Earnings in Review: DLocal and Snowflake

Earnings in Review: DLocal and Snowflake

Two incredible businesses, two earnings releases covered

I am going to release back to back newsletters over the next two days because there was a lot to talk about this last week and, since my 9-5 job had me in a hurricane over the past few days, I will make up for the midweek memo.

In today’s Newsletter we are going to review DLocal and Snowflake’s earnings. We are going to answer questions like:

Why did DLocal drop after earnings and why would the price recover shortly after?

What was so great about Snowflake’s earnings? Why did it pop nearly 20%? Is it sustainable?

Are either of these businesses buys now?

On the next newsletter released tomorrow, I will talk about Jackson Hole and what this means for the markets moving forward as well as provide a portfolio update.

*Quick Plug*

If you enjoy my analysis, please consider subscribing to the free or paid supporter version of BluSuit’s Newsletter where I write Bi-Weekly on important news like:

Federal Reserve policy evolution and how it impacts the markets

Bond market expectations

Stock earnings

Market technicals & direction

Members also enjoy a free BluSuit Discord group to collaborate together. At the moment, our members chat has hundreds of participants all talking about technical analysis, portfolio strategy, fundamental analysis and their favorite stock picks.

*End Plug*

Alright, let’s get back to it.

DLocal Earnings in Review

I am going to talk primarily about their results but if you’re interested in learning more about the business, I posted a short SubStack here about their business model:

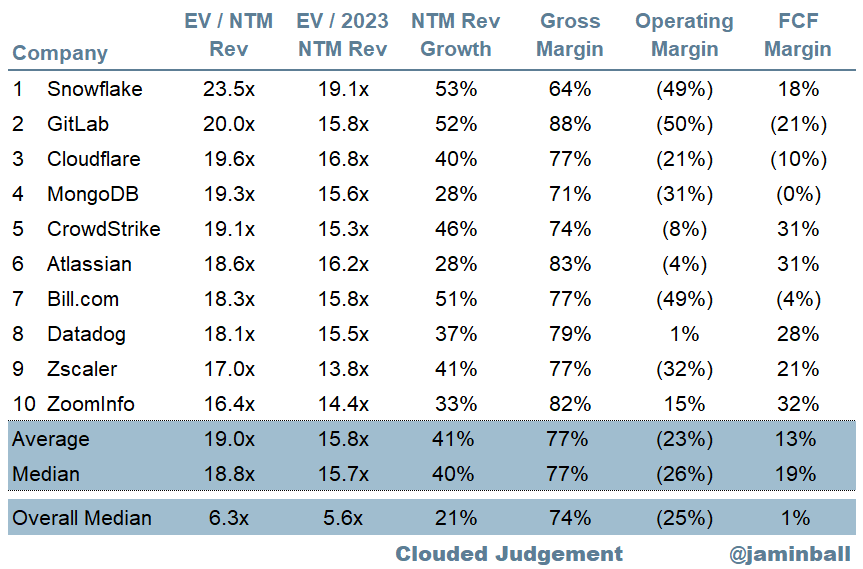

DLocal is one of my favorite positions and they sold off after their latest earnings report. I, of course, have a few thoughts around why there was weakness in the stock price. First, let’s go over the valuation:

$7.7B company, roughly a $7.3B enterprise value

TTM PE of 100x

Forward NTM PE 60x

2023 P/E 39x

Forward price to sales ratio of 16x

In my opinion, DLocal is an expensive stock. Typically when you see very expensive businesses not outperform on every metric, or at least a majority of them, you see their stock price struggle. On a valuation perspective, DLocal finds itself priced in line with the most expensive stocks on the stock market.

The thing that makes DLocal unique is its profitability compared to many of the other software stocks as they run 35%+ EBITDA margins on a consistent basis.

