Digital Ocean: A Cloud Infrastructure Disruptor

Digital Ocean: A Cloud Infrastructure Disruptor

If AWS and Shopify had a spinoff, this would be it

I draw a comparison between AWS (Amazon Web Services) and Shopify to describe Digital Ocean because it’s a pure play on cloud infrastructure that serves the massive SMB market. Their mission, “to simplify cloud computing so developers and businesses can spend more time creating software that changes the world.” In simple terms, they provide cloud services for small and medium sized businesses to build upon.

This publication will focus on a few concepts that have built an extraordinarily compelling bull thesis for investment. What we will focus on here:

The underlying business model

The exponentially expansive and large market opportunity

Catalysts for accelerated growth from current rate

Business financials and latest quarterly result

My plan for investment

Digital Ocean’s Business Model

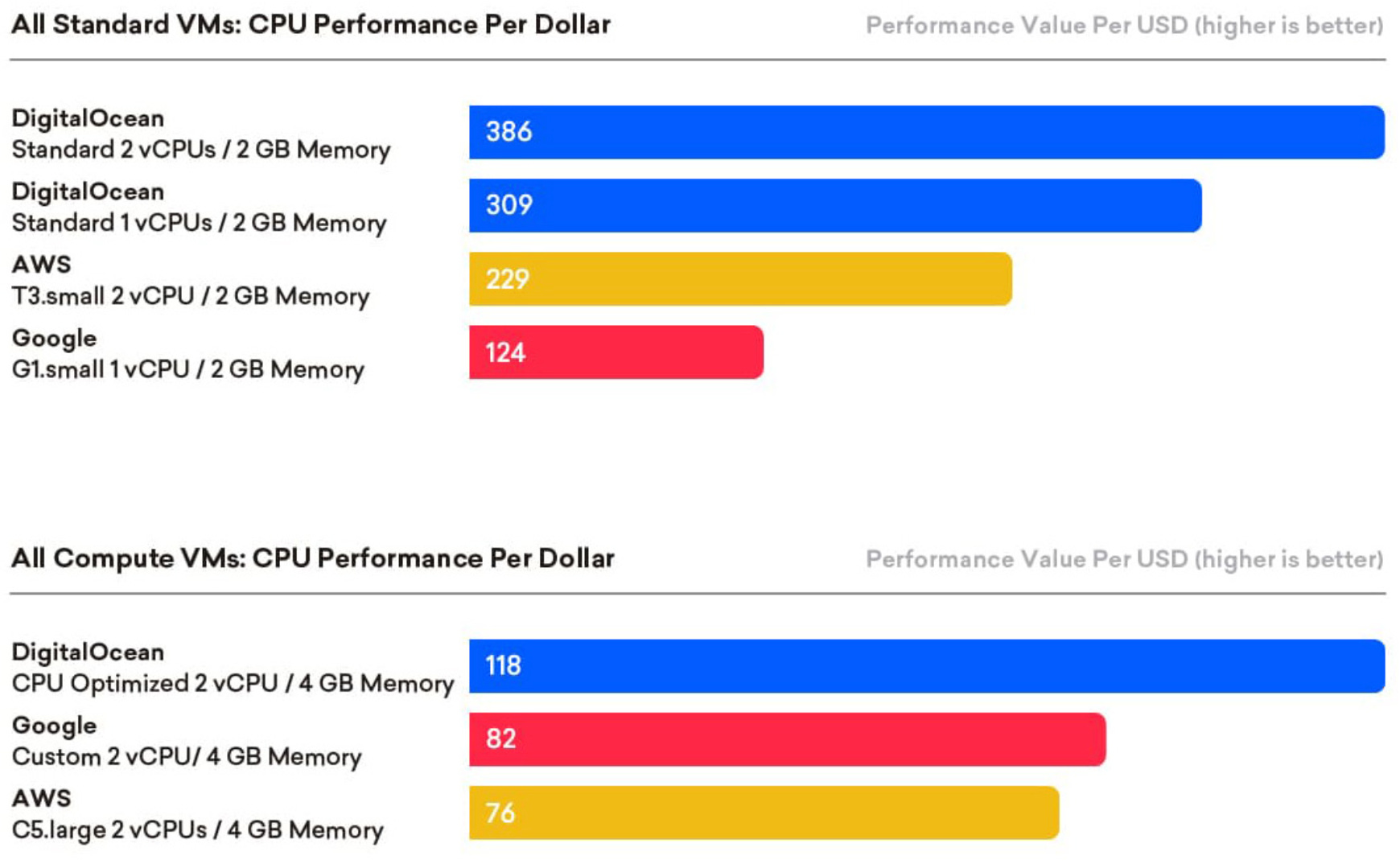

Digital Ocean draws a strong comparison to a few of the other cloud giants like AWS, Microsoft, or Google. However, they have a unique pricing and capability competitive advantage that positions them perfectly to address their primary audience, the small to midsize business market. In a study done by Cloud Spectator LLC, they benchmarked Digital Ocean’s virtual machine (VM) performance per USD against the top two players in the industry: AWS and Google. What the study found was that Digital Ocean provided the best performance per dollar in the industry.

This high performance, low cost model works great for SMB’s. However, their focus on addressing this target market need only begins with price/performance. They offer a market place that offers a collaborative feature where “developers support developers”. Essentially, this is a place where newer businesses, entrepreneurs, and tech developers can go to learn.

They offer multiple content types like curriculum and books (above) but also offer: Conceptual articles, tech talks, tutorials, cheat sheets, meet up kits, and events. This positions Digital Ocean in a unique way to be the go-to place to enable the entrepreneurship and innovation of tomorrow.

