Deep Dive: 3/3 Hyper Growth Cyber Security IPO

Deep Dive: 3/3 Hyper Growth Cyber Security IPO

ForgeRock (FORG) is IPO'ing soon at a $1.9B valuation, you're going to want to know this one

ForgeRock (FORG) has filed for an IPO, offering 11m shares with a price between $21-$24 per share. This would put it at a $1.9B valuation. This will likely go up from this price on IPO day, depending on market conditions.

Speaking briefly on current events within the markets, it appears the chances for a market correction are becoming increasingly more likely. When looking at the S&P 500, it has now been over 365 days since the bottom of the last correction, a 10%+ down. The NASDAQ saw somewhere between 10-12% down earlier this year in February/March. Needless to say, we are over due to maintain overall market health.

With my personal portfolio strategy, I always take market exposure down to 100% (no leverage) while accumulating and saving cash. This is a way to participate in the broader market rally but patiently wait for excellent buying opportunities in some of the best businesses I can find. If it doesn’t happen now, I can still wait for valuations to come back down to earth. A few stocks I have high on my shopping list:

DLO under $50

GLBE under $45

PATH around a $20 - $25B market-cap

Both of the IPO’s mentioned in the first 2 member’s letter

FUBO in low $20’s

LSPD below $90

This is obviously subjective to my personal portfolio strategy and depends a lot on my cost basis, position sizing and portfolio allocations that I already have within my portfolio. One thing I’ve learned about the markets over the years, if you think a price can’t get back down to a certain level, it probably can. When prices become mind boggling and valuations are so low, this is the time for maximum long term opportunity.

But, markets aside, I have an exciting opportunity to share with every one!

ForgeRock: Cloud IoT and Digital Identity Platform

Overview of the Business Model:

A security and identity management business, ForgeRock is a global leader. When thinking about “identity”, this common terminology wouldn’t necessarily apply in the digital world. Identity can consist of people and things, or really any thing with a digital footprint. By modernizing the digital user experience, their platform allows people to log-in without any risk to security and compliance and, in addition, improve it.

