FuboTV: Competitive Moat, Earnings, and Profitability

FuboTV and the story behind the stock

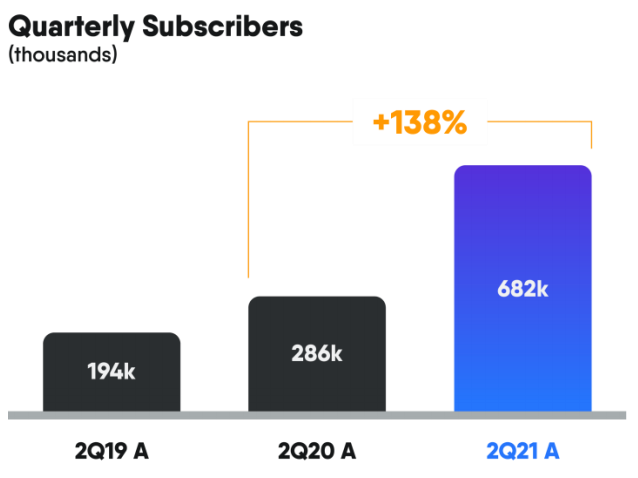

FuboTV has many investors blown away, how can a small streaming business

accomplish this growth and capture this much market share? Top-line financial metrics for reference:

Since Fubo IPO’d, I’ve owned this stock. There are few stocks I own that have this much divide between Bull’s and Bears. I’m a Bull, because there’s a story, a path to profitability, and a potential 10x stock.

Fubo’s business is unique in the sense that it does take a sports first streaming approach. There are many streaming players, but there are none who have put up the costs it takes to run a sports first streaming service and with this depth of content in their offering.

Article referenced: https://www.reviews.org/tv-service/best-sports-streaming-services/

From the surface level, the extent of the sports offering is the most broad among its competitors, this caught my attention. But this is only part of the investment thesis.

What really caught my attention was the hyper growth. Typically when I see businesses growing this fast, I can’t help but research the business to discover their competitive moat. The answer here may surprise you, but the answer lies within their leadership. As David Gandler (CEO and Co-Founder) said on his Q1 earnings call, “what we do really well is collect data and use it efficiently”. They are efficient operators.

It’s not just what the business has done, it’s where they’re going, their competitive moat. As I continued to dig into this business model I began to really understand what they were. They’re not a streaming company, they’re a sports company and look to bring this to life through interactivity. The way they see it, they’re focused on acquiring sports viewers and finding new ways to monetize them, primarily through:

Paying subscriptions ranging from $30 - $80 (depending on the package)

Advertising, much like cable TV

Sports wagering

Yes, sports wagering, this is where it gets interesting. There is not a business out there that can integrate streaming TV with interactive, real time, sports betting and interaction. They are the first business that is pursing a real time interactive interface between your mobile phone and CTV. The primary use case here is sports wagering. This is what it will look:

The use case(s) for this seem unlimited, a technology that links and interacts with your TV or more specifically in this case, within Fubo’s infrastructure. This will allow users to watch their favorite sporting event which can be Soccer, Basketball, Football, etc and allow them to place up to the minute wagers. DraftKings may be the closest to this technology, and on their latest earnings call they said they were going to release plans to do something in the “media space”. However, Fubo is a first mover and you can tell that DraftKings sees this potential as well and when leaders try to follow a disruptor, it usually doesn’t work. Think Roku with their OS and TV’s, the big dogs are still trying to play catch up.

This is usually where people think to themselves, is this even possible? This is going to cost money and FUBO is running on borrowed time. The way I look at it; they have $400m in cash, they need to get their streaming service to break even and they need to be successful with their Sports-Book launch. As far as their streaming service breaking even and reaching profitability with their sports book integration, I’ll give you guys the option to see the numbers and reference you to this Tweet:

In short what that thread is saying is yes, they can reach profitability and they can pull this off. By continuing to expand on their advertising offering and scaling subscribers, they can get there. With an 8% adjusted contribution margin, they’re getting close. Ideally the streaming service adjusted contribution margin would need to see 15%-ish to start seeing a potential for profitability, I think they can get there.

This leads me to the biggest risk with FUBO, the execution risk is very high but not impossible. The scenario to profitability assumes a successful tech integration, a smooth operating platform (some wagering platforms are clunky), and Fubo viewer adoption/expansion. If I had to rank these risk it would be like:

Smooth operating platform

Tech integration

Viewer adoption/expansion

There’s also regulatory risk, but that’s pretty universal for all sports wagering operators. Obviously these are my subjective views and there’s many other cases for why something that hasn’t been fully implemented yet, wont work. But, in this particular instance completing a major project like this on budget and on time takes a unique mindset, leader, and team.

It’s a bet I’m willing to take and also, my portfolio allocation is appropriate. I’m position sizing correctly to not be killed if it doesn’t work but can still can catch meaningful upside if it does. This is a speculative position, one I am very excited about and as a fundamental driven investor, I don’t take many of these positions often. However, their recent execution against the odds lead me to believe they will continue to execute against future challenges and meet expectations.

Stay tuned.. stay classy,

Dillon