Deep Dive: 2/3 Hyper Growth IPO's

Deep Dive: 2/3 Hyper Growth IPO's

Unknown, not covered and massive potential. Our second IPO we're adding.

IPO’s offer exciting opportunities to discover businesses others are not 100% aware of, just yet. It takes an enormous amount of time researching a new business to understand the long term potential and challenges.

But, if new IPO’s are picked successfully before the market prices in its full potential, the rewards are tremendous. Here are a few examples of returns so far among this years best performing businesses:

Global-E (A BluSuit call out at $27/share): YTD gains 212.4%

Agrify (BluSuit call out at $13): YTD gains 85%

Upstart (BluSuit call out at $110 & $85): YTD gains 506%

DLocal (BluSuit call out at $30): YTD gains 109%

Digital Ocean (BluSuit call out at $55): YTD gains 72%

A few missed IPO’s:

Monday: YTD gains 112%

Doximity: YTD gains 87%

I’m sure we’ve missed a few more, but those stick out to me the most. However, I’m committed to continue finding these hyper growth businesses when new S-1’s are filed and begin a position before the market prices in its full potential. I will continue to share this research with all of you.

The business covered today has it all from operational excellence, unrivaled profit margins, exponential growth and a distinct competitive advantage. The IPO date is not certain yet, but when I know I will let all of you know.

A quick recap of all three IPO’s I’m talking about in this 3 day series. This article and the Remitly will be exclusive for members only, due to wanting to keep excitement limited. The next one, which will be published tomorrow at 6:00 pm EST will be ForgeRock and available to everyone. But, in addition, I wanted to bring a few other IPO’s to all subscribed members attention. Top and Bottom line financials of all upcoming IPO’s that can be good investment opportunities:

New companies coming public soon that I did not bring up yesterday are Toast, Brilliant Earth, and EngageSmart. All of them have impressive financials and future opportunity. In just my opinion, I think the best opportunity is in Olaplex and Remitly. But, my knowledge is limited and the other 4 can represent wonderful investment opportunities.

Olaplex: The Complete Hair Repair Driven by Salons and Proven by Science

Overview of the Business Model:

This should be thought of as a beauty first technology company and not just another hair product company. What they specialize in doing is innovating new products that customers and Salons swear by. 76% of stylists believe Olaplex offers superior products and they have a whopping 71 NPS, which is a measure of a businesses stickiness and brand loyalty.

The way Olaplex describes themselves, “OLAPLEX is an innovative, science-enabled, technology-driven beauty company.” Their patented technology/ingredient is Bis-aminopropyl diglycol dimaleate (“Bis-amino”), which they use across their products and believe why they’re able to generate superior customer satisfaction in comparison to their competitors. Essentially, this product is proven to promote hair health and can repair dry, dead, hair from bleaching and coloring. They also mention that there are claims Bis-Amino has application in skin care and nail health.