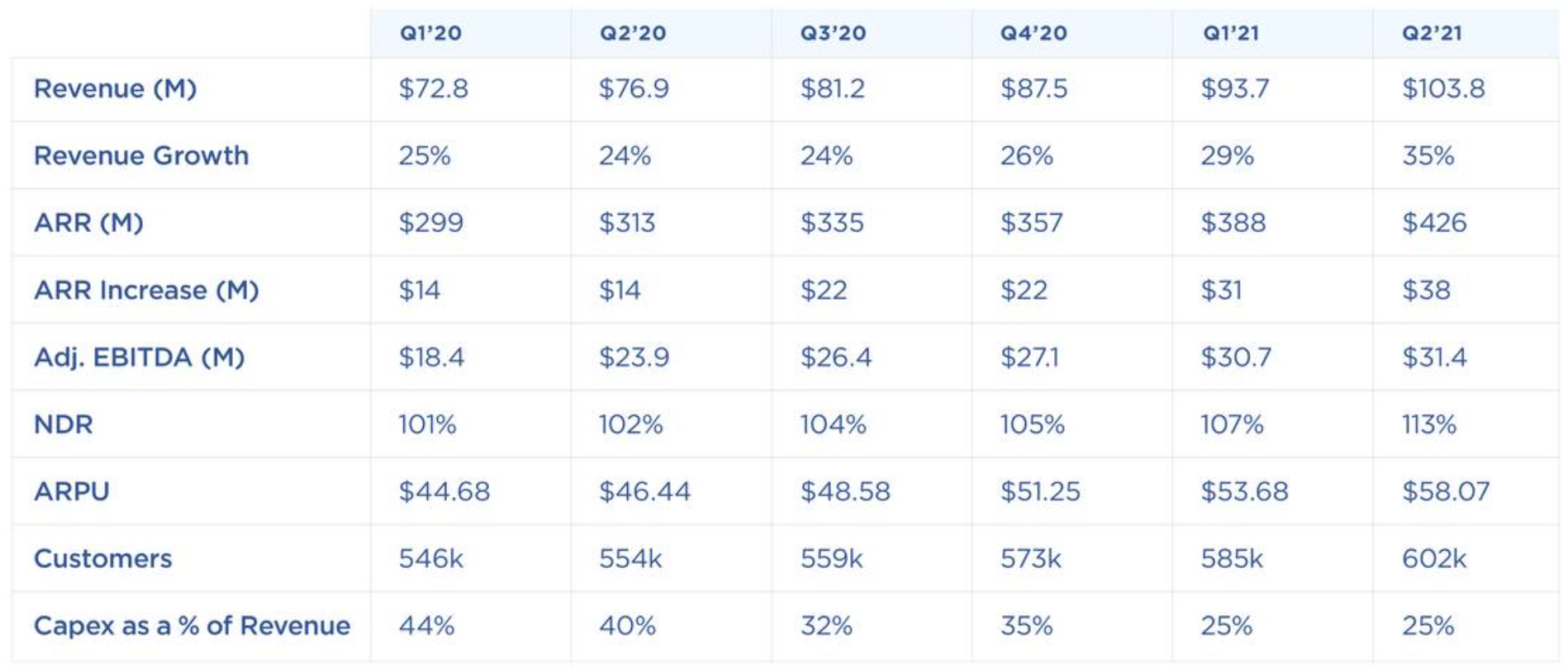

This small consumer centric model has led them to obtain over 602,000 customers with 10’s of thousands being added on a monthly basis. The way I like to look at this is a funnel effect. Of these new customers, they have a relatively high churn. However, once they pass one year on Digital Ocean’s infrastructure their churn is less than 1%. This makes a ton of sense to have a higher churn in the SMB market, especially with new businesses or ideas. But obviously, the successful smaller businesses will eventually scale and grow revenue. When their customer grows, Digital Ocean begins to make more revenue due to their consumption based business model. This means they have a vested interest in retaining and growing every single one of their customers. Another business that runs this similar model of enabling SMB customer success, Shopify.

The Massive Market Opportunity

The unique thing about operating in the SMB market is that it offers a massive, low hanging fruit, opportunity that the larger players tend to not focus on to the extent Digital Ocean does.

Currently AWS and Microsoft Azure do have a products for SMB, but Digital Ocean is priced 28% lower than AWS and 26% lower than Azure.