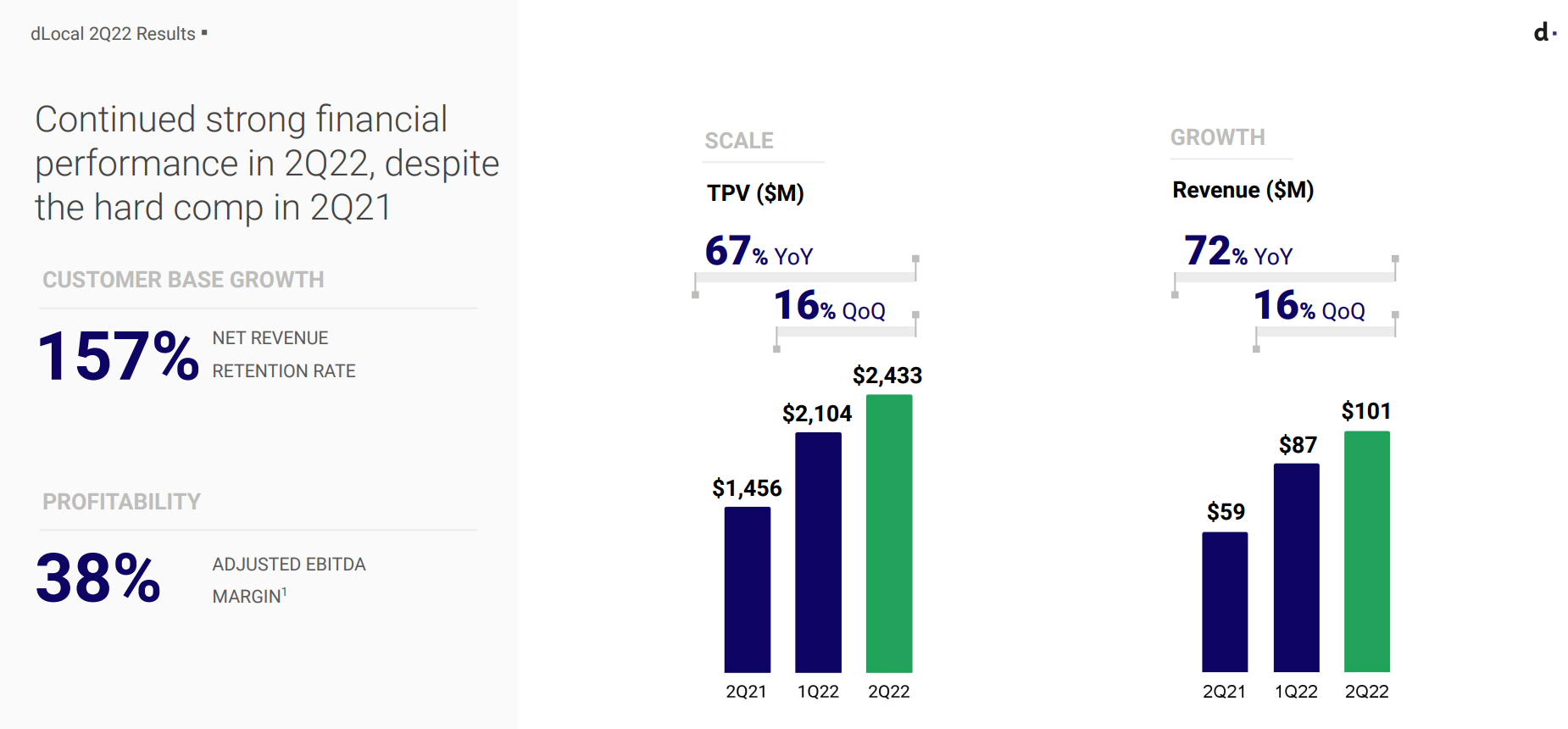

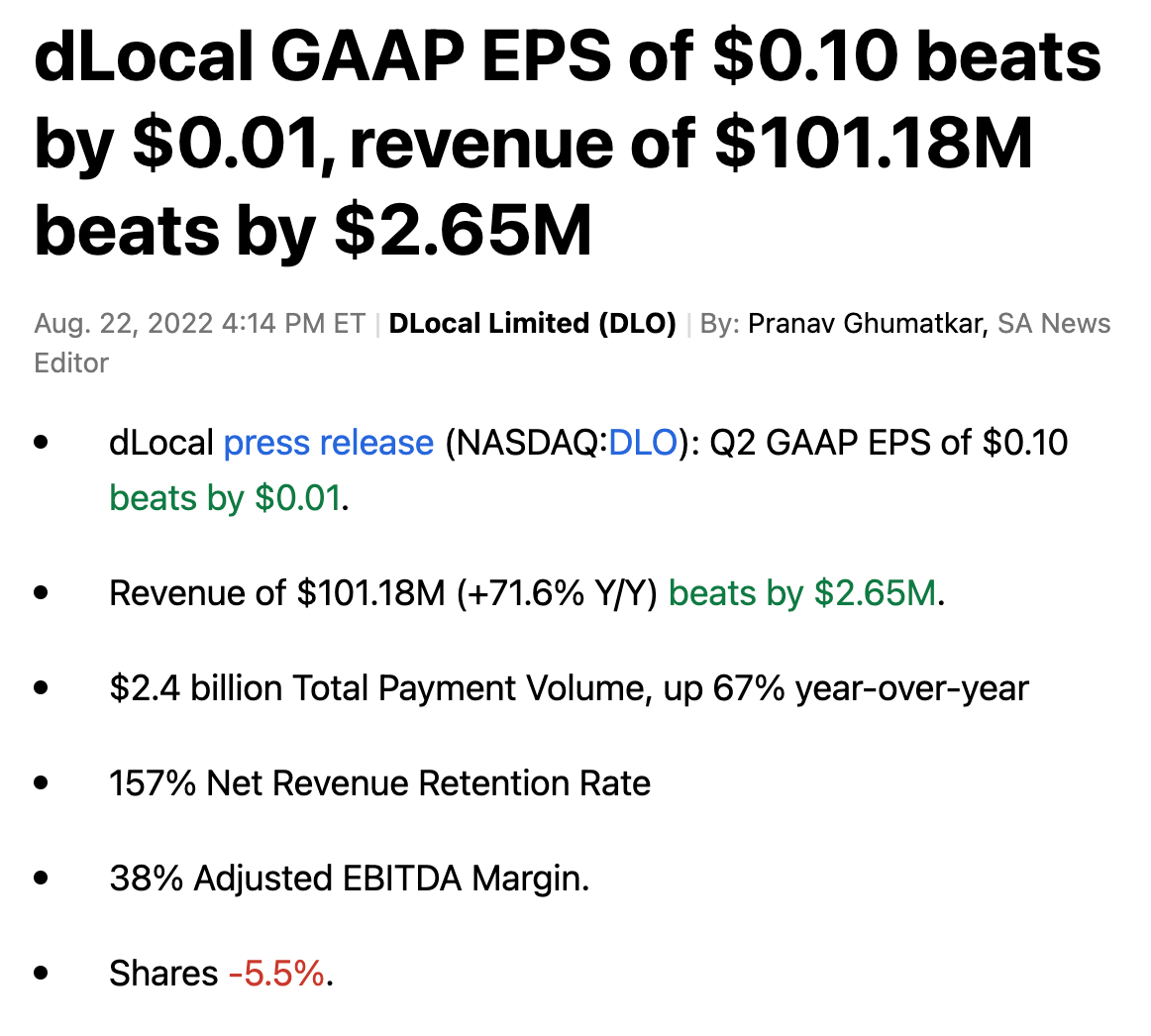

The Results

There are multiple factors that led me to believe (on a results basis) that the stock price was beaten down:

The year over year revenue growth is slowing

DLocal refuses to provide clarification to analyst questions

Lack of guidance

GPV (gross payment volume) is slowing down

Macroeconomic risks, meaning they don’t benefit from a strong dollar

I think the most important of these, that tied to the stock price punishment, was the lack of guidance and clarification on business results for analyst modeling. DLocal’s unusual behavior towards analysts, keeping a more closed door approach to all internal metrics, is not a normal way to report financial results. Typically, I see businesses opening up more and more over time, as a public company.

