Global-E Q2 Earnings in Review

Global-E Q2 Earnings in Review

GLBE business, Financial Statements and Long Term Thesis

Global-E is gearing up to be a long term e-commerce winner and their partnership with Shopify (Shopify bought a portion of Global-E during it’s IPO) is proving to be an instant success and long term, will continue to reward more accelerated returns for patient investors. Especially as Shopify’s largest customers begin to use GLBE. If Shopify wins, Global-E wins and vise versa.

When mentioning that they’re an e-commerce company, and before talking about financial results, it’s important to understand exactly how they make money and their competitive niche. Global-E is an enabler of international, cross-border, e-commerce. When businesses sell into other countries there are many rules, regulations, currency exchanges, and language barriers that come into place. This is where Global-E comes in.

They make cross boarder e-commerce a fast reality and reduce the complexity. In addition to the capabilities above, they assist with localized browsing, checkout, logistics, market insights, and risk managment/regulation. They claim that this has led to stunning results for their clients where they can see international online orders increase 100%+.

Post earnings, GLBE quickly rallied 14% on market open the day after but dwindled as the selling pressure from the broader market caught up to them, ending the day 1.13%. This tells me many investors are very excited (almost euphoric) about this stock. Needless to say, their earnings results were good, but how good?

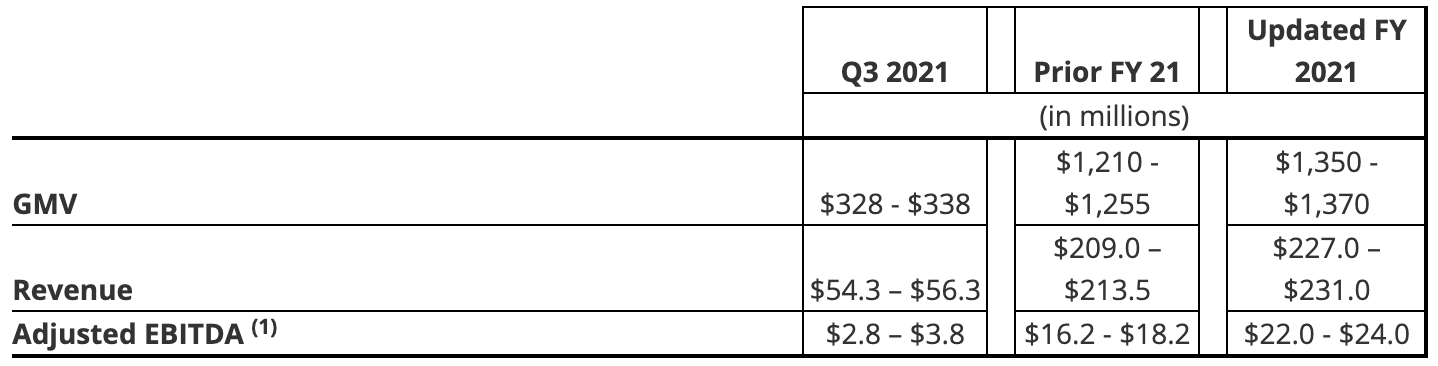

Earnings highlights:

GMV (gross merchandise volume) hit $326m, an increase of 95% YoY

Revenue was $57.3m, an increase in 92% YoY

Gross Margin expanded to 36%, up from 32.4% last year

Adjusted EBITDA was $7.6m compared to $3.1m last year

Net loss was ($22.2)m compared to ($.4) a year ago. This was primarily attributable to Shopify’s warrants.

The most important thing to take from these metrics is that Global-E is growing very, very fast and will continue to do so for the forseeable future. But where they really won was the continued expansion of the gross profit margin. As they mentioned on their earnings call, they continue to expand their gross margin as their business scales, very bullish. This means that they can be profitable today if they chose to be, but they also mention that they will invest in their company for the forseeable future to capture their market growth. This can lead to a sacrifice of short term profits. As an investor, I am ok with this especially knowing this business can be profitable if they choose to be. There will inevitably be competitors in this space and they have to move quickly to capture as much marketshare as possible to be dominant market leaders in crossboarder e-commerce.

Their guidance was equally as good as their latest quarterly results:

They raised full year guidance from roughly $210m to $227m-$231m while accounting for Shopify’s boost in new revenue. This will represent approximately 70% YoY growth for GLBE. However, this brings me to my top concern with this stock and that is it’s valuation compared to EBITDA, Gross Margin % and growth rate to justify it. Currently their market cap is fluctuating from $9B - $10B, if we break down their metrics it is substantially higher than their peers. How this breaks down (using a $9.5B market cap):

41x FY21 PS, and 27 FY22 P/S

108x FY21 EV/GP (enterprise value to gross profit)

375x FY21 EV/EBITDA, 118x NTM (next twelve months) EV/EBITDA

NTM Forward P/E 345x

Needless to stay, this is expensive and currently presents a very unattractive risk/reward at this price. But, there’s a few catalysts upcoming for you guys to think about. At the moment, they still have their IPO lockup and it expires on November 8th. This always seems to create selling pressure as VC’s and insiders rush to sell their immense gains from the initital IPO price of $24/share, a 291% increase from IPO. Also, there’s no question the market is wobbly with taper talks looming at every corner (this never changes) and any hint at the fed starting tapering will surely create a self-fulfilling prophecy and a broader market correction. Couple multiple negative catalysts upcoming, I may believe I may have an opportunity to add heavily to my original position I started at $30.

Conclusion: It’s hard to imagine that GLBE doesn’t have a very long runway for growth. This is the makings of a multi-bagger investment for the long term share holder (speaking my language here). Patience will be key when adding or beginning a position in this business, I’d like to make it one of my top 3. I’ll continue to keep you guys updated through this substack and my YouTube channel.

Stay tuned… Stay classy,

Dillon