I need additional capital to expand and open a new lemonade stand. I approximate that I’ll need about $1,000 for expansion and I decide to see if anybody wants to give me money in exchange for business equity (ownership), where I would now share the future profits. I tell you, “dear reader, I will give you 25% of the business for $1,000”. You figure that, assuming financial projections stay consistent, that the business will eventually sell $1,000 in lemonade per week and earnings will be about $200 per week. If you own 25% of the business, that means you’re entitled to $50 per week of profit. This profit goes directly back into your pocket. At $50/week, you figure it would take approximately 20 weeks for you to make all your money back in profit and it will continue to make money for you long term. It makes sense, right? You get your money back and when it’s all made back, your investment continues to pay you money over time.

Scenario 2: Same lemonade stand, same plan of expansion. Except in this scenario, I am still selling $500 of lemonade per week but I am losing $50 per week. This means I am net income negative and I am losing cash. I ask you the same question, “Do you want to invest $1,000 for 25% stake in the company?” You run the numbers and figure that if I have 2 lemonade stands operating the same way, I will increase my revenue to $1,000/week but the business will lose approximately $100/week. The next question is, is there a path to profitability? Because you need money in your pocket to recoup your investment and create that passive income opportunity. However, I answer your question and say, “Yes, but it’s about 5 years away. I am really trying to just grow the business which is why I am losing money today.”

In scenario 2, many investors instantly look away and say, “no, that’s too risky. I have no idea if I’ll make my money back”. In scenario 1, investors are more confident that they’ll receive their money back and create a long term passive income opportunity. With scenario 1, I’ll likely be able to raise additional capital as well because more investors are confident in this business scenario’s ability to return their initial investment and generate long term returns. This increases the ‘valuation’, we’ll talk more about that later.

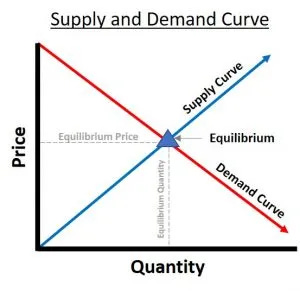

When we think about the stock market, it’s important to understand exactly what it is; it’s a market. At its most simple state, it’s a place for investors to buy and sell small pieces of individual companies (equities/stocks). The collective state of confidence in a businesses ability to return the initial investment is reflected in a share price that is dictated by supply and demand. The more confident investors are, the higher the share price.

Let’s bring this back to why a core piece of my philosophy revolves around earnings and revenue growth. From the information above, we can draw a few key conclusions:

A businesses ability to provide earnings is the equivalent to real returns

Real returns give more investors confidence

Confidence creates demand which is what moves a share price along the supply and demand curve

More demand than supply = stock price appreciation

When we think about the principles above and apply it to growth stock investing, specifically revenue growth, we (as investors) can assume that if a company is growing revenue we can make our money back faster in the form of earnings. The faster the revenue growth, the quicker we make our money back especially if the business is profitable or will become profitable in the near future. I’ll cover valuations soon, but the concept is below.

Assuming the same time frame, a slow growing company will be priced lower because investors know it will take a longer to make their money back. On the contrary, fast growing companies are priced more expensive because they anticipate their earnings will come back faster. A growth companies ability to grow revenue and grow earnings, justify’s faster share price appreciation over time because earnings (or real returns) grows faster than the broader market.

This is why I am a growth stock investor. I try to pick companies that can grow net income quicker than the broader market to produce market beating returns.

Short Term Market Volatility is an Opportunity

There are periods in the market that are often very confusing. Investors and traders are willing to sell their stocks at steep discounts because stock prices are going down. When you pull open your watch list, you can see every stock follow the exact same pattern. It does not matter what a company does or how profitable they are, people will sell anyway.

Now, I do think there are instances where a portfolio manager should hedge their risk to maximize the opportunity of a steep sell off and protect account value. In most cases, when the markets decline it can create a lot of pain for many investors. In fact, I often hear people refer to it as “max pain”. What a lot of people don’t mention is how making emotional portfolio decisions during this pain can be detrimental to a long term portfolio’s performance.

My strategy strongly coincides with the 80/20 rule, in this case it’s centered around 80% fundamentals and 20% technicals. During market corrections, having a strong fundamental back ground is crucial and important. When everything is selling off the only thing that a business, or a stock, has is the underlying business model and it pays to buy on dips. A stock price always catches up with the business’s performance over time and the best, most profitable, company’s are the first to rally and recover.

It has been a historically proven strategy to take advantage of discounted stock prices to great company’s. Benjamin Graham’s Intelligent Investor, a world renown, Warren Buffet recommended, book, talks about taking advantage of stocks when they find them selves at bargain prices. Another book, “Richer, Wiser, Happier” by William Green, discusses the exact same thing. In both cases, both novels talk about the greatest market crashes in history, the 2008 financial crisis and 1929 market crash. They both tell stories of legendary investors who went against the crowd and bought stock, rewarding the bold investors with rich’s beyond their imagination.