For example, DLocal guided for 35% full year EBITDA (earnings before interest, taxes depreciation and amortization) margins. At the moment, they are trending for a 38% EBITDA margin on a full year basis but refused to provide clarification if they would somehow end up posting, let’s say, one quarter of 34% EBITDA margins. This does concern Wall Street investors because it could signal that the business is beginning to come under pressure. When you have a forward P/E of 60x, imperfection is a cause for punishment.

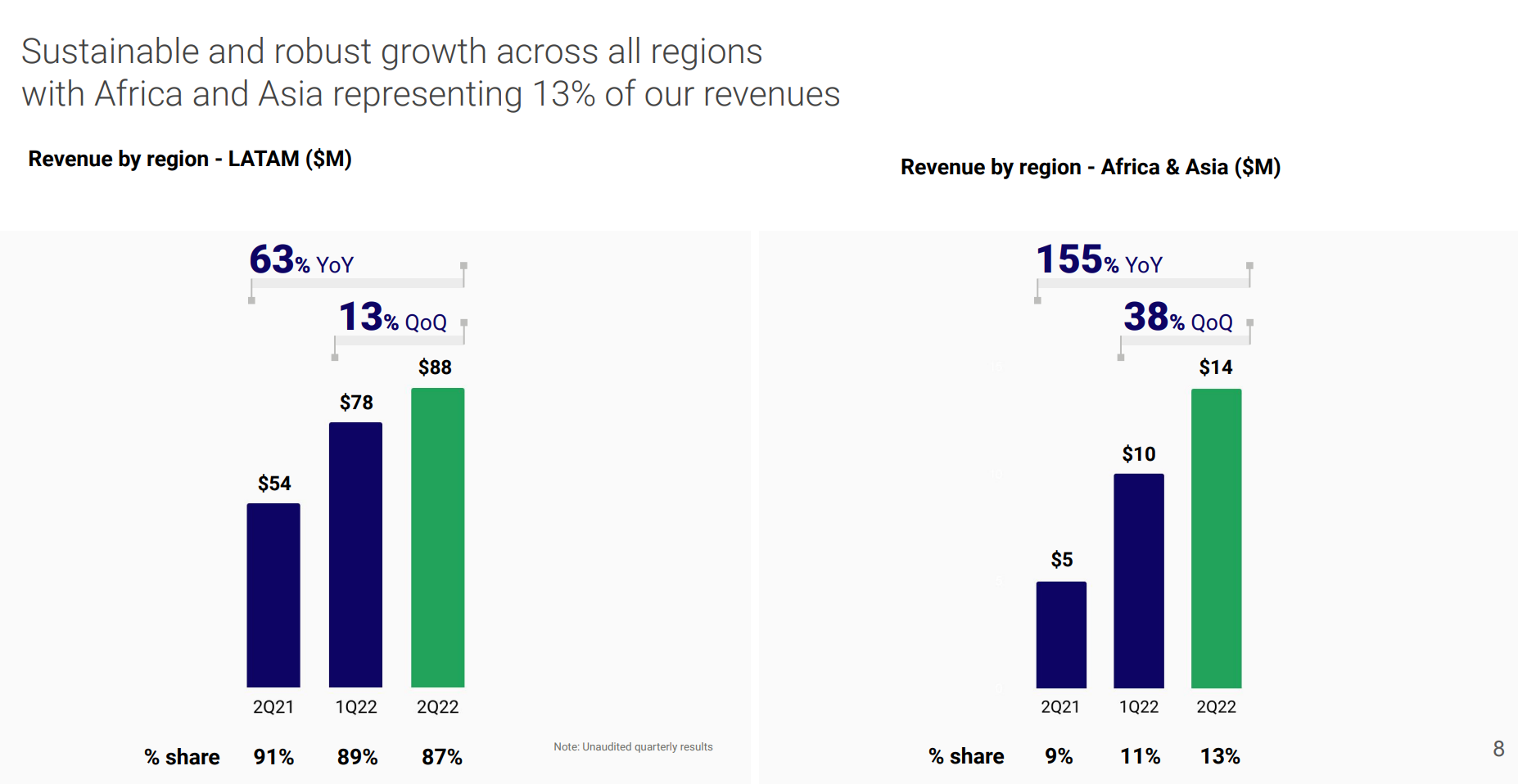

The revenue slow down can actually be explained by macro economic volatility and may not accurately indicate a material slow down in the business. When the U.S. dollar is strong compared to other global currencies this has a tendency to influence emerging market company metrics. DLocal is headquartered in Uruguay and they do a majority of their business in LatAm with other markets in Africa and Asia.