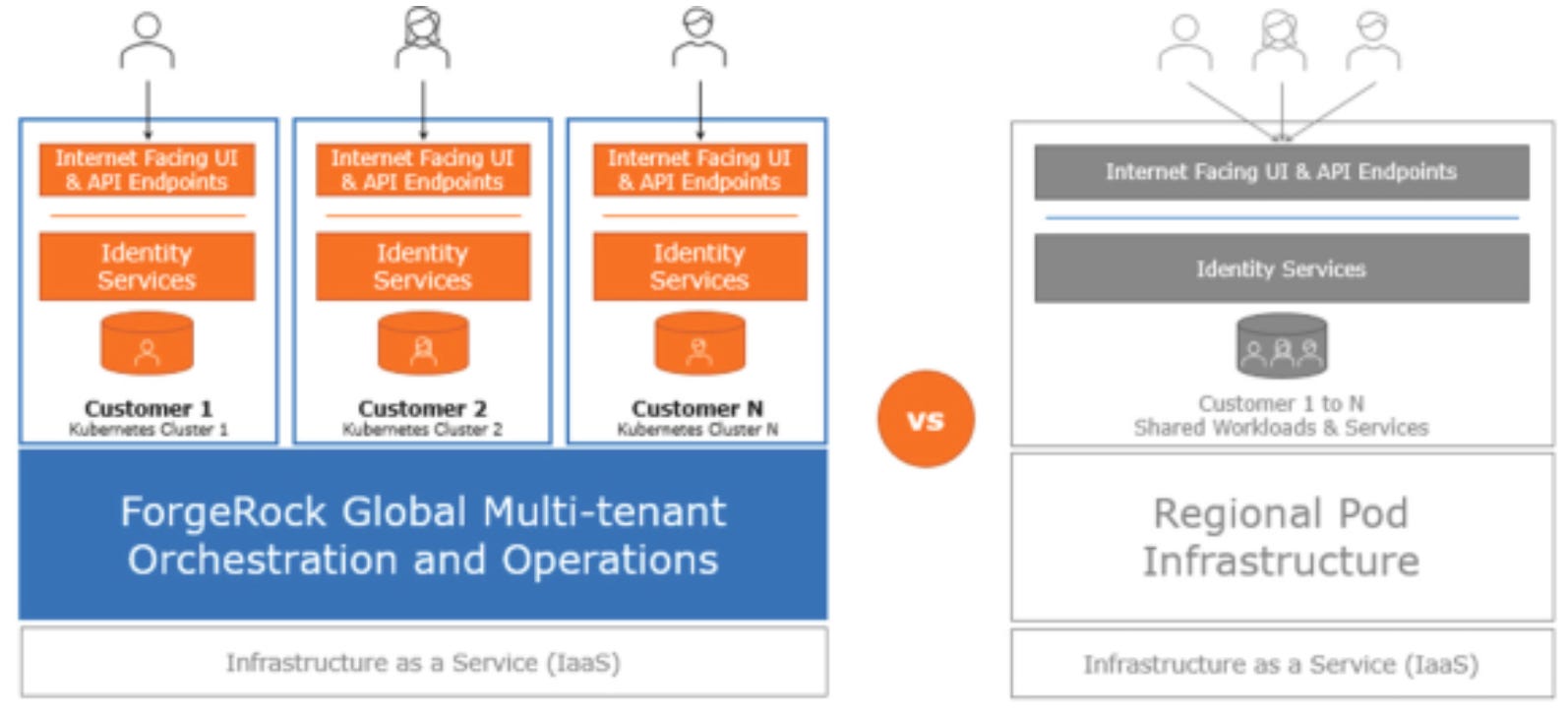

They are a cloud first SaaS business that focuses on a subscription based model, much like many of the other SaaS businesses we see on the market today. The reason why many of these companies have yielded great returns for investors since IPO is a direct result of the best in class stickiness this revenue model provides. Especially being cloud based, they classify themselves as “Next Generation Cloud Identity” replacing many of the clunky, on-prem, legacy systems. This enables scale and can handle high work loads.

Coming back to identity being anything with a digital footprint, it is important to understand exactly what this means because it opens up a better idea of the present and future opportunity.

Every industry and every business has various users of identity. This can be consumers you work with, employees, partners, API’s, micro-services, devices, and internet of things (IoT). ForgeRock platform helps enterprises through the services of:

Identity management: Facilitates with the life cycle of an identity from initial set up to departure.

Access management: Secure and simple access management to identity’s

Identity governance: Manages users access to applications, data, devices. Basically the security arm of identity management, preventing people/devices from getting to places they shouldn’t be.

Autonomous identity: A view of access, processes and risk reduction to digital identity’s

If all these identity’s are not managed correctly it can inhibit an enterprise from growing and scaling successfully. The alternative to successful management is poor customer experience, user productivity issues, and security risk.

In its very simplest explanation, ForgeRock customizes and enhances an enterprises ability to manage various different types of identities (identity meaning anything with a digital footprint) to enable better security and operational performance to both protect and enable a businesses goals. This is necessary because as the world becomes more digital, there are a ton of new “identities” and businesses that need a way to manage everything. ForgeRock comes in and gives their customers better flexibility, scale and safety (preventing cyber attacks).

Total Addressable Market & Competition:

When it comes to SaaS and especially anything that would fall under a businesses technology arm, I love to use Gartner. Let’s briefly break down exactly what each quadrant means and how you can leverage it as an investor:

Challenger: Typically runs a strong business and is competitive in pricing. This can be a good investment, Shopify is a challenger.

Visionary: Usually very innovative and can have best in class tech, especially the further to the right they go. This depends all on revenue & revenue growth.

Niche: They operate in a very niche market and niche segment, typically investments I stay away form.

Leader: Typically the market leaders that are paving the way for the rest and offer the most robust capabilities and efficient pricing structure.

ForgeRock has some really big competitors in this segment. However, it is important to note that this is only access management rather than identity and access management. Below is the Forrester Wave, which is similar to Gartner where it provides business and technology research.

In both reports, you can notice that one of the main competitor to ForgeRock is Okta and a few other big players like Microsoft. Needless to say, this is a very competitive space. Where they really separate themselves is through combining the solution between identity, management and security.

