Financial Crisis of 2023: Part 1

The Devastating and Historic Banking Crisis Explained.

2022 was a terrible year for all assets as the financial bubble of 2020 and 2021 deflated. We can point the cause of many of today’s problems toward the decisions political leaders and central bankers have made since the COVID-19 pandemic hit. This isn’t a time to point fingers, however, but it is a time to understand how to manage our wealth and the implications of what is happening today. By understanding what is happening today, we can make better choices about our future tomorrow. What worked from 2009 - 2020 won’t work for 2023 - 2030, in my opinion. We need to be smart.

I am under the impression that 2023 is a year that will go down in history as a financial crisis

There are two pieces of this equation that make this a financial crisis and they both directly impact the performance of stocks, bonds and real estate. This means that no matter what kind of investor you are, it’s important to understand how these events all play together. Buying and holding an index, something that has worked so well for so long, will likely not produce the healthy 9%+ returns (from today) that many Americans are used to. Instead, over the next few years:

Inflation will be known more as a structural problem

Interest rates may remain elevated (depending on the choices of policy makers in the months to come)

Real Estate may not appreciate as quick as the standard 10%+ since the bottom of the global financial crisis housing market crash

The banking system will become more commoditized

Of course, I am speaking from today. The future is incredibly difficult to predict past the next 3-6 months. Over the longer term horizon our financial system is destined to change and the best investment that you can make, today, is into yourself and your education. By understanding the workings of today’s economic system, you will fully grasp exactly the severity of the situation that we are in today.

“the best investment you can make, today, is into yourself and your education”

There Are Two Factors that Make Today a Financial Crisis

Since Silicon Valley Bank’s Collapse, I have found myself becoming increasingly more defensive toward the wealth that I manage for my Wife and I. It would behoove me to share “why “I am becoming defensive with everyone to put the appropriate context as to why I am thinking this way. As mentioned above, I believe that there are two components to this financial crisis and they have created a dangerous cycle that will be extremely hard to stop without letting it unwind naturally for a period of time:

Inflation and how a different type of money creation is fueling a dangerous, sticky, inflationary market cycle

The Fractional Reserve banking system is on the verge of collapse due to the inflationary market cycle

Historically, I have been very bullish as we saw substantial progress from inflation. In the 1970’s we saw the market bottom every single time inflation peaked. However, if many recall, I posted this newsletter back in February:

To simplify exactly what I mentioned above, I was concerned about the Federal Reserve’s ongoing QT (quantitative tightening) and the stress that it was likely to put onto the banking system. Of course, the Federal Reserve did over tighten and withdrew too much banking system liquidity in the form of bank reserves. However, it wasn’t the large banks that felt it, it was the small banks.

It wasn’t just banking system liquidity that has created this problem though, it was the Fed’s blind disregard for how they fueled an asset bubble and popped it. The asset bubble, this time, was in bonds. Understanding the bond market component is crucial to tying this whole piece of the puzzle together.

Factor 1: The Bond Market Bubble that has Popped and the Threat to the Fractional Reserve Banking System

This can become an extraordinarily complex topic, quick, but there are three things to really be aware of here:

Why banks hold US Treasuries on their balance sheet

How the present value of a bond fluctuates

What actually banks do with the cash that you give them to hold

Banks are a For-Profit Business

Profitability can sometimes be politicized but what it’s really reflective of is the efficiency of a business model. When it comes to banking, they are incentivized to give loans, or lend money, it exchange for profit in the form of interest. In other words, banks are incentivized to create debt to make more money. To (very) simply explain:

This is an extremely simple example. The actual interest on the first year is variable to the monthly payment from principle and interest amount as well as how it’s compounded. The goal here is to just understand the concept of interest being bank profit.

