Defensive Options Trading

Defensive Options Trading

Options are usually thought as a way to yield high return, but let's talk about how it can manage risk and generate cash

Options trading and cash flow:

To those unfamiliar with this type of trading strategy, can be chopped up to playing a big role in GME’s short squeeze. Or, it can be thought of as a way to YOLO, generate serious gains, and can be a gamblers way to participate on the financial markets (not saying that’s wrong). But this publication is about how important options can be in the long term, investor like, portfolio strategy. To make this universally friendly for various experience levels, let’s cover a few things.

Options can be broken down into two types; call options and put options. An option is essentially a contract to buy or sell a stock at an agreed upon price at a specific date in the future. These “options contracts” have a market of their very own where you can buy and sell them separately from the stock market. Basically, it’s the options market. This means you can buy a contract, receive a gain/loss on it, and sell that same contract without any commitment to the stock it’s attached to. When you sell a contract (a form of shorting) you can buy it back at a later date with a gain/loss.

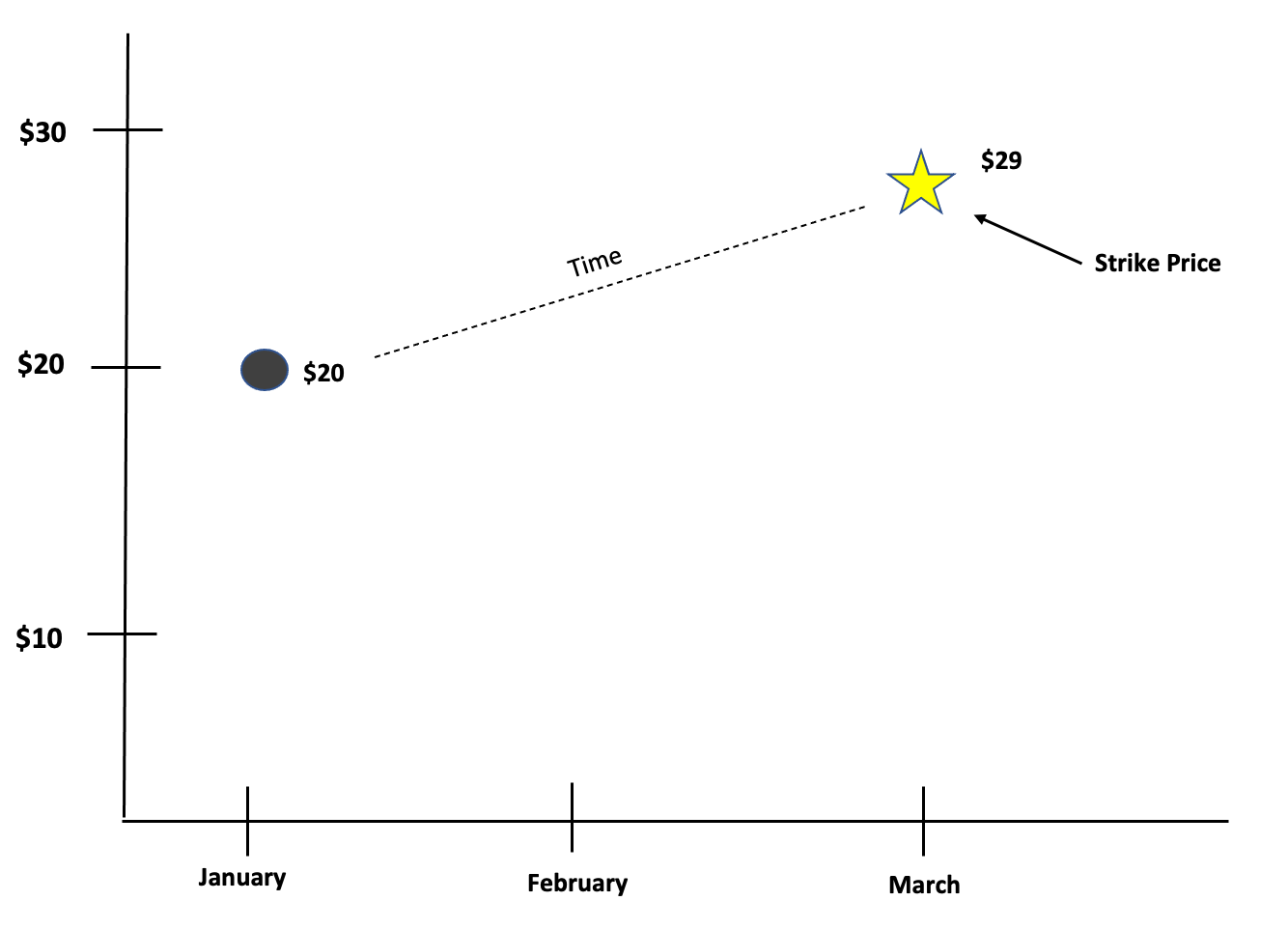

Call options have unique fundamentals where you can buy and sell contracts. When you buy a call option, you pay a premium (think of this as the value of the contract) that basically tells the seller, “I will buy the stock for $29 and I will pay you $.20 per share for your commitment to sell 100 shares”. This means that the premium for the contract will be $20 (100 shares x $.20). It’s important to understand a few points here.

Strike price is the agreed upon price (in this case $29). This is universal for both calls and puts.

The premium (the price) of the contract goes up and down as the share price goes up and down. Some traders exclusively make money off the price fluctuation of the premium in the options market.

All options contracts are 100 shares (1 contract = 100 shares).

When you sell a call option, you are essentially on the other side of this equation. You are telling the buyer of the call, “I will sell you my shares for $29 per share if you pay me $20 for this contract.” When this transaction is executed, the seller of the option collects $20. This is also called ‘selling covered calls’ because you’re selling call option contracts to collect premium and you have the shares to back this contract up, which is why it’s covered. If you don’t have shares, it’s called ‘selling naked’. At this point it’s important to mention that if the price of the stock does not hit $29, the contract will expire worthless. Meaning the buyer of the contract will not end up with shares and the seller will keep their shares and the premium.