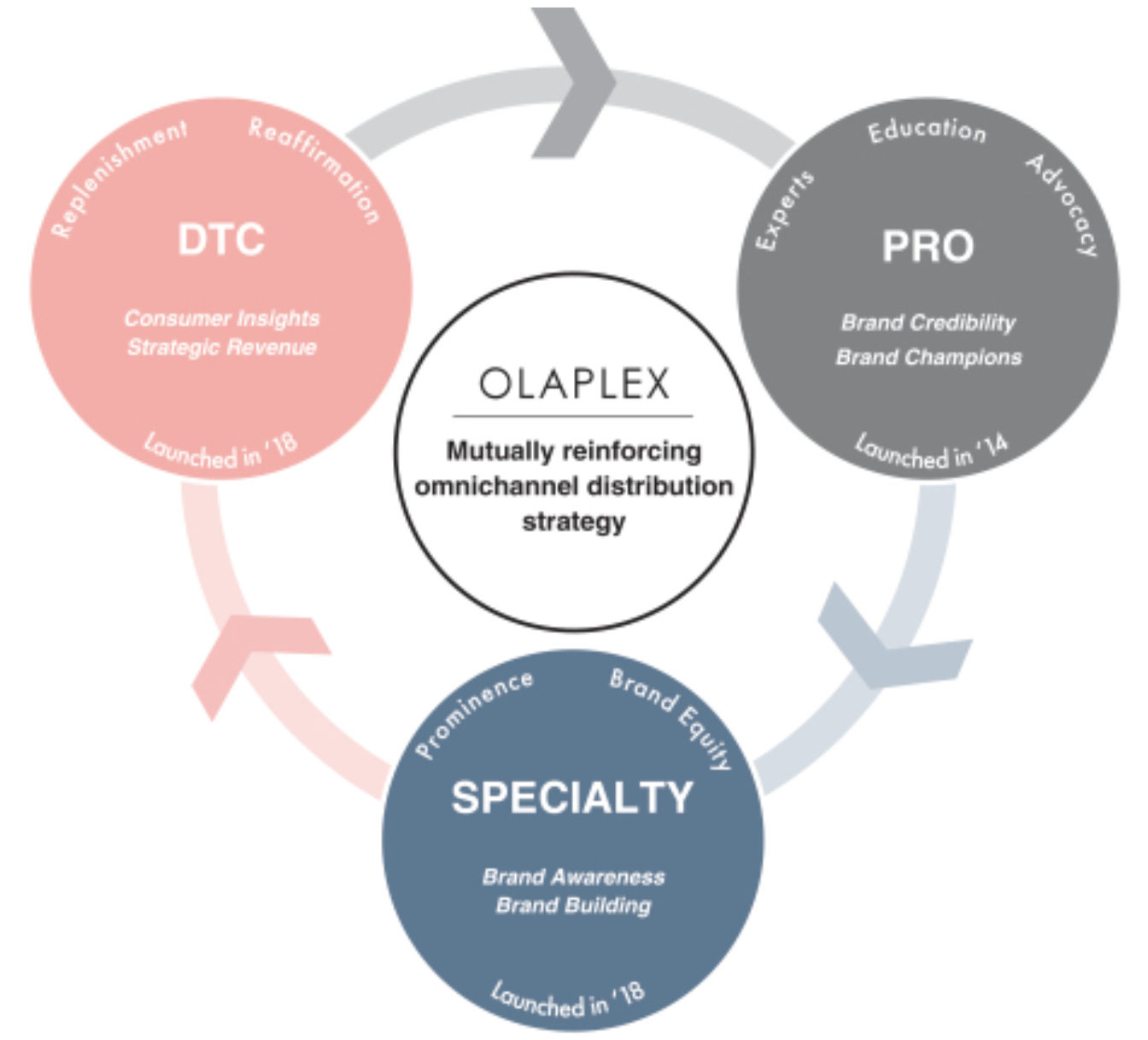

Their business model depends heavily on maintaining a direct relationship with their salon partners, who they view as being instrumental for feedback on their products and new product ideas. This is an extraordinary approach. If you get the professionals to buy in, this heavily enables a DTC approach and gives you pricing power. They sell their products through three channels: direct to consumer, specialty retail and professional (hair stylists). Stylists consist of 55% of their total revenue and grew 59% YoY. Specialty retail, primarily Sephora consists of 18% of their total revenue and grew 75% YoY. Direct to consumer, which is primarily e-commerce and their fastest growing segment yielding 260% growth YoY and represented 27% of total revenue.

They began selling their products in 2014 but only worked with Salons/Professionals. Four years later in 2018, they finally opened their product line for direct to consumer. However, what’s interesting is that they only had 3 products until 2014 but have expanded their product portfolio substantially over the past 3 years to reflect different use cases.