(notice the decrease share % of market share in LatAm, this is cause of concern)

Fx adjustments aside, global commerce has slowed down meaningfully. MercadoLibre (who posted excellent results) only showed 12% YoY growth in the commerce portion to their business. Amazon, Shopify and Sea Limited also showed a noticeable slowdown in international commerce. This is likely do to a global economic recession looming.

The Positives and What I Plan on Doing

Obviously, we have to be aware of the risks and, in my opinion, the ones posted above are the most notable. Investors on Wall Street, and the like, noticed the slow down in revenue, it’s an expensive stock and leadership did nothing to calm investors worries. This did justify a multiple contraction as additional risk is priced in to the stock.

Despite the risks, this is still a fantastic quarter given the macro volatility. They still post profitable revenue growth like the unicorn they are, they still have high NRR and they still have a tremendous opportunity ahead of them. In my opinion, despite increased risk being priced in, this does not invalidate the long term thesis. It reminds me of Global-E’s last quarter when their stock price tanked to $13.50!! I wrote about my thoughts here:

This will be something we, at BluSuit, will continue to monitor and of course I will share my thoughts.

It’s a full sized position, I neither plan to add or trim.

SnowFlake Earnings in Review

Frank Slootman (CEO) is the man. Seriously, this executive team is tremendous and they deserve the hype. Snowflake does an excellent job providing transparency in their business, their financial results and future expectations. In addition, it’s impossible to ignore what Snowflake has done the past few years. For example, when they IPO’d in 2020 they were did about $400m in revenue. This year, 2 years later, they are going to hit $2B in revenue with world class NRR.

In many cases, after this earnings call, I can’t help but consider making Snowflake my largest position. I will add aggressively on any sort of sustained market weakness. More about my perception on the markets tomorrow.

A Short Thesis on the Business Model

Snowflake is pioneering a new category of “DataCloud”, which they like to think of as the progression of the business data infrastructure.

At first, we had computers that had a hard drive (remember those fossils?) and eventually progressed to “the Cloud”. For those who are not very familiar what the cloud is, it is basically offsite storage that’s run by Amazon, Google, or Microsoft and a few other small players. However, a problem emerged in the public cloud, it became silo’d and difficult to manage (because there was so much of it). There was a need to manage data better and unify all the information of a business.