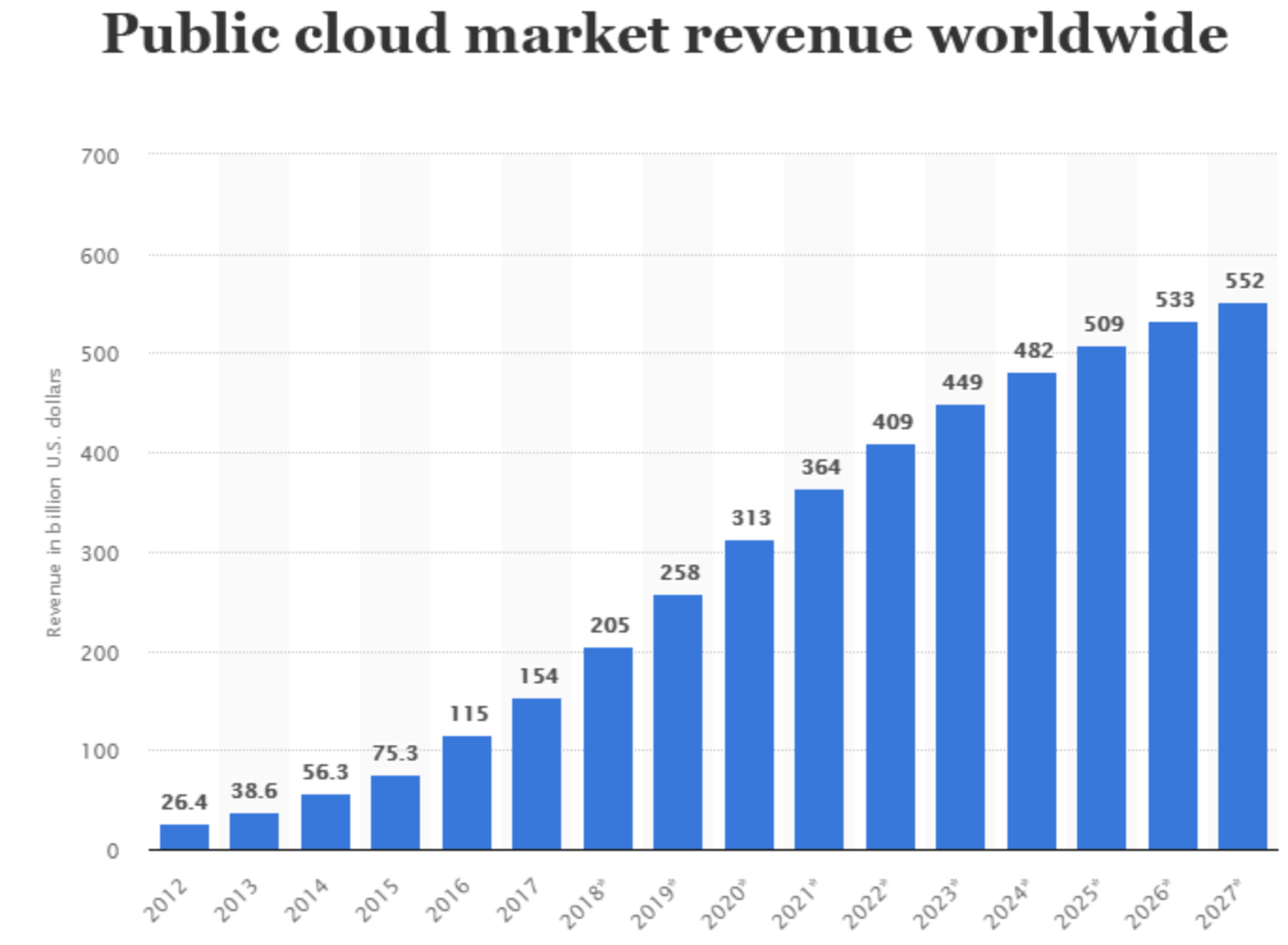

In addition, digital transformation and cloud adoption has been a secular growth trend that’s still in its early stages.

