Confluent - Opening a New Market Opportunity

A well run business, who founded Kafka, with a seemingly limitless market opportunity over time

When I first came across Confluent, I quickly dismissed it because it was expensive. At the time, it was trading at 40x P/S and I couldn’t justify that sort of stock price. But fortunately I have had the chance the accumulate more at depressed levels. Obviously, Confluent was caught up in the tech bubble and its inevitable bursting which may leave its chart looking unattractive at first glance.

From Institutional Money Managers to Independent Investors, I am Going to Put One on Your Radar that I Think is a Long Term Winner

This has the “recipe” I usually look for when I evaluate a stock. Typically the stocks I pick have similar qualities:

A mission critical component in B2B

Recurring revenue

Higher than average growth, showing fast adoption among international businesses

A strong and clear moat, offering some sort of differentiated offering from direct and indirect competitors

A strong balance sheet allowing for focus of execution on the long term business plan

A competent and effective CEO

Cash flow positive today or positive cash flow within two years and ample amount of cash to get there

An attractive long term market opportunity

A sticky business model with high switching costs

The concept of individual stock picking is simple, it’s to produce alpha. If, back in 2009, you spent your time accumulating businesses like Google, Apple, Amazon, Adobe or Salesforce you would have produced tremendous alpha for 10+ years without trying to time the next macro cycle or buying and selling based on a 200 day moving average. Good businesses produce good returns over time, especially those with excellent management.

I am confident all investors should have some exposure, at the very least, to some of these growth businesses I discuss every week.

Estimated time to read: 10 Minutes

Format:

Business thesis and business model description

Current financials

What I am looking for in the coming earnings reports to validate thesis

The goal is not necessarily to do a “deep dive” but to provide an introduction to the business

Confluent

Jay Kreps, the CEO, was formally the lead data architect at LinkedIn when he founded Apache Kafka with a few of the other founders at Confluent. Apache Kafka, if you’re not familiar, is a code based system that “puts data in motion”. To make things simple, it goes away from the traditional data model where it is stored and queries need to be run to extract it.

As data needs began to evolve for many different applications and businesses, the demand for real time processing manifested itself. Think about traditional business models that used to have filing cabinets where you would store physical pieces of paper that contained information (data). In order to get that piece of information (data), you had to call somebody and ask them to fax it over to you.

Alright, alright, this is more back in the 1980’s (lol) but things have really evolved that much since then. Next generation technology eventually allowed that information to be stored electronically on computers. This, in other words, could be stored on the “hard drive”. Do you remember when we used to have to care about how much space we had on our computer?

Eventually, we could store that information in the cloud (think Amazon web-services) but the process of retrieving that information would still be the same. The next evolution of data would be “data in motion”, meaning the constant flow of data that can be interacted with real time. The way I look at this, this is the next evolution of business, real time interactivity with consumers or stake holders to instantly respond to events.

The best way I can explain how this works is in a similar, less technical way, that Jay Kreps does. Jay coins Confluent as the “central nervous system” of the business. To build on this, we can draw comparison to how our brains process data or information. As we interact with our world we typically have an event and we respond to that event real time. Think of touching a hot stove top; we don’t necessarily have to try to ‘remember’ (our version of tapping into a data base), we instantly respond to our environment and pull our hand away. Basically, it’s hot, we know it hurts, so we respond instantly. The cause and effect was instant.

Confluent is a platform for businesses to use Kafka and their cloud platform allows a managed solution of Kafka. This is effective for companies in a few key ways. Typically you may need a developer (an actual person) to create code, process it and adjust it to suit the needs of a business but Confluent does that managed portion for them especially within their cloud offering.

When it comes to the core thesis of Confluent from a business model perspective, this is a play on the evolution of the modern enterprise. In my eyes, I can imagine that the data needs of an enterprise is only just beginning and it will continue to evolve, becoming more demanding, over time. Specifically when it comes from the real time need of data streaming and data processing. I can see that, as business models evolve, the need to interact with consumers or stakeholders real time will only grow. In addition, I believe there are applications and use cases past what we can understand that can/will evolve through Confluents platform.

When thinking about competitive advantage and differentiation, I know that there are a few other managed streaming platforms in the major cloud vendors like Google, Microsoft and Amazon. However, investors time and time and time again forget that the most important characteristic of many of these infrastructure businesses that are building on top of those major cloud players is that they are multi-cloud.

According to Factioninc.com, “Today, 92 percent of organizations have a multi-cloud strategy in place or underway, and 82% of large enterprises have adopted a hybrid cloud infrastructure. On average, organizations are using 2.6 public and 2.7 private clouds.”

