D-Local: The Small FinTech Taking Wall Street by Storm

D-Local: The Small FinTech Taking Wall Street by Storm

These quarterly results destroyed expectations

D-Local, an international fintech commerce company that benefits largely from two large secular growth trends; globalization and emerging markets.

Due to this being a new IPO, I want to make sure this publication is carefully constructed to grasp the entirity of this opportunity and business. This is the research I’ve done that I’ll be sharing with all of you today in this publication:

The scope of the market opportunity

D-Local business and competitive moat

Latest Quarterly Results

Current and forecasted valuations

My personal portfolio strategy moving forward

The market opportunity

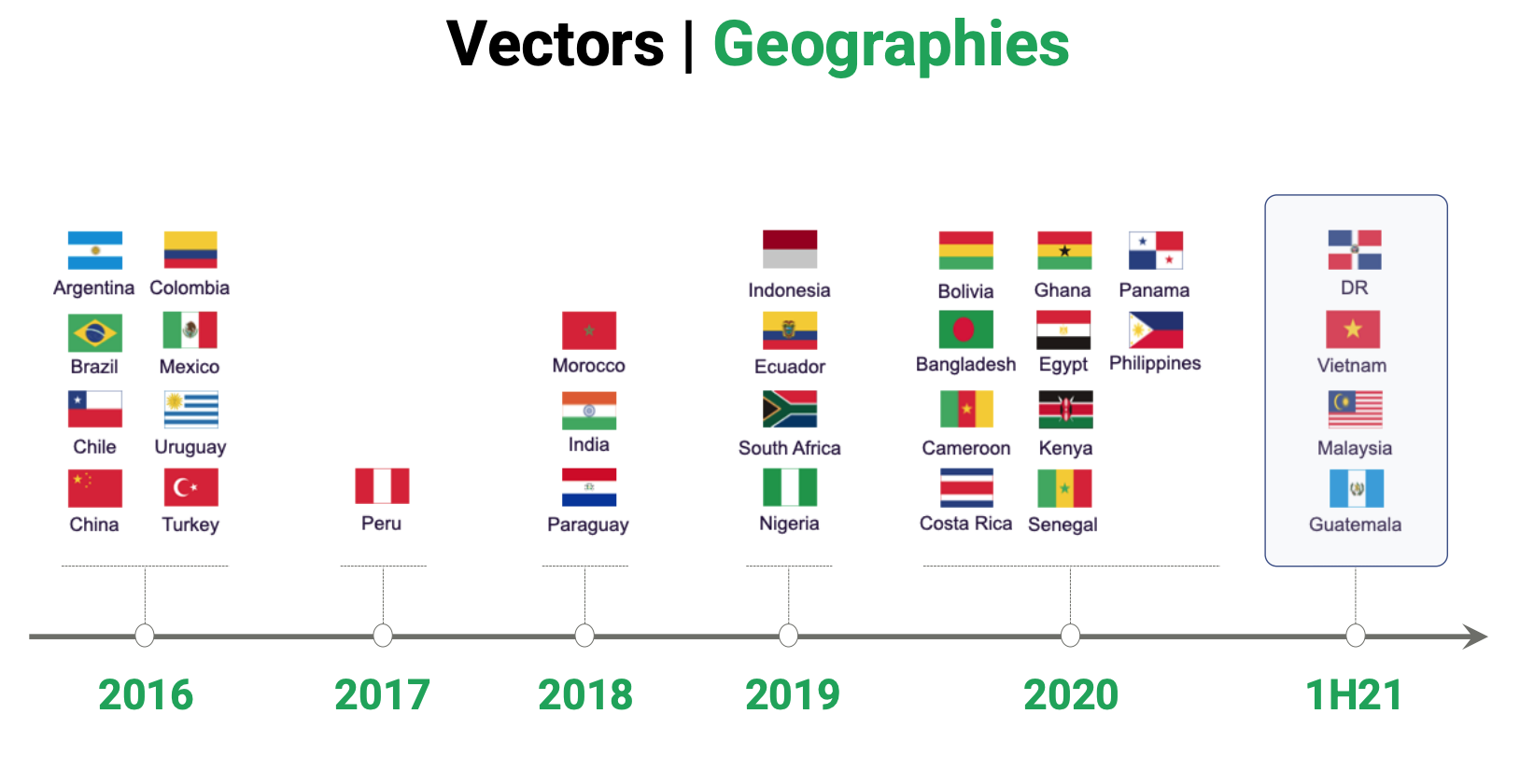

D-Local specializes specifically in emerging markets, currently they’re operating in 30-32 different countries since they began expansion in 2016.

The reason why this is important is that they’re enabling major businesses to do commerce in the worlds most up and coming countries. They live with the belief that their customers success in these countries is their success, which is true. The more payment volume their customers do, the more their customers make, the more they make because they take a % of the payment volume. This leads to a vested interest in their clients long term international performance. But, when it comes to an international market opportunity, exactly how big is it?

This is really where it gets exciting. They estimate that they’re operating at a $1.2T TPV (total payment volume) market, of which they collect a margin of approximately 4%-5% TPV. In terms of revenue, their current addresable market (assuming 4%) is $48B in revenue that they can do, today. This is expected to continue to grow at a 27% CAGR from 2020 - 2024 (this data they used was from 2020), which will put it at approximately a $3.122T TPV opportunity, or a $125B revenue opportunity.

Side note: they’re running 40%+ EBITDA which has the opportunity for $50B EBITDA. If you added a multiple of 30x EBITDA, this would equate to be a $1.5T company. This is assuming 100% market share, which is unrealistic. But the opportunity is there none-the-less. Maybe in 10-20 years, right?

In other words, this is a massive market with a massive opportunity and exponential growth. They’re projected to do about $240m+ this year. This means that this business can experience exponential 100%+ YoY growth for years, and years, with limited competition. There are only a few companies who do exactly what they do and focus on emerging markets.