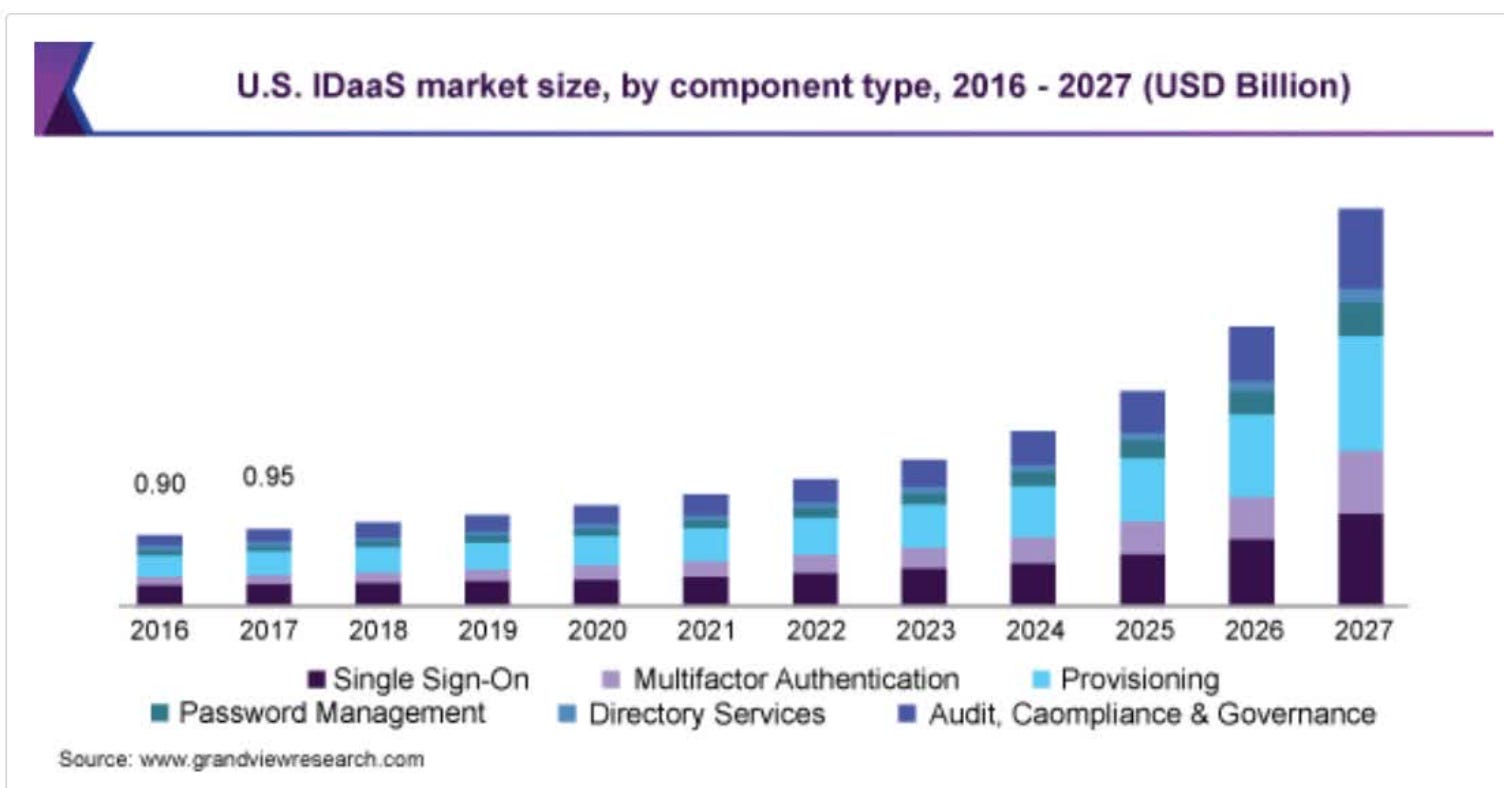

According to Grand View research, the identity as a service market was $3.34B in 2019 and is expected to grow at a 22% CAGR till 2027 to $16B.

IoT and digital identities are in the very early beginning. However, there are very big competitors that ForgeRock will have to go against now and for the foreseeable future.