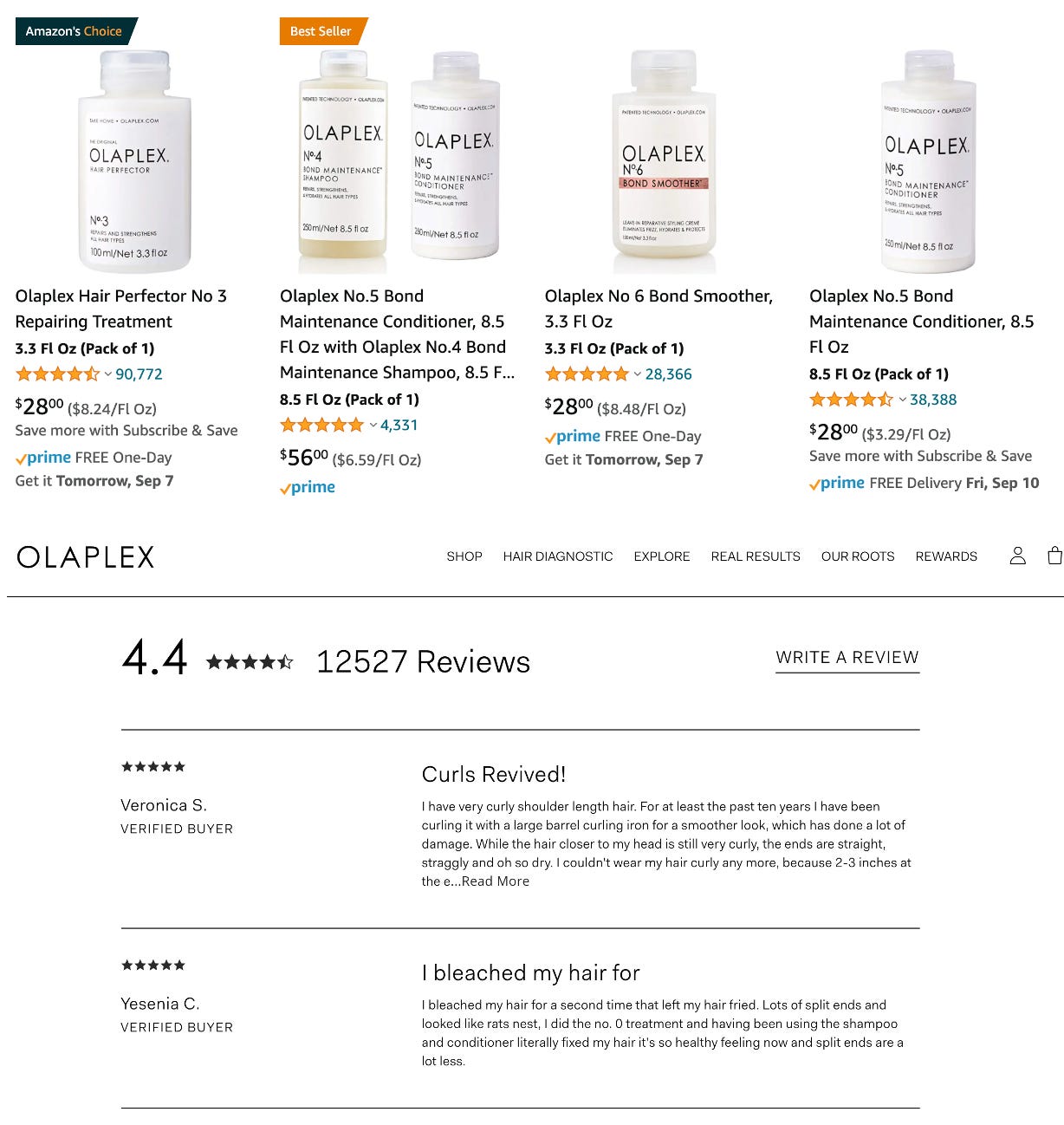

An expansive/innovative product portfolio with hyper growth on the top and bottom line always suggests they’re doing something right. With 27% of their revenue being from their e-commerce channel, I had to check customer reviews. To me surprise, it validated what the NPS score suggests. There are tens of thousands of testimony’s on Amazon and on their website.

You can find more reviews on Amazon and this is only a few.

To summarize their business model; they’re extremely successful selling their product which is sold in 3 different avenues: DTC, retail, and e-commerce. They have a unique product with patented technology that’s backed by science and tens’ of thousands of testimonials. They focus primarily on the professionals in the Salon’s as partners. This is important because it allows them to hear feedback and come up with new product ideas to deliver to their client base.