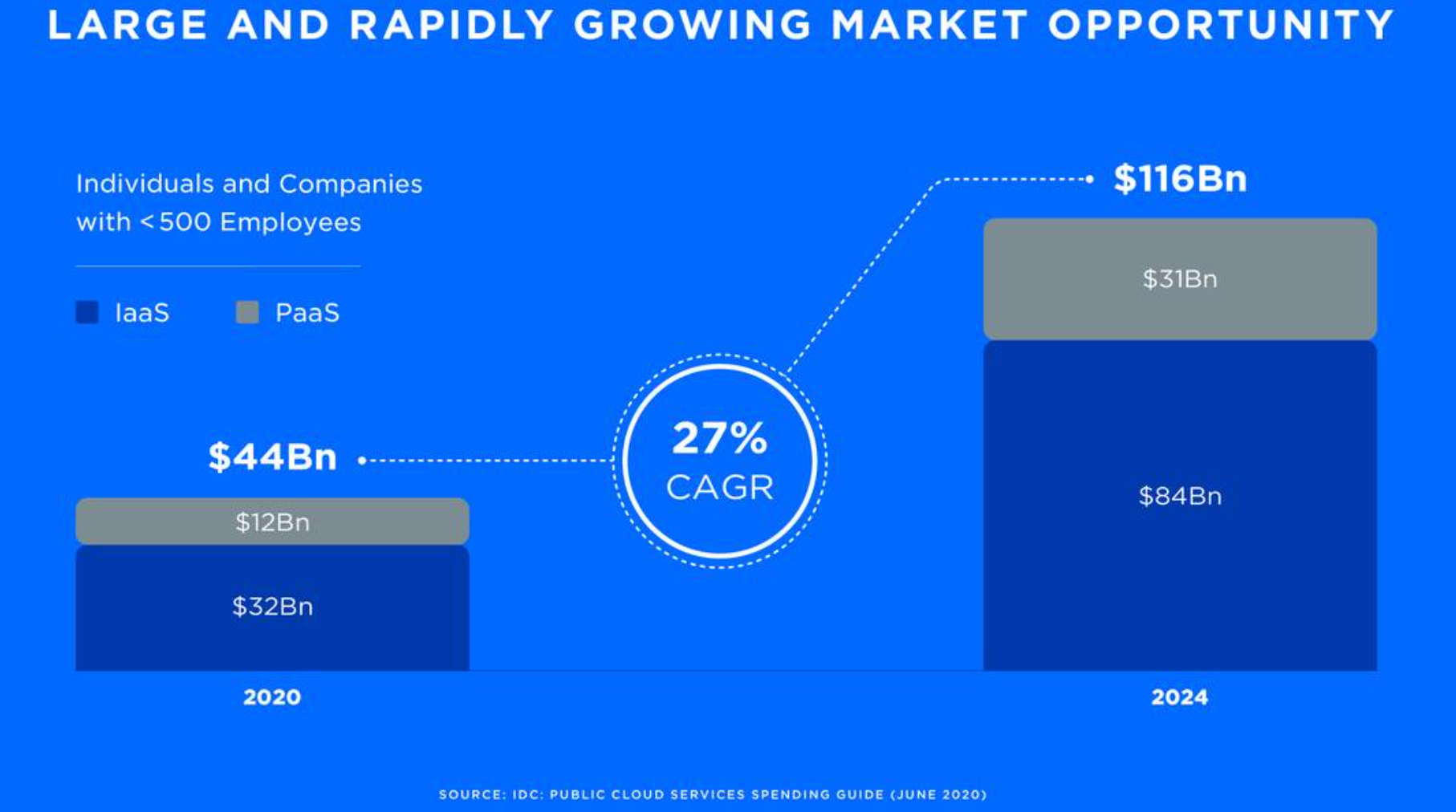

When it comes to Digital Ocean’s addressable market, it was surprising to find out that 44% of all the U.S. GDP comes from SMB’s! When you isolate their cloud infrastructure and platform demand, it turns out to be quite large.

27% compound annual growth rate is arguably one of the fastest growing TAM’s I’ve researched. This implies a near 3x market opportunity from 2020 over the next 4 years. Due to the reasons I listed above in the business model portion, I believe they’re well positioned to capture even a size-able portion of this market share. To put this into perspective, if they capture only 10% market-share of 2024’s TAM this would equate to $11.6B in revenue for Digital Ocean. They’re only projected to do a little over $400m in FY 2021. Needless to say, they have serious room to grow and have the wind at their back.

Accelerated Revenue Growth

There’s nothing more sweet to me as an investor than to place a bet on a business that has the ability to accelerate revenue growth and beat revenue/earnings projections. Another business that has recently done this is Upstart. I believe we have the opportunity to see something similar here. There are two big reasons why I am led to believe that they are more than well positioned to accelerate revenue growth from today.

The first reason and rationale, they’re already doing it:

Above, when I mentioned they have less than 1% churn after their customers reach 1 year on their infrastructure, this is an underlying proponent for exponential growth. When these businesses eventually become successful, they spend more and more with Digital Ocean. This will continue to increase Net Dollar Retention Rate and Monthly ARPU. The best way to think about this is that it acts a lot like a Snowball rolling down hill. As it roles down the hill it continues to collect more and more snow as the surface area continues to expand. This is applicable to Digital Ocean’s SMB base because they’re consumption based. The more their clients consume, or the more infrastructure they need, the more DOCN’s revenue will expand. In simple terms, their smaller clients success will eventually pay dividends years from now.

The second reason will come as surprise. They have managed to grow in the high 20’s to low 30’s without a significant sales force. This means they have depended heavily on marketing, website traffic and word of mouth. They call this a “self service marketing model”. They’ve essentially created this self service, low friction, easy to try/adopt model on their website which has accomplished a global presence of over 600k customers and rising every day. This type of organic growth is very impressive and one can only imagine what can happen with additional investment. In 2020, 2% of their revenue came from a sales force and in 2021 this grew to 3%.