Past Financial Performance:

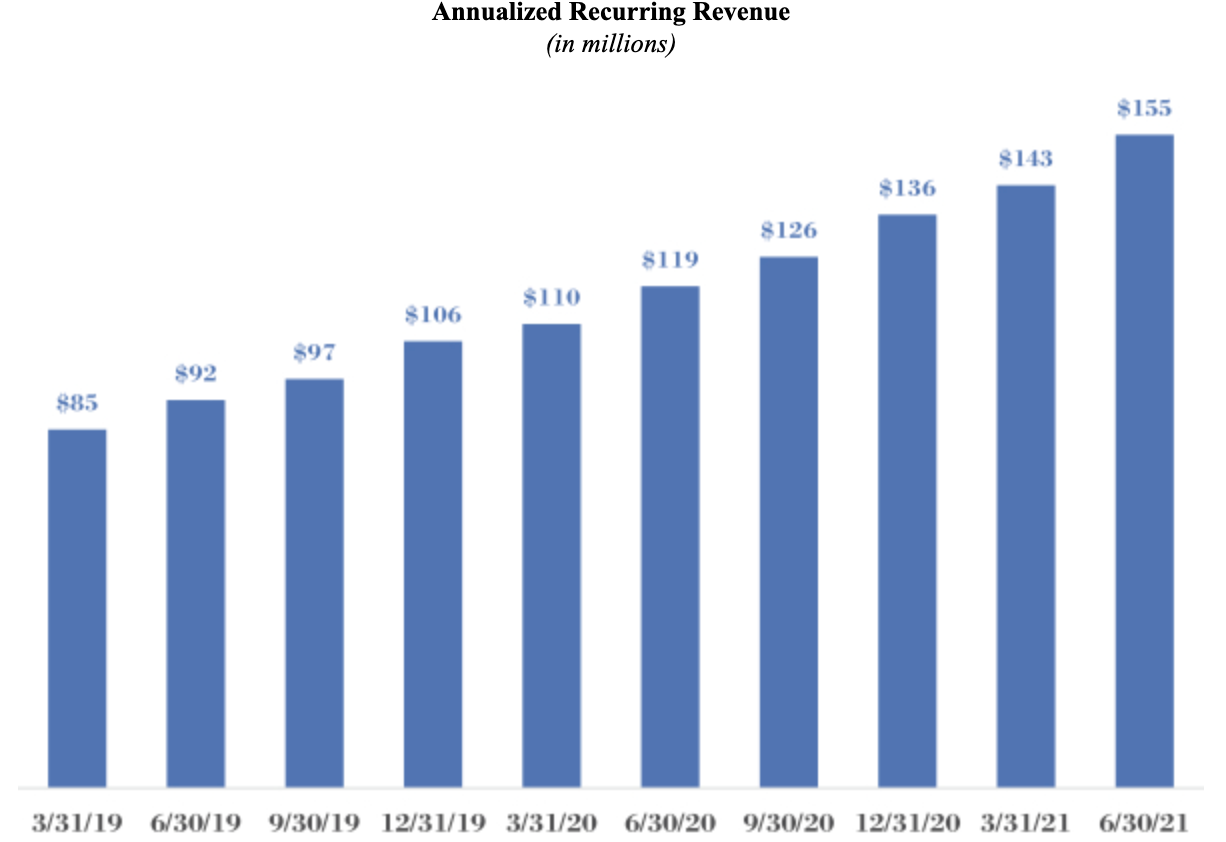

Their growth and margins are definitely the most impressive thing about ForgeRock. They have consistently grown from an ARR perspective and run 83% gross margins.

I did notice that there were times their growth did slow down which included back in 2019 and during the COVID lockdowns. Typically this is concerning when I see this from a SaaS business. I always like to see consistent, strong, growth. This tells me they MIGHT (but still could) not have a mission critical product, or can be inundated with competitors. However, typical cyclical seasonality exists with many of these businesses meaning Q4’s revenue can be higher than Q1 due to budgeting cycles of their customers. But, below, you can see June 30th, 2019 which brings the most attention.

Their explanation for June 30th, “June 30, 2019, compared to the three months ended March 31, 2019, primarily due to a decrease in subscription term licenses and a decrease in perpetual license revenue in the three months ended June 30, 2019.”