This is the same as the bull case for GitLab (I will post about them at a later date) and Snowflake. The importance of being multi-cloud cannot be understated as more and more businesses move away from just one provider. They need a system that can integrate with many different data sources to create a collaborative infrastructure.

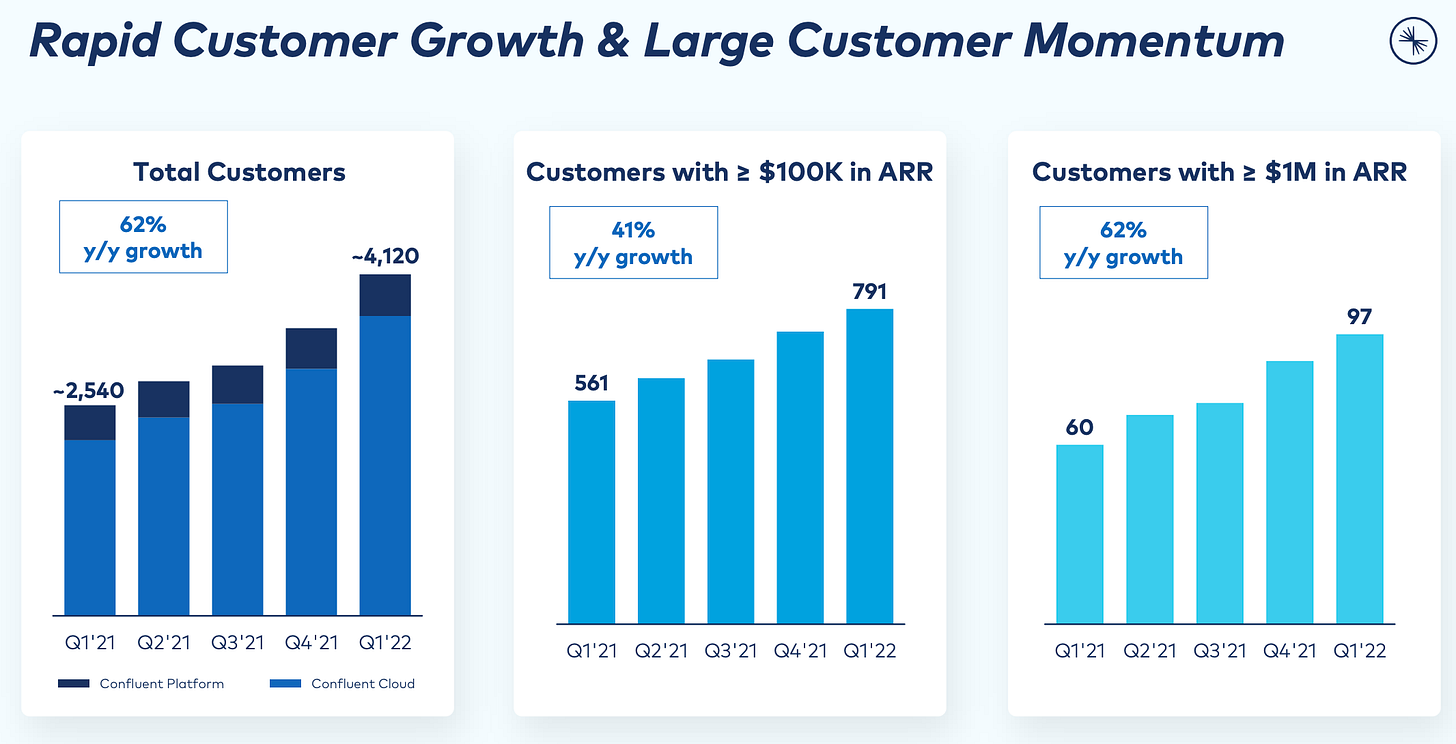

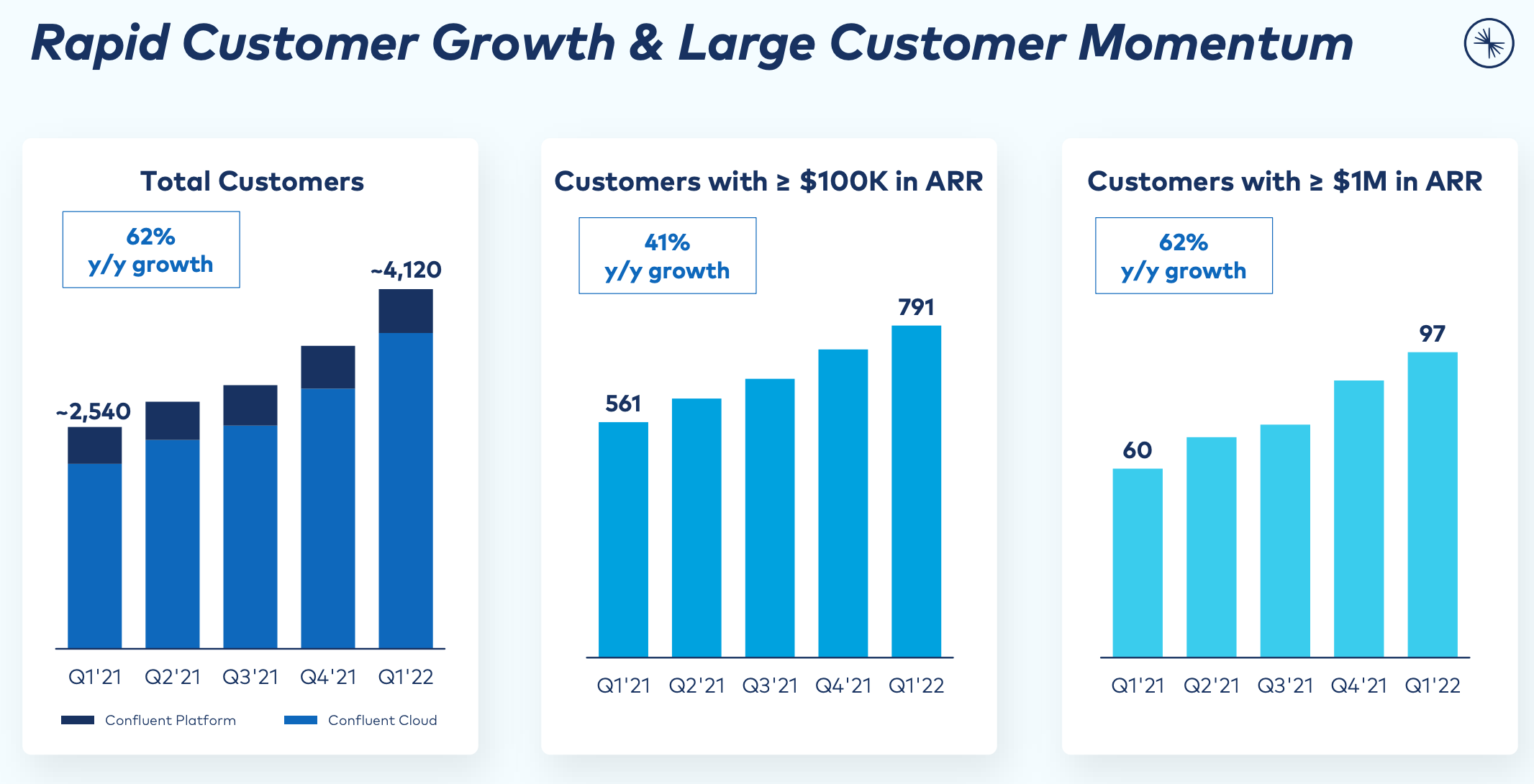

Confluent Financials

The key is in the details with Confluent because the story is not necessarily on their top and bottom line. It’s what’s going on beneath the surface of the top and bottom line metrics and how they are evolving. In particular, I am referencing their fully managed cloud product rather than their self managed product.

Since IPO, their cloud solution has been growing nearly 200% (in many cases over 200%) and has grown from under 20% of their total revenue to over 30%. What this means is that their business should continue to see strong top-line growth of 50%+ for years into the future assuming their cloud business maintains (with progressively diminished) momentum. Over time, we will likely see their platform become a smaller and smaller portion of their revenue while their faster growing managed cloud solution will become dominant.

Using analyst estimates, they have them reaching break even cash flow in about 1 1/2 years, which falls under the qualification I am looking for when finding a company with break even cash flow or close to it. To build on top of analyst estimates, Jay Kreps and Confluents CFO Steffan Tomlinson have mentioned multiple times that they expect to be break even cash flow in 2024. Obviously there is always risks but it’s hard to imagine a world where they don’t get there with scale.

When it comes to their balance sheet, it’s basically a fortress and more than capable of handling any macro environment. Above, I highlighted their long term debt portion which could “normally” be thought of as a risk. But, this is a convertible note offering they made in December 2021 when interest rates were still very low.

Above I included the press release from Seeking Alpha where you can see that it’s 0%. Dude, let me pause right here. These senior convertible notes are basically a call option. Let me explain what this means:

Investors who gave Confluent $1B today have an option to buy 9,993,600 shares in 2027. This means that later on down the road, this will be dilutive to current share holders ASSUMING that Confluent reaches over $100/share by that time.