In recent history, the Corona Virus induced crash rewarded investors who bought around the bottom. Here are the returns of a few companies since mid march of 2020.

GOOG: 166%

APPL: 160%

MSFT: 125%

TTD: 378%

CRWD: 625%

ROKU: 318%

It pays to be a buyer, know the business that you own, focus on revenue/earnings growth, think long term and HODL (hold on for dear life)..

Valuations Matter, and so do Technicals

Using both methods for stock entry can prove to be a deadly combination when it comes to yielding market beating returns. It often stems from the saying, “it’s not when you sell a stock, it’s when you buy it that you make money”. Essentially, this means that it’s all about what you pay for your investment opportunities that delivers long term rewards.

When it comes to valuations, this is often overlooked but it shouldn’t be. This is technically the “price” you pay for the stock. Let’s go back to the lemonade stand example mentioned above.

In scenario 1, I mentioned that the rate of when you get your money back is directly derived from the earnings/net income of the business. In the Lemonade Stand example, it was approximately 20 weeks until an investor gets their money back assuming a $1,000 investment for 25% of the business. This puts the business at approximately a $4,000 valuation. During a market downturn, this valuation decreases by no fault of the business. During COVID, the market saw roughly a 30% decrease. If the Lemonade Stand valuation decreased by 30%, its valuation would be approximately $2,800. This means that you can put $1,000 into the business (the same amount of money before) but now own 35.7% of the business. Because you own 35.7% of the business, rather than 25%, you are entitled to 35.7% of the profits. Your $1,000 will now be paid back in 14 weeks rather than 20 weeks because you’ll collect approximately $71.4 per week rather than $50.

During market corrections, you are able to buy a larger portion of the company with the same initial investment. Thus, participating in a larger portion of the long term returns in that company. Understanding and knowing what you pay for a business is the key to knowing how much equity you own in a particular asset that appreciates over time. The higher the valuation, the less % of the company you own with a fixed initial investment. The lower the valuation, the larger the % of ownership you have in a company with a fixed initial investment. The goal here is to own as much as possible in a company that’s profitable.

Referring back to the supply and demand curve, when it comes to stock prices, there are often companies that have seemingly unlimited TAM’s (total addressable market) with out- of-this-world operating margins and breath taking growth. In this case, valuations become difficult to estimate and forward multiples are pulled years out of the future. Above, you see a chart of DLocal, one of my favorite companies. There is nothing rationale about this business’s valuations but that has so much to do with their company execution. They have approximately 40% EBITDA margins with 100%+ growth and no sign of slowing down. In this instance, I often use technicals to begin building a position.

Technicals offer the long term investor insight into lines of support and resistance to gauge potential areas of opportunity to add to a position. Lines of support and resistance are basically areas of increased demand or supply. The reason why a long term investor may use this strategy rather than a valuation strategy is the acceptance of not knowing what you don’t know. Institutions, money managers, investment banks, and many other big money investors have teams and complex algorithms that run forward valuations and take into consider data points you wouldn’t think of. If I waited for DLocal to get to a forward P/E of 30, I wouldn’t hold my breath because it will probably never happen.

From my investing perspective, I use technicals to participate and own the best businesses I can find where the valuations don’t necessarily make sense today but most likely will 3 years in the future. I continue to accumulate DLocal, specifically, and as it falls I add to my initial investment to build the position. In this case, dollar cost averaging on key technical points is a way to go and an appropriate strategy. I missed on Tesla because I looked at the TTM P/E and NTM P/E before it began its run up and I passed on it because of valuations. But, today, the valuation makes sense as their gross margin and operating margin continues to expand with accelerated revenue growth.

Summary

To summarize everything above, there are a few key things to know about my investing philosophy. First, I want to emphasize that this is what works for me and I do not have all the answers.

Revenue and earnings drive stock prices over time. It is all centered around real returns, or earnings, and the revenue growth of a particular stock justify’s increased or decreased valuation multiples.

Market volatility is an opportunity to buy incredible businesses at great prices and I often do the most buying during these periods

Valuations provide an excellent frame work for investing but the best businesses typically have valuations that don’t make sense, in this case technical analysis substantially helps

A natural follow up to this news letter would be a frame work I use when stock picking. There is a mental “check list” I do when assessing if a business is a good investment or not. I will have to release that one as well. I have this and much more content planned for you guys!

For those who have not yet subscribed, if you are interested in getting closer to this type of investment philosophy I high encourage you to join our membership.

Thank you for your time, stay tuned, stay classy

Dillon

Here I am again ;) Really well thought out article and explanation. Nice job!

I like the idea of a blended approach to stock picking and entry; growth, value, technical, etc. I'm not sure why a lot of folks have to abide by only one black and white strategy. The market seems much more nuanced than that, just like everything else in life.

I've started using basic technical analysis such as MAs, RSI and MACD to help with entry. I picked some good stocks early on at a bad price and paid for it. It helps give me a pricing framework and keeps me patient and disciplined. I'd love to hear more detail about what technical indicators and analysis you incorporate and looking forward to more discussion on valuation.