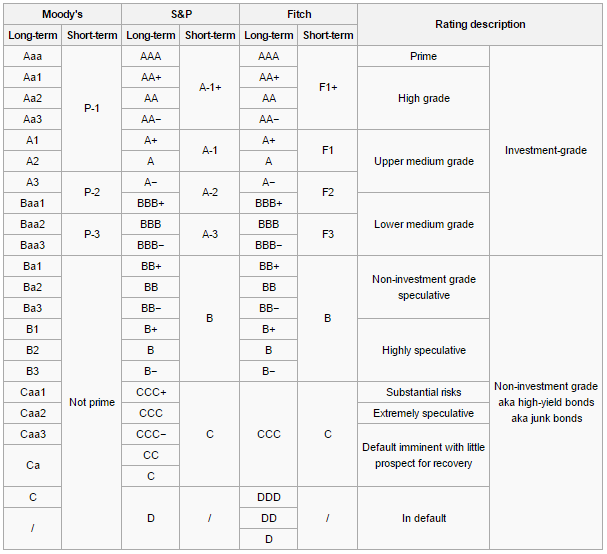

Lending is rated on a scale from most risky to least risky. The most risky being subprime (think somebody with a credit score of 550)/distressed debt and the least risky being US Government debt (because the US Government cannot default on their debt). The risk scale is important to banks to ensure they are “managing risk” or “default risk” on those loans. Recall how I mentioned that US Government debt is the least risky. In the example below, this can be considered AAA, or “prime” credit. This means that it’s “as good as money”.

Book mark the “as good as money” comment in your mind. We need to cover, briefly, what banks do with your deposited money.

When You Give Banks Your Money, they Actually Re-Lend Your Money to Make More Money

I could write an entire substack on the fractional reserve banking system but we are going to hyper focus on what banks do with your money and why. At the very nuts and bolts of how our whole system works, banks will take money that you have and re-lend it out. They can lend this money out to other people, businesses or the US Government. It works a lot like this.

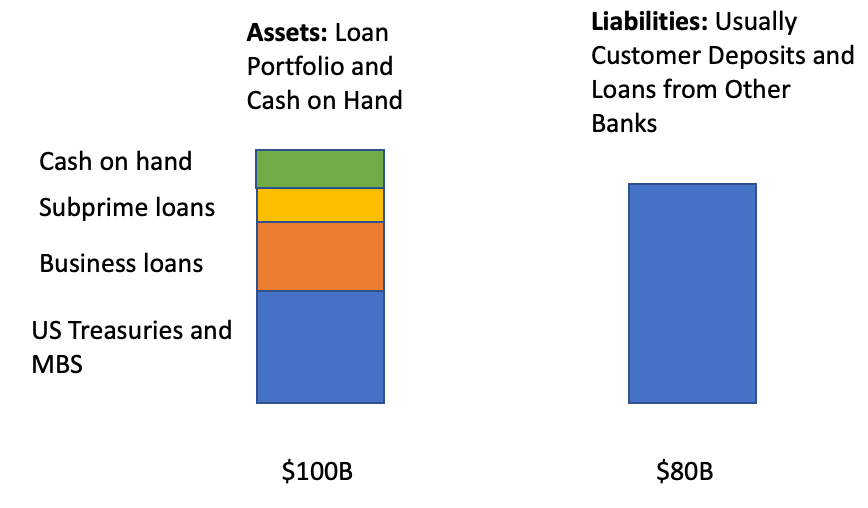

Recall above how I mentioned that banks will manage risk by ensuring that they are buying highest quality credit first and lowest quality credit second. The lowest quality credit is often the most profitable but the risk of default is higher than something like the US Government, which has that AAA rating. Typically, what banks balance sheet usually breaks down to something like this at it’s most simple form:

Alright, pay attention to how assets must be larger than liabilities for a bank. That’s the sign of a healthy bank. We are going to shift our focus now on what is going on today, what happened in the credit markets and why the entire banking system is at risk due to the Feds actions. To bring this full circle, we need to talk about how a bond is valued but keep in your mind how assets must be higher than liabilities for a bank to be healthy.

