Digital Turbine - The Saga Fuels On!

Digital Turbine - The Saga Fuels On!

Post Earnings Analysis

Digital Turbine knocked it out of the park.

In this publication, what I’ll cover are the top-line results, what this means for the story as a whole, and the business model. More importantly, I’ll talk about where they’ve been, what they’re doing now and where they’re going.

I am confident you’ll walk away from this with a new or renewed insight.

Top-line Results:

Revenue: $212.6m vs $190.28m expected, representing a 260% YoY increase

Non-GAAp EPS: $.34 vs $.31 expected, representing a 161.54% YoY increase

Guidance:

Q2 Revenue: $300m - $306m vs $291m estimate

Q2 EPS: $.38 vs $.37 expected

Yes, these results are absolutely incredible but I believe this is exactly what APPS needed to move higher. See, the thing that’s happened with Digital Turbine is that a majority of this revenue growth is from three different businesses they’ve acquired: Appreciate, Fyber, and Ad-Colony (we’ll get more into these later). What is important about these metrics, is that Digital Turbine is still showing that it has the ability to continue to beat expectations even after the recent mergers. It’s important to know that the market already priced a lot of this in but this was absolutely a “show me” story and I think Bill Stone and his executive team did just that. They proved they can still win. I think now is the time for some stock price appreciation! :D

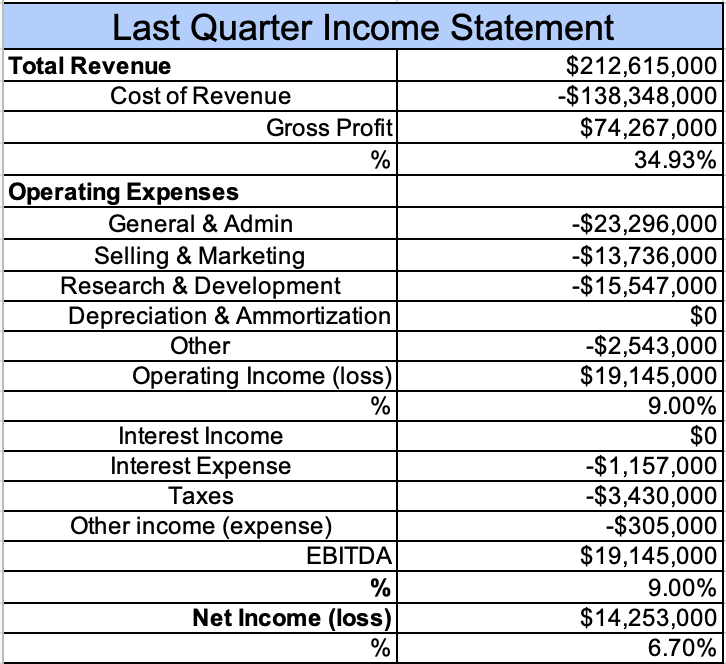

However, we all need to be aware of this risk, their balance sheet and cash flow is definitely cause for pause. Let me show you exactly what I’m looking at first, this is from a spread sheet I put together to manage all my investments:

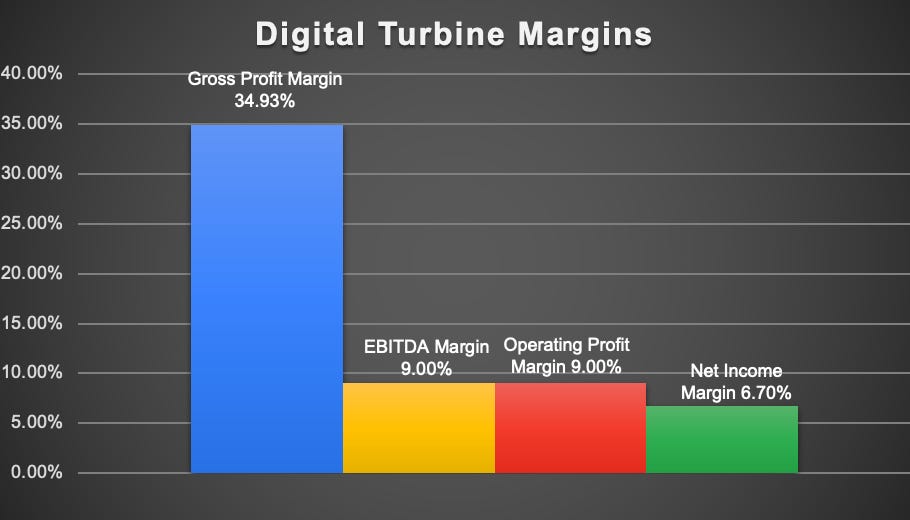

Their gross profit, operating income, EBITDA and net income all decreased QoQ. You can see the margins more here:

This isn’t terrible but it isn’t great. It’s great that they’re making money and they are net income positive but the gross margins decreased from 40% to 35% this quarter. Is this something to be concerned about? Keep reading…

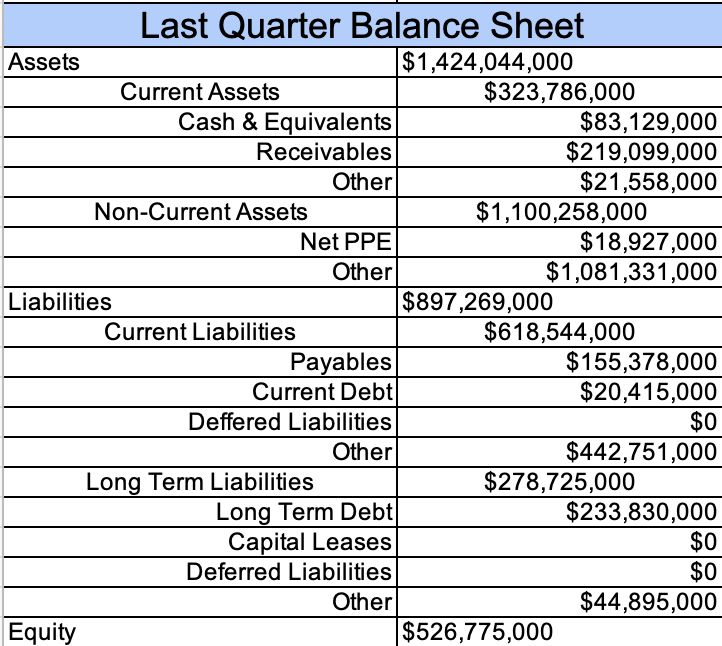

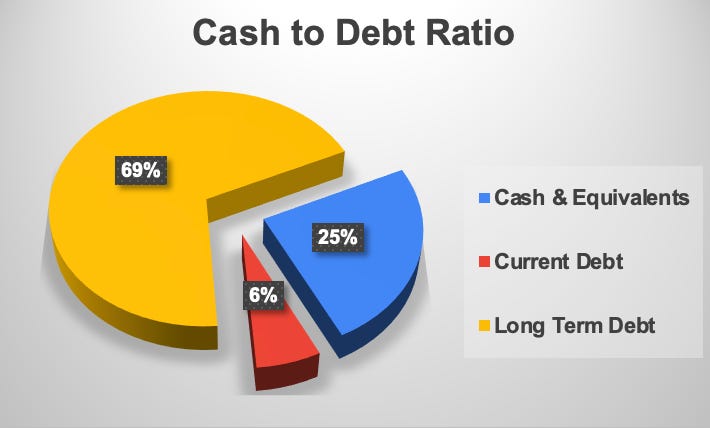

Their balance sheet is pretty levered up as well:

This cash to debt ratio is arguably the worst out of every investment I own but we have to talk exactly about what happened and the amount of risk that’s associated with this.

They levered up to invest in their business when the cost of debt was cheaper than equity. This is basic corporate finance 101. Rather than raising equity, they levered up to take on debt to fund their latest three purchases of Appreciate, Fyber and Ad-Colony. Honestly, I love this move and I typically hate debt on any businesses balance sheet. The most important thing to take away here is that they are net income positive. This means there’s going to constantly be cashflow from operations. It’s also important to mention that Bill Stone (the CEO) mentioned that all these businesses are already profitable as well and when synergies are realized, they will improve their margins. I expect over the coming quarters they will continue to build their balance sheet with their profitable business model to pay off debt. As far as any acquisitions in the short to intermediate term, I think that is very unlikely given how much they just did. I would anticipate their business strategy is focused on realizing the full potential of their investments to create business synergy.

But that begs the question, what exactly are they trying to accomplish? Let’s talk about their three business adds and briefly cover what exactly each one does, as well as the organic business.

Fyber is an app monetization company, specifically around mobile games. They’re basically a digital advertising company.

AdColony, another mobile app monetization company, that acts as a digital advertising company for developers and publishers.

Appreciate is a supply side, programmatic, mobile advertising platform. Much like the other two. Although each is unique and I could definitely go into how they differ, I’ll focus primarily on Digital Turbines strategy for growth.