D-Local business and competitive moat

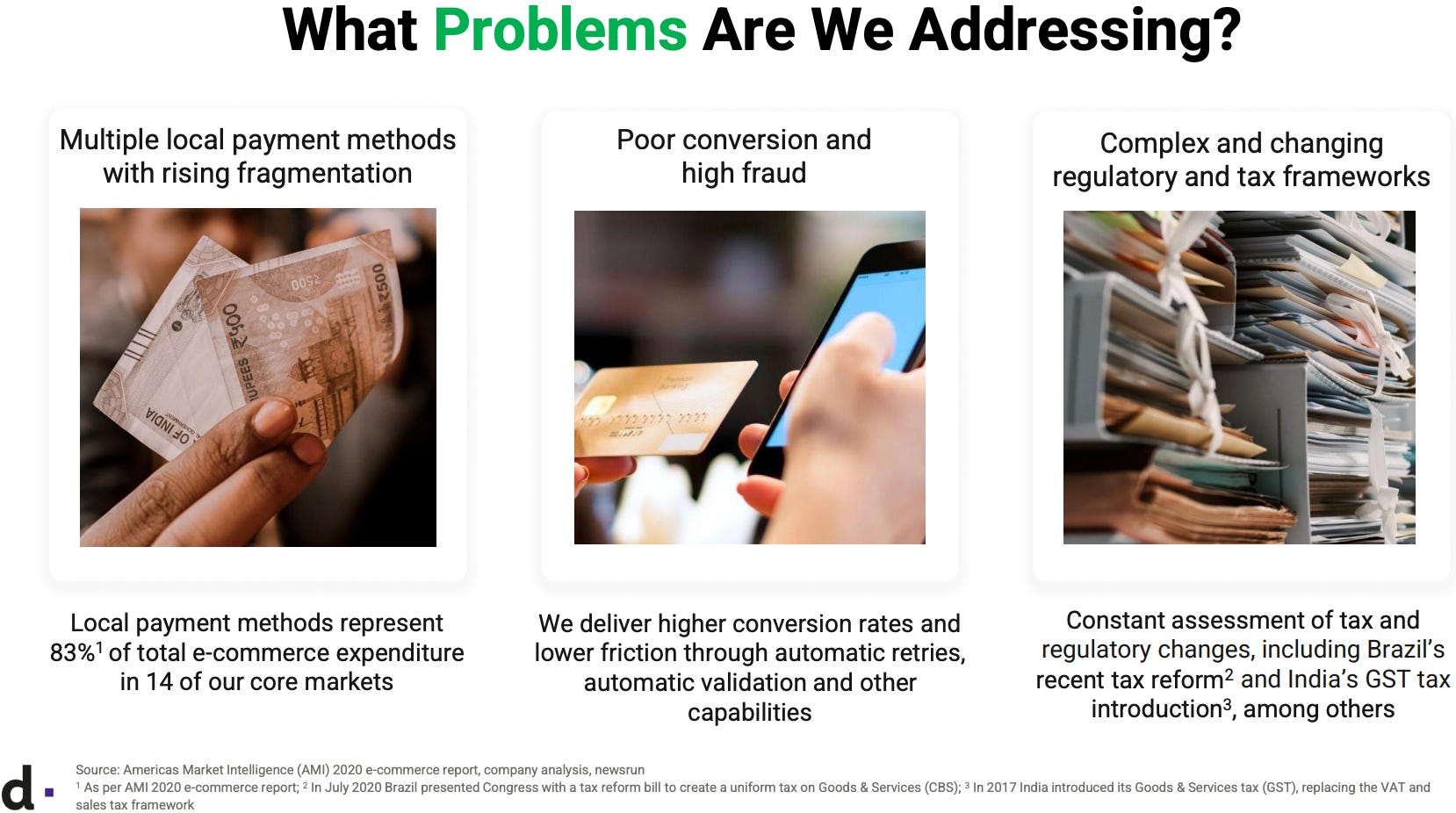

When investors typically say FinTech, their minds can go to PayPal, Square or some other payment opportunity. But that’s not exactly what they’re doing. They enable commerce business to get paid (pay-in) and to make payments (pay-out) to customers and employees internationally.

Their offering goes substantially more in depth, but if it was summed up how they help their clients, they reduce the friction and risk of making cross boarder commerce payments. In emerging countries, they often have multiple steps and processes they need to take to receive and send money. DLO makes it possible for these merchants.

Let’s take a minute to talk specifically about a few use cases they provided to cover exactly what Pay-In is and what Pay-Out is. Also, categorize exactly what commerce means because it’s not only e-commerce.

Pay-Out Example: DiDi (China’s Uber) works with DLO to pay their drivers. They help with taxes withholdings, bank transfers and split payments for their drivers to collect fairs.

Pay-In Example: A large streaming company they work with offers their service in Puru. DLO helps the large streaming company offer their product but enabling acceptance of local currency.

When we talk about commerce, it goes much deeper than only e-commerce (although they do that too). They enable social media platforms, video streaming, ride hailing, e-commerce, and anything that requires a transaction from an international company to an end user. Their client base is any business that wants to do business in another country.

When it comes to their history, this is important to know because it touches on their competition and their competitive niche. Originally, they were a division of a business called AstroPay but seperated from them in 2018. AstroPay has a subdivision that does something similar to D-Local, called Directa24. However, where they differ is that AstroPay and its subdivision, Directa24, operate primarily in South America and India where they focus on ForEx, online gambling and adult entertainment. D-Local does not do this, which is why they have clients like Amazon, Microsoft, DiDi, Dropbox, Nike and Uber. In this case, they’re one of a kind.