Confluent does not need to pay interest rate on this debt between now and then

Confluent currently has roughly 126 million shares out standing. This will be dilutive by roughly 8%.

Until 2027 this has no financial business impact. If they are cash flow break even by 2025, they wont need to worry about raising anymore capital potentially ever again

Last quarter they had nearly -$60m in free cash flow, which means that left the balance sheet. This is obviously high, as we can see the last few quarters on their FCF margin but if we ran the numbers and saw exactly how long they could last without improving their FCF margin and not raising any capital we come up with roughly 8.5 years left assuming -$60m in cash per quarter (which I doubt will happen)

Conclusion on Financials

They look good

What I Am Looking For in the Coming Quarters

There are a few risks in the future that I see, which is typically why I monitor my stocks so intently over time on a quarter by quarter basis. The best stocks, I have found, over time consistently improve the fundamental story. However, I am patient if there are slight hiccups along the way. For example, last quarter Global-E (another one of my businesses) had to guide down revenue on a full year basis because they had roughly 5% of their business coming out of Eastern Europe. They guided down 5%. We need to use common sense.

On the other side of the equation, I watched Digital Turbines bottom line metrics continue to deteriorate with a high debt load. I quickly decided I needed to cut them and forget about them as they were headed toward a downward spiral. My cost basis was $65, I sold them at $45, they are now $16/share today. I took a loss, but it was devastating like it could have been.

What I am trying to say is that I don’t believe in buy and hold. I believe in buy and validate, over time. When in doubt, get out and don’t hold deteriorating business models but understand the difference between growth pains and fundamental risks in the asset.

When it comes to Confluent, these are the risks I see today:

Emerging competition - we need to pay attention to emerging competitors that are not the major cloud providers.

Negative FCF - we need to make sure that they continue to improve and manage their capital effectively. It may not be perfect here and there may be growth pains as well but one missed quarter isn’t thesis changing.

Continued, strong, top-line growth - I expect a deceleration in their cloud growth but do expect to see their top-line growth remain strong and relatively in-line with analyst expectations. I will become concerned if I see a material slowdown in the business, which will bring serious questions about the business execution.

Taking on more unnecessary debt, I doubt this will happen but it’s always something to pay attention to

No investment is without risk. What I need to see from Confluent moving forward:

Continued execution on the top-line revenue growth while maintaining responsible responding. In particular, growth investors should pay attention to the sales and marketing expense. If their growth slows down while S&M expense increases, this is a red flag.

Cloud becoming a larger and larger portion of their revenue

Continued customer growth, especially those with $1m+ in ARR

Continued improvement and development of the core thesis outlaid above. I have found that businesses who constantly change their tune on who they are deteriorate over time. My classic example is Fubo, where I liked the thesis originally but then I began to see the narrative the management team was talking about changing over time. This tells me they lacked direction and it was time to get out. Confluent has never given me a reason to second guess their long term vision. Thesis should improve and evolve from here.

Maintaining their cash position the best they can and improvement in their free cash flow burn. I am not super excited about a cash burn of -$60 and would like to see this metric improve. If they spend more, I would hope they would put the appropriate context on it.

Confluent Wrapped Up

Confluent really is a great business, as it stands today, and I do think this is worth a watch list add. Long term, I can envision them improving their underlying business model to their long term expected goal.

Today, they are trading at approximately 10x next years P/S but analysts have them only growing 44% this year and 35% next year. This does not make sense especially as cloud becomes a larger portion of revenue. In this instance, I am led to assume that these estimates are conservative enough to work off of to provide a baseline valuation. To get an idea of where I think this stock is going by 2025 and to follow what I do with this company real time, consider becoming a member of BluSuit.

We have a Discord community where I regularly update everyone on buys, sells and what I am thinking about Macro. In addition, you get to watch me “put my money where my mouth is” which includes failures and wins, total transparency. I plan to do this for years in the future as that is my goal for my investments, years. Until next time…

Stay Tuned, Stay Classy

Dillon

I'm having a hard time understanding what exactly differentiates Confluent from its competitors, aside from being cloud agnostic? Apache Kafka is open source and there are competitors like Segment or MuleSoft (recently acquired by Salesforce) that seem to be doing the exact same thing. How can you tell that Confluent's product/service is better than the competition?

Trying to understand your thought processes here and learn from you.

Thanks a lot, Dillon & Thank you for this little insight into Confluent - keep up the good work :)