Before understanding the strategy, we have to understand exactly what Digital Turbine’s organic business does. This can really be broken up into three components:

Single tap: It’s the simple tap solution on droid devices that allow you to instantly download any app

The Discover Bar: This enables for content to be found on your phone to quickly download new apps for your android device

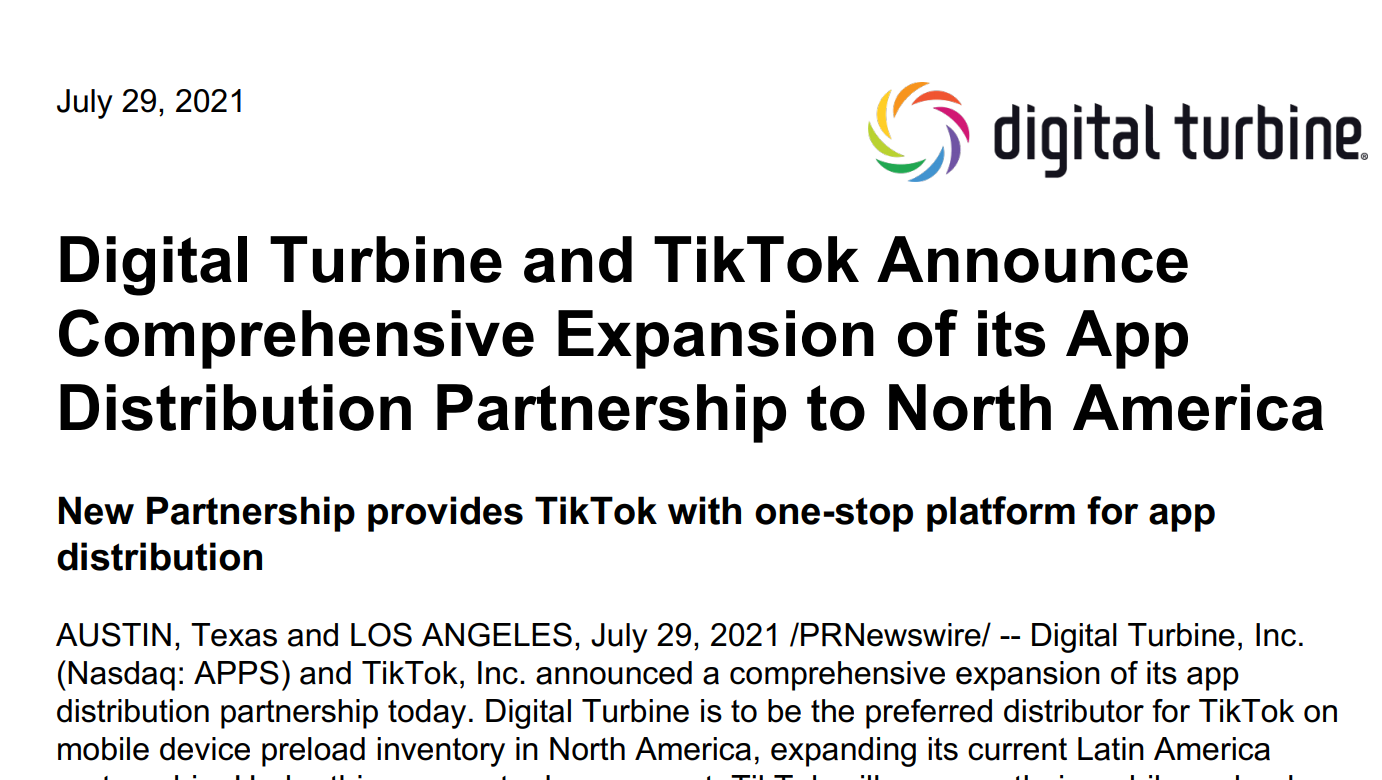

The Home Screen: Place your app directly on a device for instant use. For Example, TikTok has recently done this for android devices through Digital Turbine.