Latest quarterly results

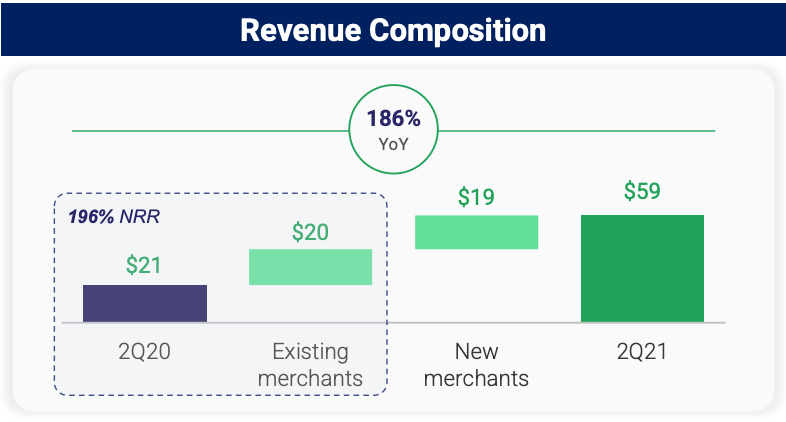

Their results are nothing short of impressive, let’s cover some topline metrics.

These metrics are absolutely best in class and extremely hard to find. A 44% EBITDA margin coupled with 186% YoY growth (slightly impacted by a slow down in last years COVID related numbers) is nearly impossible to find. Throw in a 196% NRR, meaning their clients spent 196% more with them YoY, makes it have better metrics than another super stock on the market today, Snowflake.

They did mention on their quarterly call that they do expect to see a slow down to a more moderate NRR level of 150% - 160% and EBITDA of low 40% which means it’s relatively predictable to gauage their growth. Speaking of growth, they broke it down to two categories; existing clients and new clients (they classified new clients as ones obtained within 12 months).

They did mention that they added 10 new clients last quarter alone and that their pipeline remains “extremely healthy”. It’s important to note is that the “new merchants” column is the vector that provides the most opportunity for growth. With their NRR estimated to be between 160-170% in the future, they’ve proven that they can grow their business in a sticky fasion. As an investor, unpredictability and unaccounted upside is how we see large periods of multiple expansion which is why it’s important to pay attention to how many new clients they obtain. There’s a case where DLO accelerates growth after becoming public due to these potential new clients becoming familiar with their product offering, which they said was a big reason why they went public in the first place. It’s all about exposure.

Valuation

DLO traded up to an $18B marketcap, but it could quickly go to $20B. For this reason, I will use $20B as the basis for these forward valuation metrics. I will also use a base case of 40% EBITDA to show the forecast for earnings growth.

2021 revenue expected to be $240m @ $20B marketcap:

83x P/S, 204x EV/EBITDA

2022 assuming 100% revenue growth, $500m @ $20B marketcap:

40x P/S, 100x EV/EBITDA

2023 assuming 80% revenue growth, $900m @ $20B marketcap:

22x P/S, 55x EV/EBITDA

DISCLAIMER: I am not a financial advisor or analyst, these are my numbers I am sharing for educational purposes only. These can change!

The key take away from these valuation metrics is that it’s currently valued so high due to the anticipated future growth. When you have a business that has a seemingly unlimited runway for growth it almost appears cheap where it’s trading at right now. For this year’s forcast, they expect to grow 134%, which is higher than my 2022 case of only 100% and 2023 case of 80%. Needless to say, with this overall market opportunity and the potential for new clients, there’s room for upside surprises. Especially as this business is in the early innings to what seems to be a long term, secular growth driven, company.

My strategy

I plan on making DLO a position as big or bigger than my Upstart position and would be comfortable making it my top 3. I currently have it at 60% and will add on any weakness. Rarely, there are investment opportunities like this that come along that can be once in a life time. The combination between high growth and profitability makes this have all the odds in it’s favor of becoming a large multi-bagger, possibly tomorrow’s MELI.

I hope you guys enjoyed this, if you did consider subscribing and follow us on Twitter and YouTube (just go to my Twitter and it’s all there).

More multi-baggers to come.

Stay tuned, stay classy…

Dillon

Thanks for the write-up Dillon! The valuations look very interesting now with the recent downturn...

Hi Dillon, Are these revenue estimates on 2022 and 2023 are fair estimates or the best case scenario? Do u mind sharing how you arrive this 204x EV/EBITDA.