The Present Value of a Bond

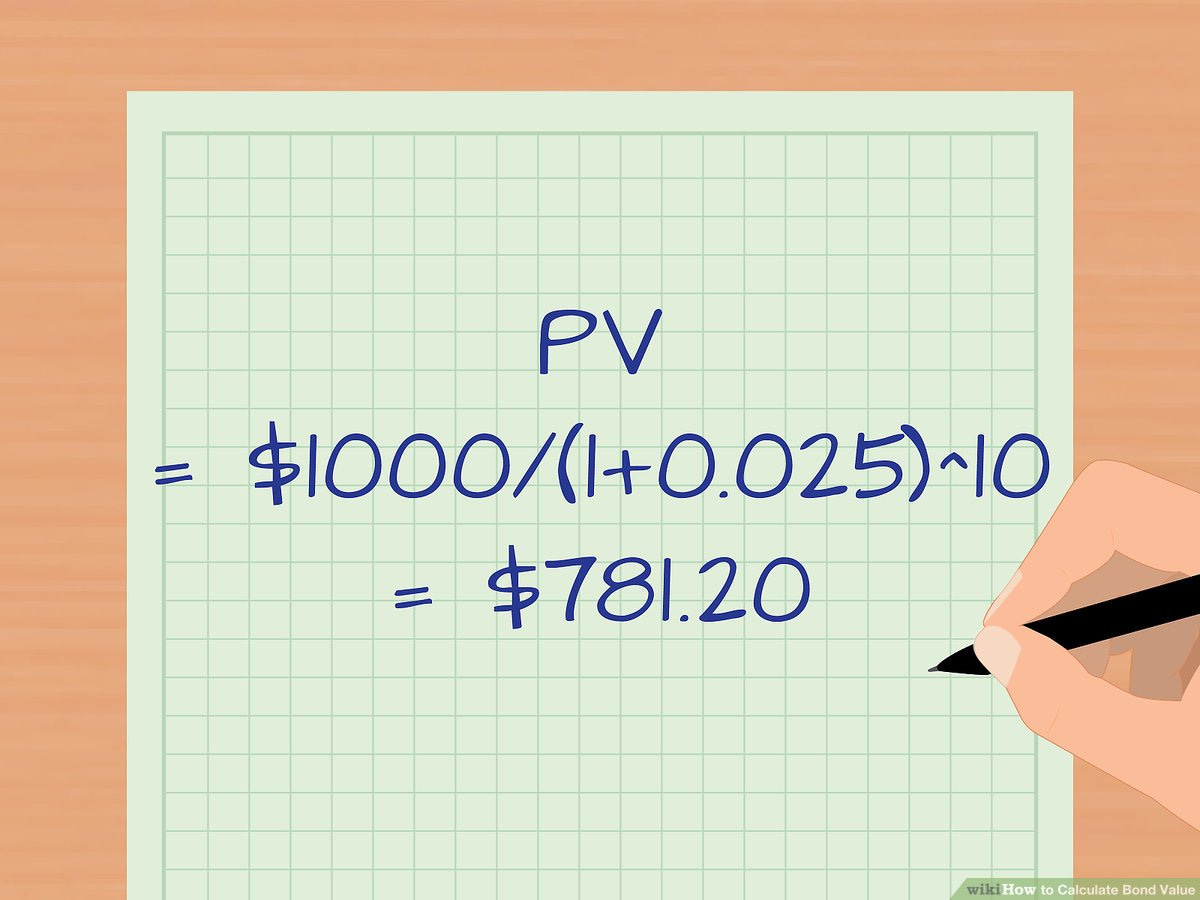

Just like the fractional banking system, I could write an entire newsletter on how the present value of a bond can be calculated and how this all has a relationship. But for the purpose of today, we need to focus primarily on the US T-Bills, or US Treasuries, or Government Bonds market. When somebody buys a government bond, you can either buy it directly from the US or on the open market. The value of that bond is usually calculated with some sort of present value discounted for the expected yield in the future.