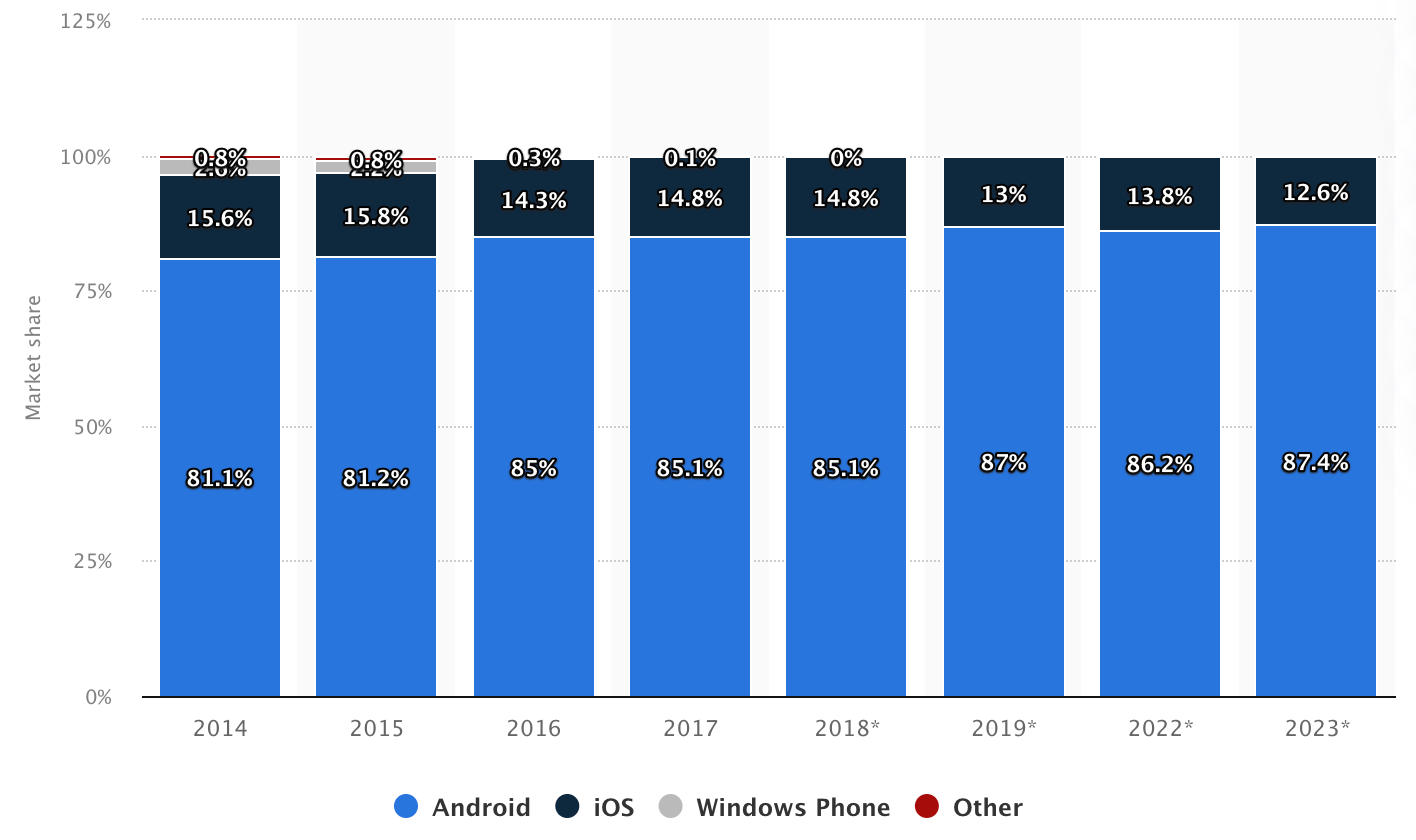

Ok, now we can talk about their strategy. Basically, what they’re trying to accomplish is being the premier advertising partner for mobile apps. Digital Turbine’s software is downloaded and included on every android device. In turn they split the revenue directly with Google. I originally dismissed this when I heard they only work with Android, but then I saw the market share between iOS and Android worldwide:

As app adoption and cellphone usage continue to grow, so does Digital Turbine’s relevance and market. After they help app creators get their content discovered, they can and will now continue to manage that partnership throughout the life of the device with their newly acquired businesses which creates recurring advertising revenue. This is big, very big, and nobody else does this or has this sort of close, unique relationship with the end consumer and app creators. Essentially, they make money in two ways:

1.) They make money when the app is first discovered and installed

2.) They make money through all the advertisements run through that app, that reaches the user

This second part to their revenue model is only recently applicable through their three major acquisitions and every reason in the world why I am this bullish on them. I cannot see this slowing down any time soon.

Conclusion

APPS is just beginning and this is chapter 1 to a business that has a much larger and longer growth story. Despite their slightly uneven balance sheet, they’re in hyper growth mode and the synergies between these businesses have yet to be fully realized. I expect margins will continue to increase and expand, along with their debt being repaid before they make another significant investment. They have mentioned that the next chapter would include all device types (not just mobile) like TV, or really anything with a screen. Long term, screens and operating systems aren’t going away. Neither is Google, who they work closely with.

On the Google note, many would ask if I have concern about their partnership together since Google can just make their own software for their devices. I have no concern, Digital Turbine has made Google hundreds of millions of dollars over the years. A likely scenario is an acquisition, if anything.

I am long APPS and don’t intend on selling a single share. It is, and will remain, one of my largest positions.

Good article. But I think Digital turbines shared the revenue with the phone carrier instead of with Google. Fundamentally, this will be different in supplier relationships as having Google as their sole supplier might render the company a victim of negotiation should this be the case. However, this is not what is being practiced at Digital Turbines. They have multiple relationships with phone carriers such as AT&T of whom they'll share their revenue split with them. Gross margin is low as Digital Turbines report Gross revenue before splitting it with the phone carriers.

What's up with the price action today? Downgrade by Cannacord or something else? Thx.