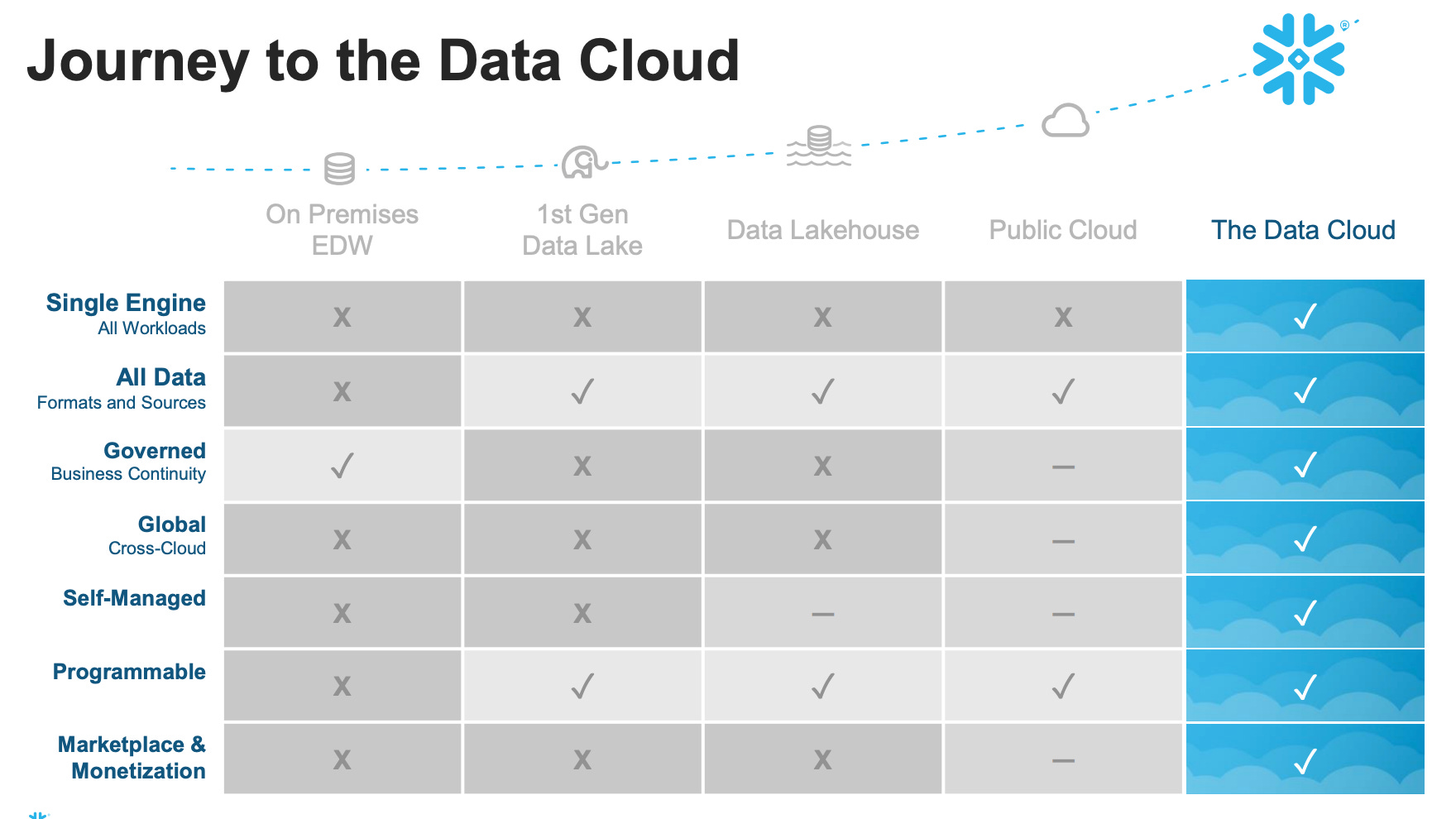

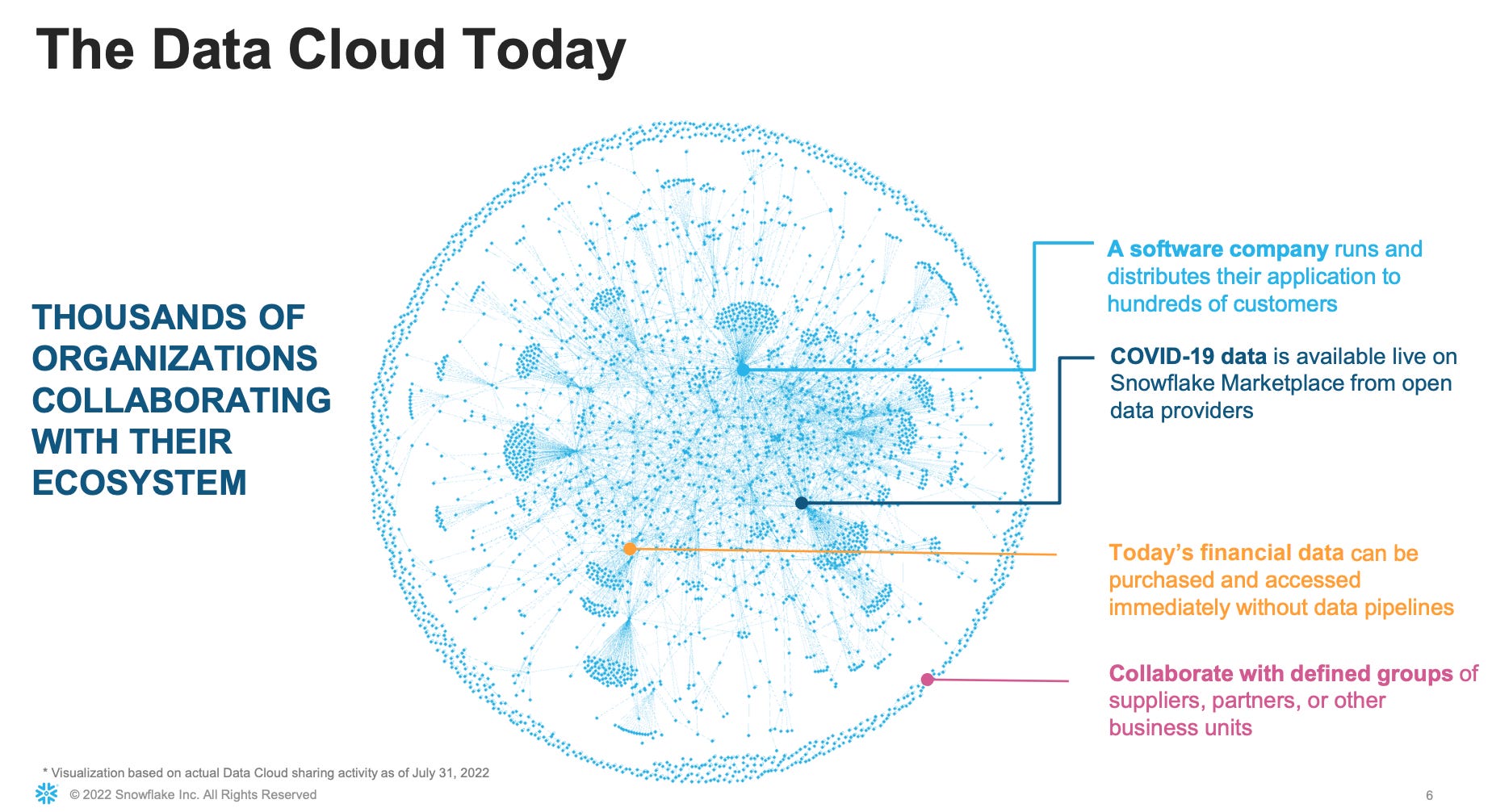

Introduce Snowflake who specializes in unifying multiple clouds and data centers both on and off prem (premise). But, that’s not all they do, they have multiple different product initiatives to become something much larger than just a place to store and manage a company’s information. They are focused on security and more specifically, application development and a market place for those applications. This visual representation of Snowflakes ecosystem is helpful, but this is not up-to-date.