The above is an extremely simple example of how to calculate the present value of a bond. This can be broken down to:

$1,000 is considered the face value

Interest is 2.5%

10 years to maturity

$781.20 is the present value of the bond before maturity

The present value is the value somebody is willing to buy a bond for based on today’s MARKET INTEREST RATE. Today’s market interest rate is the most important piece to this puzzle to understand the severity and threat to today’s US Banking System.

WHEN THE FEDERAL RESERVE HIKED RATES FASTER THAN ANY OTHER TIME IN HISTORY, THEY FUNDAMENTALLY DECREASED THE VALUE OF DEBT (BONDS) IN THE US BANKING SYSTEM

Recall the image above where the present value of the bond is $781.20 based on the interest rate being 2.5%. If the market interest rate rapidly increased from 2.5% to 5%, the present value of the bond is now $613.91. THIS IS A 21.5% LOSS IN VALUE on that bond, based on the current market price. This of this as a giant black hole that exists in the financial system today, that money was lost and that wealth was destroyed.

Now, the way bonds are valued is that they have a “face value” (to maturity) that’s absolute. In this case, it’s $1,000. If the bank held on to the bond until maturity there would be no harm, no foul. The bank would receive the full $1,000 bank. However, the problem begins when people begin requesting their money from the bank (or when the money supply begins to decrease) when the cost to borrow has rapidly increased and the value of all their assets decreased.

Recall this image

At it’s very simplest form, all banks (if they didn’t hedge interest rate risk) look like this now

The U.S. Banking System is Sitting on Hundreds of Billions, Possibly Trillions, of Dollars in Unrealized Losses Because the Fed Raised Rates so Fast

To bring this full circle, the entire banking system would collapse if the FDIC or the Federal Reserve did nothing (even though it’s their fault in the first place). Banks are supposed to hedge risk, which is where people are saying that SVB was a poorly managed bank, and this includes interest rate risk. In other words, banks know and understand how to calculate the present value of their loan book. However, in the world of statistics, you rarely compensate for an incredibly unlikely event.

So if you held US Government Securities, thinking they are “risk free” or if you grossly miscalculated how high the Fed would need to raise rates, you run the risk of defaulting and blowing up your bank. This problem isn’t just applicable to the United States banks, however, it is a global banking problem. Look no further than Credit Suisse, which has billions of dollars in losses.

Factor 2: The Ongoing Inflation Fight is NOT Over

I am going to point you, the reader, why a systemic problem like banking defaults is a serious issue to the same substack posted above:

This publication (above) is extremely important to read to fully understand what I am saying and the gravity of the scenario that we are in. For the first half of the Substack above, I talk about how the Great Depression started and how the Global Financial crisis happened. More importantly, how the Global Financial Crisis did not become the next Great Depression. In the most simple of words, they printed money and a lot of it to prevent a global depression in 2008 and 2020.

There is a way out of the problem above (with the banking crisis) and that’s to do exactly what you did in 2008 and 2020 (print money). However, the issue becomes when you are fighting inflation. Policy makers effectively created inflation to offset deflation in both 2008 and 2020. In other words, massive government spending coupled with flooding the market with dollars prevented a deflationary unwind. The problem is that when you print a lot of money, you get inflation.