Selling covered calls is an important opportunistic strategy that I often use to cash flow my long term investing portfolio. If I think one of my stocks have run up too much on hype/excitement, I will sell a ‘covered call option’ to collect premium from buyers. Like I mentioned, this is opportunistic and this wouldn’t work well if the share price declined and I thought the price would most likely recover to the strike price.

Put options have their own unique fundamentals that work inversely from call options. The terminology is similar to call options, where you still have a strike price on a specific date but the buyer and seller role is different. When you buy a put option, this is a way to hedge your portfolio and manage risk by limiting downside. In the example above, the buyer of a put option tells the seller, “I think my shares may decrease in value, I will pay you a premium (let’s say $1 per share) to sell my stock to you for $18 per share.” The seller of this contract collects $100 and will agree to this purchase. The buyer in this instance is hedging their portfolio and can be a great strategy in Bear Markets or during uncertain times with risky stocks. If the price goes under the $18 strike price, the option can be exercised but if it does not go below $18 it will expire worthless.

The seller in this instance can really stand to benefit especially if this is a stock they like long term. If the seller likes the stock at $18, they will collect the premium and the shares (assuming it goes below the strike price). If the shares remain above the $18 strike price, the seller of the option will collect $100 and the option will expire worthless, therefore, collecting cash.

This can all tie into a long term investing strategy, to give you a few ideas this is way I’ll use calls/puts to manage risk and generate cash flow:

Buying call options on businesses I like during market rotations, corrections, and crashes. I will also buy calls on new IPO’s (once options are available) I like but I am not 100% sure how some businesses will be reciprocated. This is a way for me to define risk. My total loss will be limited to the premium I pay. For example, I like Bright Health Group $BHG so I bought call options on them due to the negative sentiment toward this stock in the market. I defined my risk and bought long term calls at a strike price I like it at. I have every intention of owning this stock.

Buying covered puts on a business I own if I think the valuation has as gotten way too far ahead of itself or if I think there’s a market crash looming.

Selling covered call options on stocks I think may trade sideways for awhile to collect premium and generate new cash flow.

Selling puts on stocks I really like and wouldn’t mind adding to my portfolio if it got below that specific price. I’m basically getting paid to buy a business I like at a certain price. If it doesn’t go below the strike price, then I have new capital to use.

My mindset remains long term in all the strategies listed above with the idea that I would rather not sell my stocks. However, I do seek to manage risk and generate cash flow for my long term investing portfolio.

Stay tuned and stay classy,

Dillon