Total Addressable Market & Competition:

There are rising trends in the Haircare industry which include many technological innovations that directly damage the hair. Trends such as dying (changing hair color), styling and various products. The need for new products to protect and promote hair health has never been higher. Olaplex is best in class among a moderately crowded group:

Henkel AG (OTCPK: HENKY)

Kao Corporation (OTCPK: KAOCF)

L’Oreal S.A. (OTCOK: LRLCF)

Unilever (UL)

Remember, 76% of professional stylists consider Olaplex as higher quality than other brands. This gives me confidence that there’s a clear competitive advantage.

Based on Grandview research; with the rise of the influencer, hair styling trends are expected to continue growing at a 3.1% CAGR to a total addressable market of $211B by 2025. Their S-1 mentions that today, their current market is $77b and expected to grow at a 6% CAGR till 2025 which is slightly different than Grandview. This is fueled by new independent Salons globally and men moving toward adopting hair care products.

Being the best in a $211B market with an expected $500m 2021 revenue run rate means there is significantly more room to run. This represents a .2% market share and it’s rationale to think they can obtain 5-10% globally. This would represent $10.5B - $21.1B in revenue at near maturity. The opportunity at this stage is massive and has 10x multi-bagger potential.

Past Financial Performance:

Normally, I would dismiss haircare products but the financials are arguably the most attractive metric I’ve ever seen. However, another business that I own, with an incredible financial profile, that operates in the ‘vanity market’ is InMode (INMD). Olaplex beats and exceeds InMode from a revenue growth and margin profile. InMode has currently risen 885.85% from 2019 IPO, exactly 2 years ago.