On their latest earnings call, they mentioned that they will continue to invest heavily into this space and said they’re, “very optimistic about the ability to see a lot of leverage and much more contribution as a percentage of our overall growth and revenue portfolio over time”. Sales drive business growth and a good sales force can grab market share on an exponential basis. My opinion, further investment here can see revenue growth begin to accelerate to 40-50% YoY.

Latest Quarterly Results

Digital Ocean grew their business impressively but equally as important, they grew their bottom line and free cash flow. In other words, Digital Ocean is positioning itself uniquely among its competitors when it comes to future share holder returns.

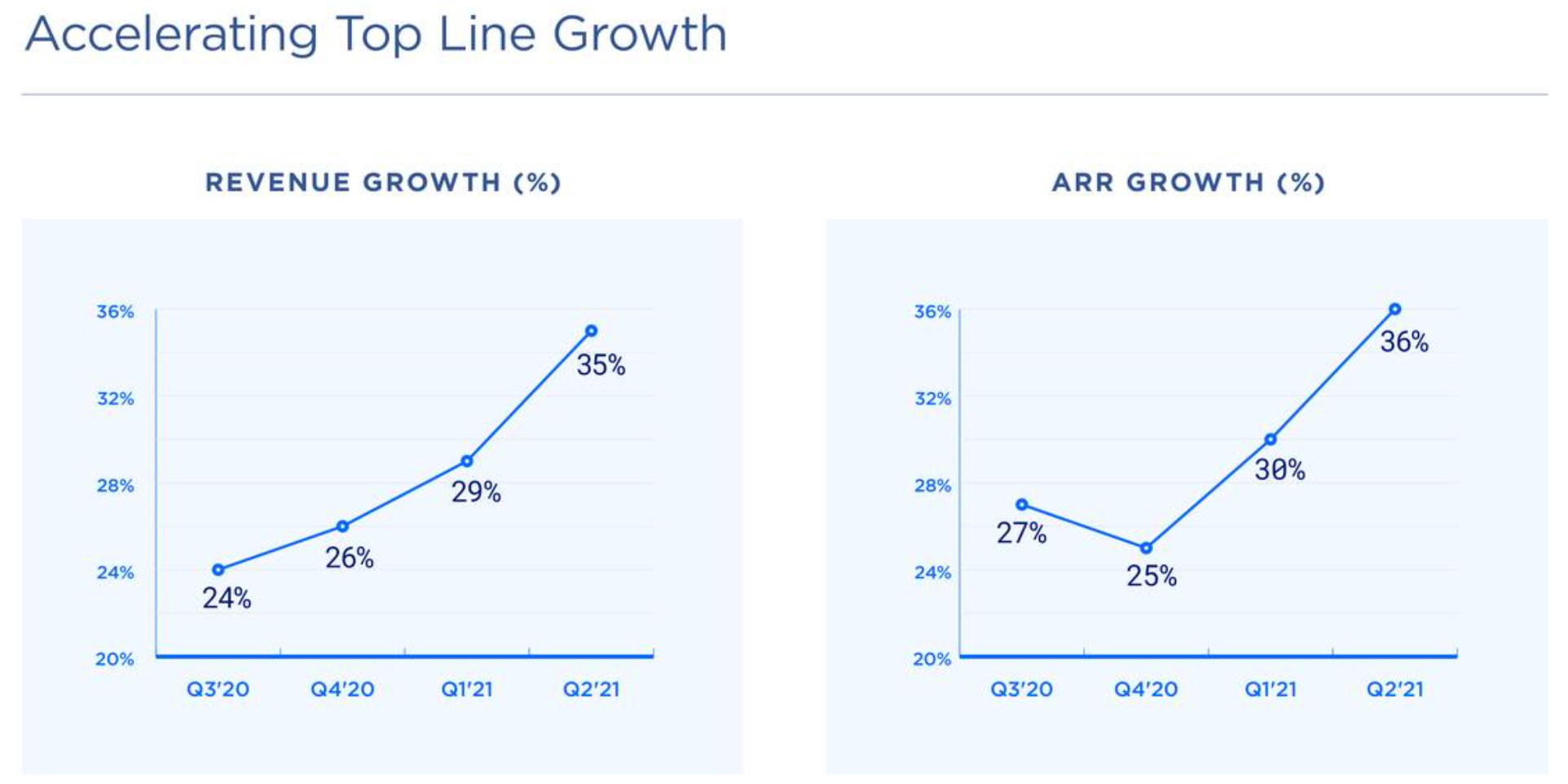

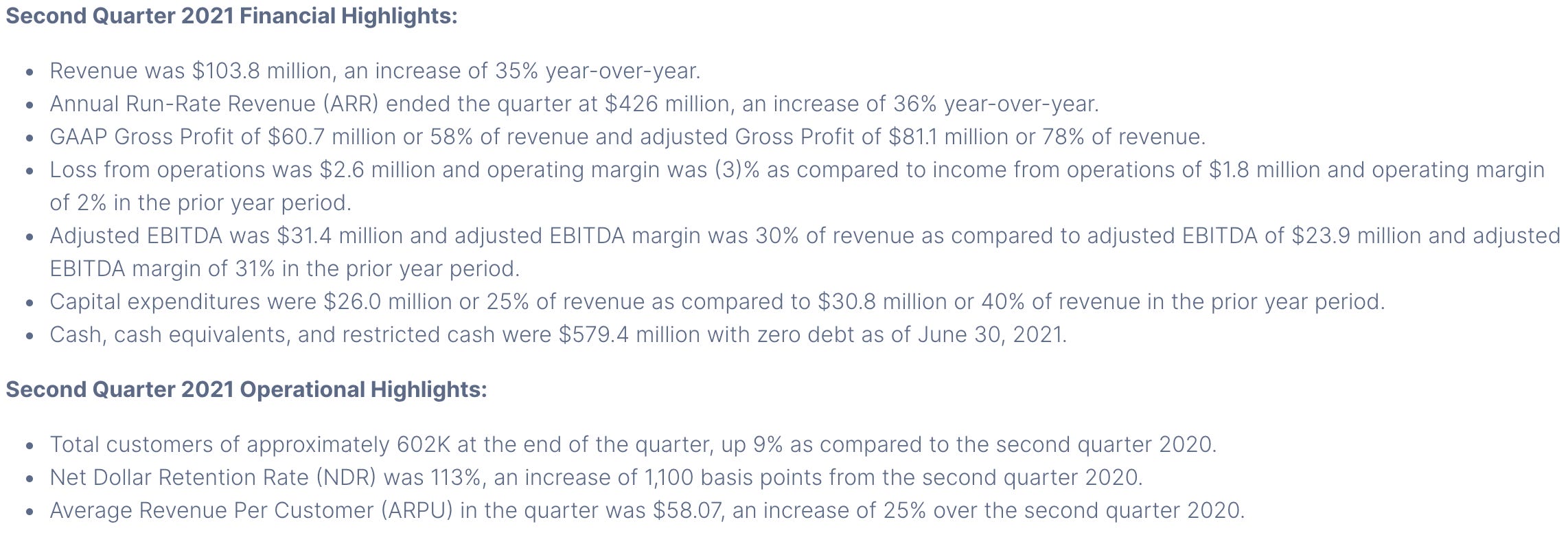

There are a few highlights that are very interesting. Revenue was up 35% YoY, which was very surprising. Seeing this number accelerate from last quarter was very exciting. In addition, their Adjusted EBITDA Margin of 30% is very exciting. There’s a rule of 40 when it comes to investing in software businesses. This means the business is on an acceptable growth trajectory when both revenue growth % and EBITDA % are higher than 40 after being added together. In this case:

Revenue growth of 35% + Adjusted EBITDA of 30% = 65%

This is exceptional on the top and bottom line. Only a few businesses I follow are able to accomplish this.