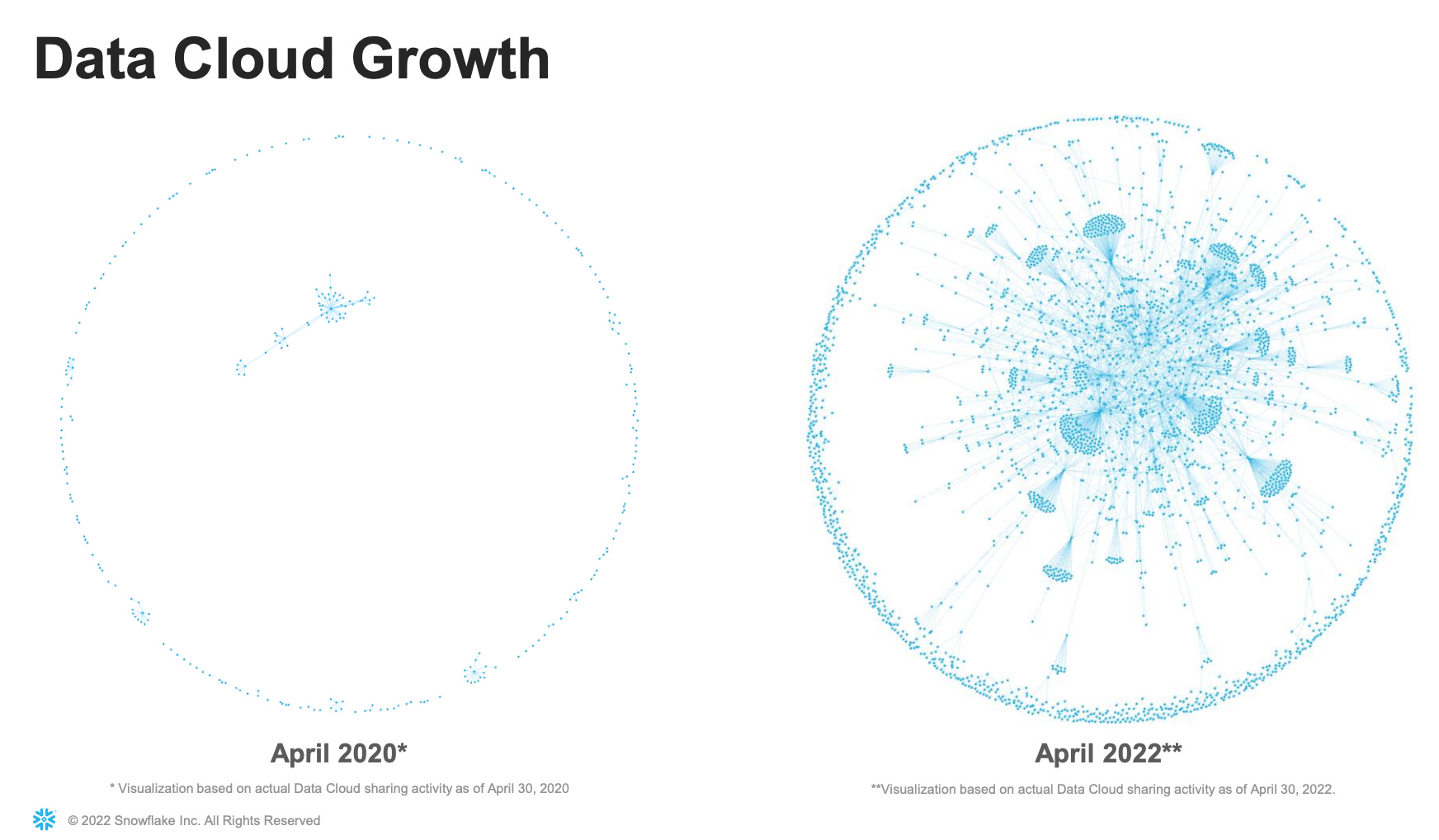

This is accurate as of their latest call:

In simple terms, what exactly does this mean?

It means that businesses can build businesses and products ON TOP OF Snowflakes platform which means that, as a consumption based business model, they will collect revenue from products that sell products on their platform!!!!!!! Basically, this could be bigger than AWS was for Amazon long term.

Full stop.

The long thesis made short, Snowflake has enormous opportunity for the next 20 - 30 years and they have only just begun. With best in class financial metrics and a best in class balance sheet, there’s little to not like about Snowflake and they should be bought on substantial market weakness.

To get a better idea of the details of their financial metrics, Francis did a great job highlighting the key details as he trends this more as an analyst would. If you’re reading this Francis, what up!

My Plan With Snowflake

Making them my largest position wouldn’t be out of the question, for the right price.

My Next SubStack Tomorrow Will Cover My Analysis of the Markets Moving Forward

Opportunity will be had on both the long side and short side of things moving forward in the financial markets. Tomorrow I will talk about portfolio strategy, key technical levels and what was different about Jackson Hole. Make sure you don’t miss it.

Stay Tuned, Stay Classy

Dillon

Wow you do this at spare time!!! Wow, hats off.