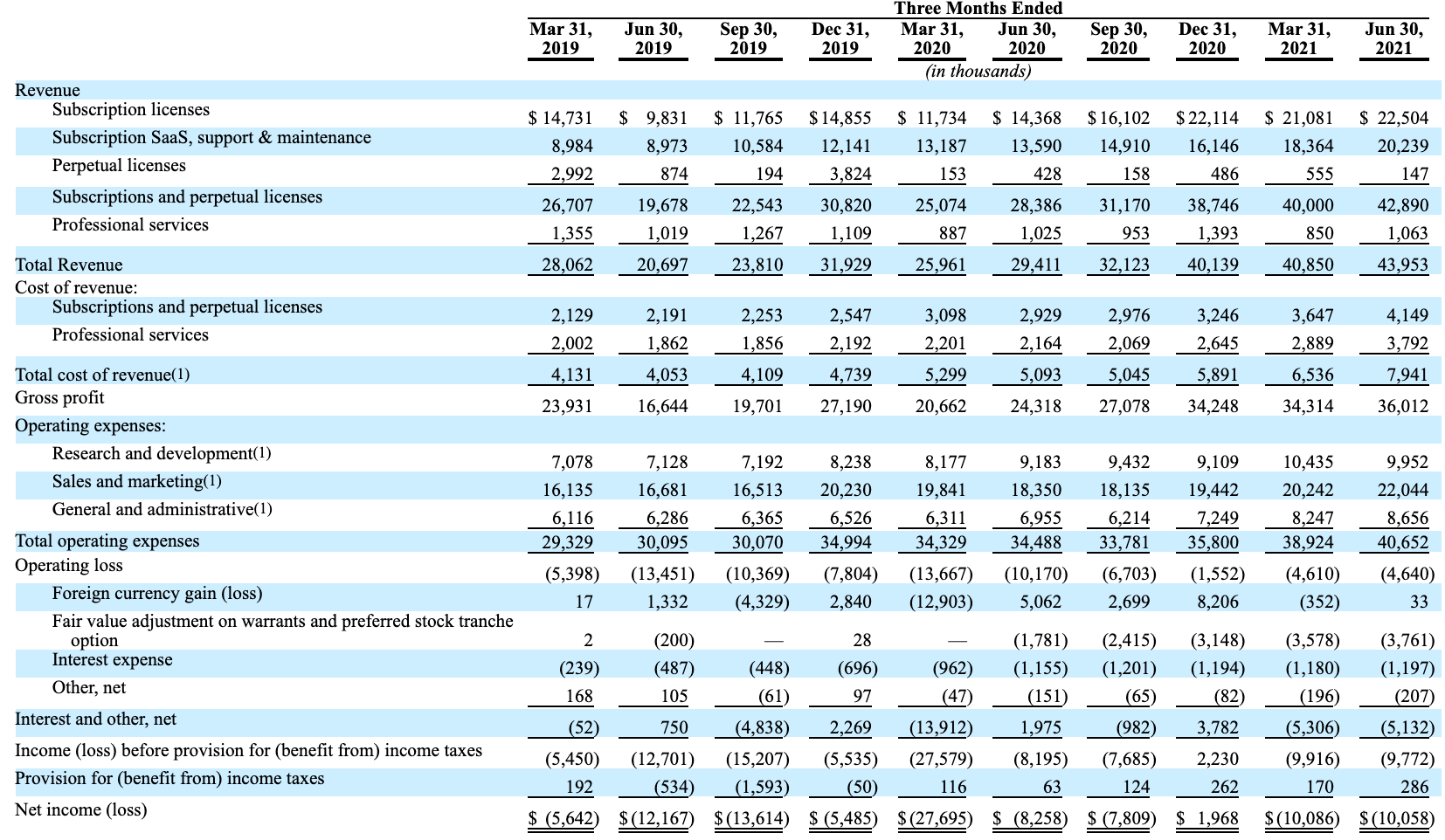

On a positive note, their top-line results for the latest quarter show some very strong path to profitability and growth. The results of the first 6 months of 2021 compared to 2020 looks like:

53.2% revenue growth YoY

113% net revenue retention

Gross margin 82.93%

Operating profit of -10.9%, up from last years operating profit of -25.1% showing a path to profitability

Net income -$20.1m but have improved as a % of revenue: 2021 -24% vs 2020 -33%. Further suggesting path to profitability.