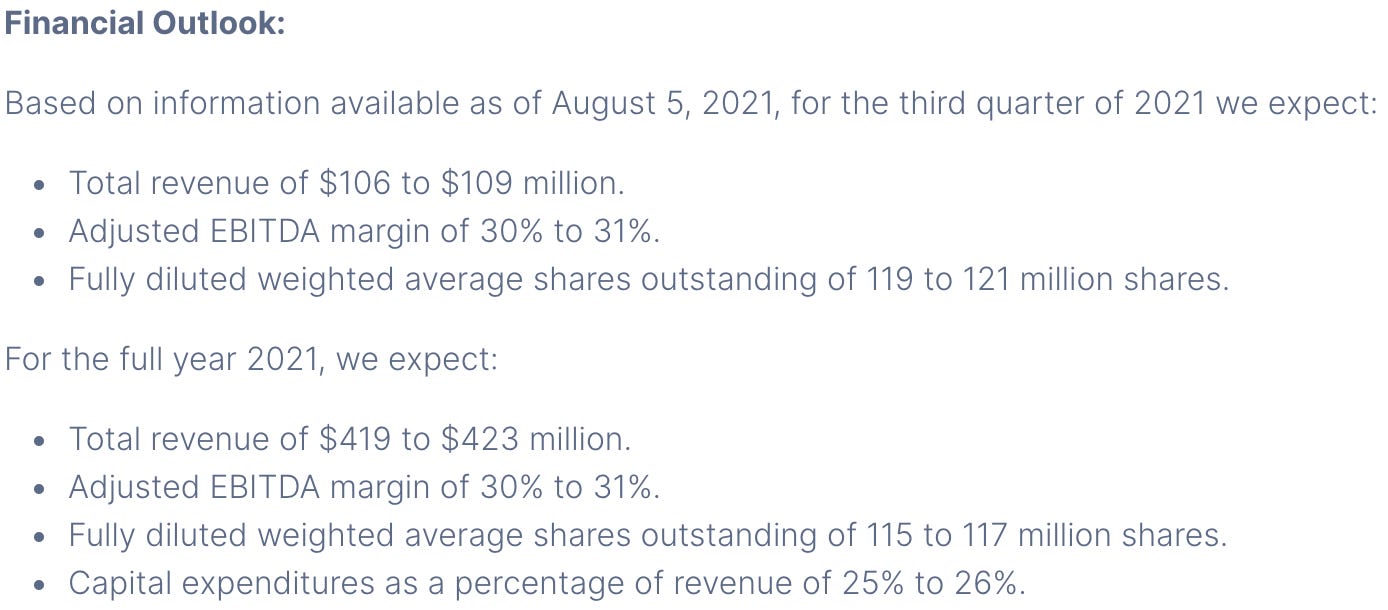

Their growth guidance was equally bullish, but I am fairly certain they are sandbagging on their growth.

The reason why I think they’re sandbagging has a lot to do with the two cases I outlined above for accelerated growth trajectory and their massive TAM. It wouldn’t surprise me to see total revenue break $110m for Q3 with a continued expansion of ARPU and NDR (Net Dollar Retention) break 115%. Look at their previous trends with these two metrics:

What I’d really like to see is customers expand faster than their original metric of 9% YoY. On their call, they mentioned they can see this getting to 10%+ and that’s a key metric management follows. Regardless, I am excited to see their next quarterly report to see if the accelerated growth trajectory continues.

From a financial perspective, there’s a lot of upside to be had with this business. They are growing nicely at 35% YoY and are a free cash flow machine. With their TAM as large as it is, growing at a CAGR of 27%, I see little stopping this business from producing excellent long term share holder returns.

Conclusion

I have initiated a position in Digital Ocean and will add on any weakness that could potentially see the share price drop down to the low $50’s. I will assume that the weakness in share price will come from overall market weakness due to the strong profitability and growth of the business. At the time of writing this, their market-cap is roughly $7B with $500m on the balance sheet with no debt. This will give it an enterprise value of $6.5B which will put it’s EV to sales at 16x and their EV/EBITDA at 52x which is a more than reasonable valuation given their growth and especially if they beat earnings and raise guidance next quarter.

I will continue to cover this growth story through this substack. As always guys, stay tuned and stay classy.

Dillon