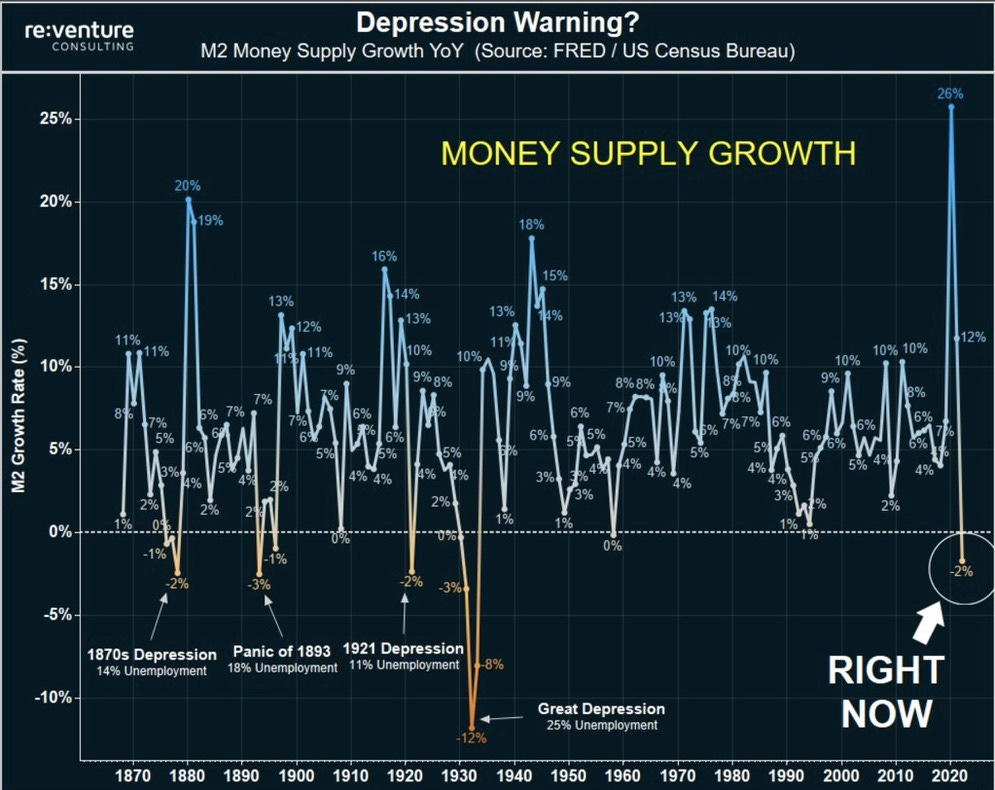

This is best reflected in the M2 growth over the past few years. We increased the money supply by near 30%, rapidly, which created inflation.

It’s simple math really. The price of goods and services is absolute, meaning the value doesn’t change. We need water, vehicles, food, housing, etc. Dollars are just a mean of exchange for these commodities/services. When you flood the market with dollars, you give more people dollars, which allows people to spend more money increasing the demand side of the equation. The price is almost always higher prices.

Imagine demand represents the good/service and supply represents dollars. When the blue line moves upward, to reflect a higher supply of dollars, demand temporarily surges until market equilibrium is once again found also known as “the market clearing price”.

Money Creation, Money Printing and the Dangerous Cycle We are In

You create money in two ways:

Bank lending

US Government deficit spending

In my next news letter, I will cover money printing on how we are in a dangerous inflationary cycle that can likely last years. We are going to talk about the US Government, how it’s actually the Federal Government that’s causing this and what the likely path forward is in the next few years to come. In the mean time, let me simplify the purpose, conclusion and point I am trying to make here.

We Need Inflation to Come Down to Solve the Banking Crisis. However, Inflation is Still high. If the Fed Acts Now, they Risk Losing the Inflation Battle. They Only Have One Option Today… They Must Keep Patching the Holes in the Banking System, Keep Rates High and Immediately Stop QT While “Hoping” Inflation Comes Down.

This means that we are in for a ride. The Economy must continue to ‘wind down’ from recent historic stimulus which will impact all asset prices in the months to come. More banks will likely have to default and soon, businesses will start going out of business as well. This will be a recession and we need to go through it. As much as I want to be optimistic, I do believe now is a time to play defense with present capital.

Stay Tuned, Stay Classy

Dillon

Good overview, easy to digest. Much appreciated