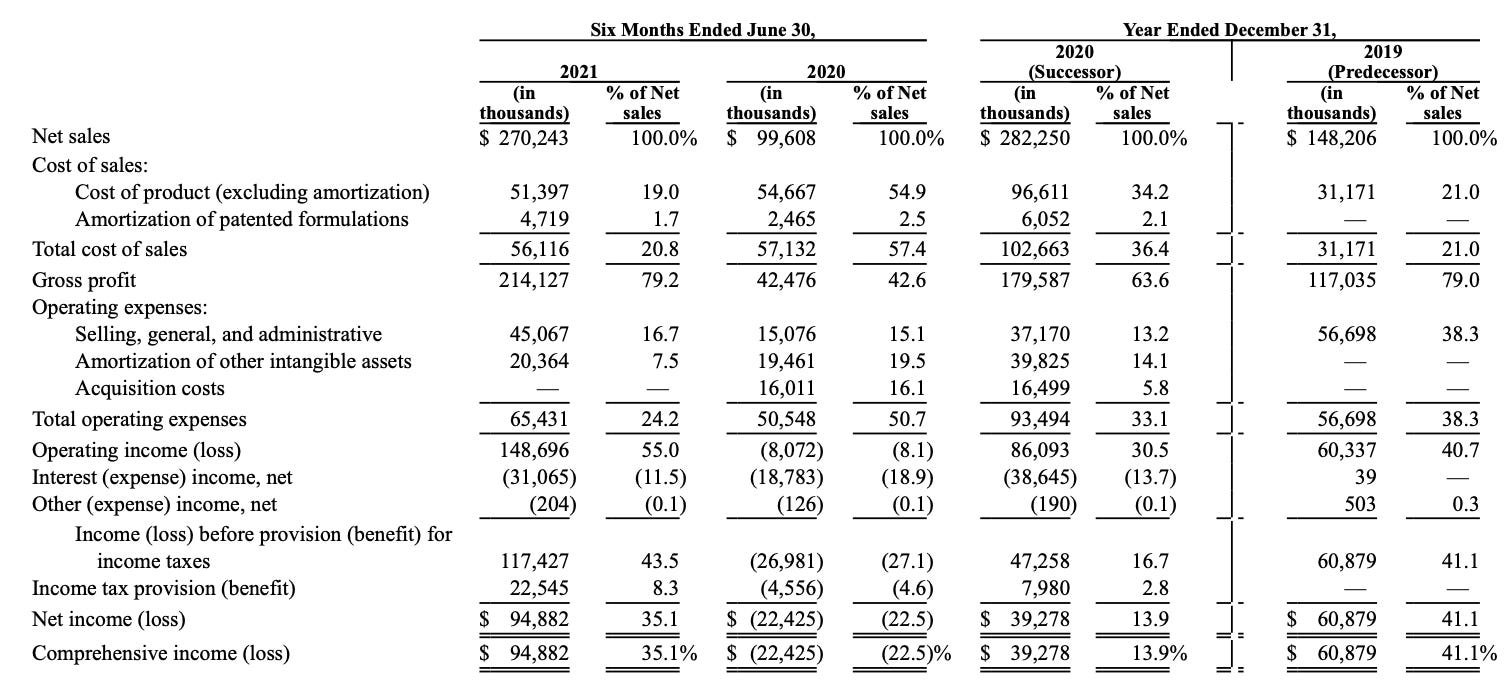

A few key highlights here on the income statement. This currently represents:

171.3% revenue growth YoY, 2020 saw 90.4% even during a pandemic and Salon’s being closed down

Gross profit grew 404% YoY, faster than the revenue growth which means margins normalized to pre-pandemic levels. 2021 Gross Margins 79.2%, 2020 Gross Margin 63.63% , 2019 Gross Margin 779%.

Operating profit 55% in 2021, which improved from 2019 and 2020 which is 40.7% and 30.5% respectively

Net income positive with the exception of 2020. In 2021, this represents a net-income margin of 35%

Due to the “quality” classification of their product, it appears they have substantial pricing power to have such a profitable business model.

Leadership’s Growth Goals:

In my last member article, I mentioned it was important to understand exactly what business Remitly was in. This has a very strong comparison in the sense that this is not just a hair care business with the products that it has today. It is a beauty company that specializes on producing high quality products. This mean it has the opportunity to leverage the existing clientele it’s developing now, for years. An example is Unilever, $UL, that we can draw comparison to as a similar beauty company. They currently do $52B in sales and $5.62B in earnings. Compared to Olaplex $500m revenue run rate this year. This beauty first opportunity is what we’re working with. Leadership just needs to execute with the wind at their back.

Leadership outlines their growth goals as the following:

Grow brand awareness and household penetration: They believe they currently have 45% target audience brand awareness compared to 69% peer benchmarked and 11% of total Sephora customers. They plan to continue leveraged their network and social media community, where their instagram currently has 1.2m followers.

Continue to grow through the existing three points of distribution; DTC, Retail, and Professional: They believe they still have significant runway to continue growing into all three channels by growing professional customers, bringing brand awareness and more importantly, driving more customers to their website. They mention they want to enable e-commerce capabilities, specifically their “hair diagnostics” portion where they have received more than 1.3m inquiries about their products.

New geographies and retailers: They see substantial opportunity expanding their international footprint. They plan to expand to their distribution partners in China and Europe, as well as Latin America. I see this as the largest opportunity in terms of expanding TAM.

Expand new innovative products and capabilities: They believe they can continue to expand into various scalp treatments and other hair products. But, more importantly, 82% of Olaplex familiar customers want to see Olaplex expand into skin care and 51% said they’d switch to Olaplex. They are focused on moving toward non-haircare products.

Expanding into new products and capabilities makes me the most excited. I always want to see businesses expand into new offerings but cross sell to their existing clientele and leverage their unique market and brand proposition. However, the expansion of the international footprint appears to represent the largest short term expansion of TAM.

Conclusion:

I have always considered myself more of a tech investor but when you see innovation at any level with extremely impressive margins, you can’t help but jump at the opportunity. Olaplex represents a business that can yield incredible share holder returns. I will be adding on IPO day, along with Remitly, and believe both of these are in the same category as Global-E and DLocal, as far as it goes with the future potential long term returns. This is a very exciting business.

Stay tuned, stay classy

Dillon

do you have any information about approx timeframe for IPOs for Olaplex and remitly?