Cash flow from operations are negative but also showing improvement

The trend toward profitability in a SaaS business with a net revenue retention of 113% is always very interesting and can lead to great returns for all investors.

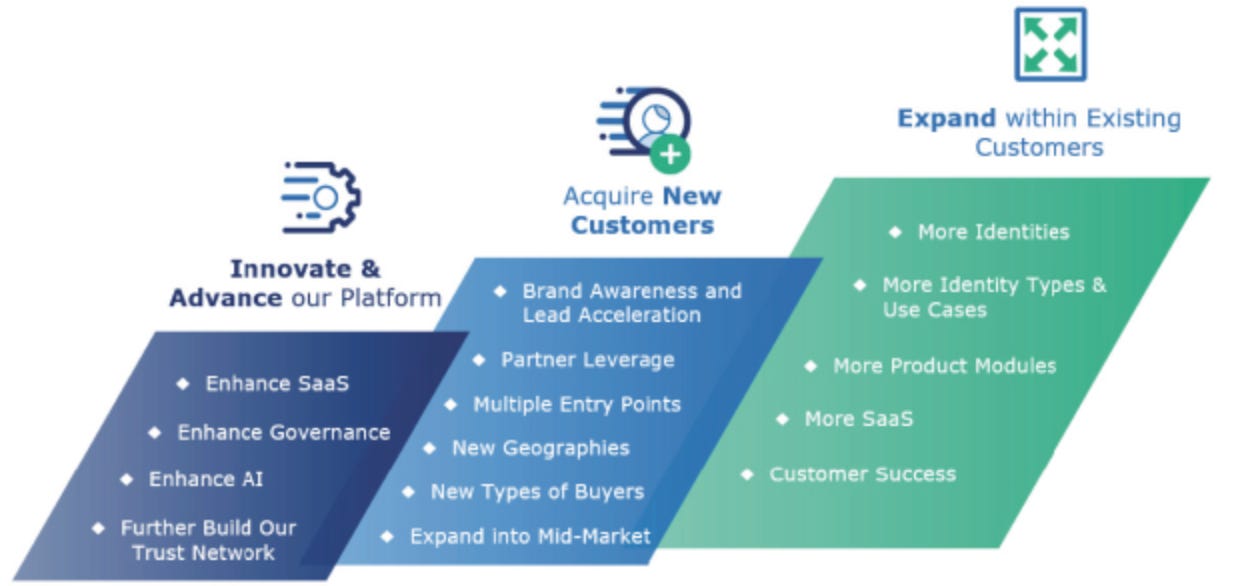

Leadership’s Growth Goals:

The market growth in itself should continue to lead to tail winds for ForgeRock, recall the 22% growth rate. However, they are competing and mentioned in their S-1 they need to continue to innovate for growth. They outline their growth strategies in really three key components.

Innovate and Advance their platform: They’re seeking to enhance SaaS, Governance, AI and their go to market strategy. From a technological and innovative perspective, I see large potential within their AI strategy. There are two other security platforms, CrowdStrike & SentinelOne, that use AI at the root of their offer for predictive and decision making capabilities. AI is truly the future.

Acquire new customers: They currently have a global presence in certain regions, but they’re looking to expand into more countries. The exciting thing is that there’s also an opportunity for them to expand into the SMB market because they’ve primarily focused on the enterprise.

Expand within existing customers: ForgeRock is seeking to expand their capabilities and cross sell their current/new solutions. This is a typical “land and expand” business model that most SaaS companies do.

Conclusion:

ForgeRock is one I’m putting at the top of my watch list, but will not necessarily be adding right away. The reason why; competition. I like to see a distinct competitive advantage or difference among similar businesses and competitors, I don’t see that here today. This can obviously change and most likely will over time, which is why I want to track this business and keep it top of mind.

I always like to say to new investors I mentor, “You don’t need to buy today. You can have that capital in a higher conviction business and watch how the story develops. It’s never too late to buy a good business.” I think i’ll take my own words of advice here and allocate precious capital to the other two IPO’s I covered in the members only letter.

If you guys liked today’s content, don’t forget to like, subscribe and share on Twitter or anybody who would be interested!

As always guys, stay tuned.. stay classy..

Dillon