Global-E's Thesis & Latest Financial Results

Global-E's Thesis & Latest Financial Results

Opportunity, Business Analysis, & Latest Earnings

I am confidently under the impression that now is the time to micro-analyze companies and buy. By micro-analyze, what I mean by that is that we have to get our stock picks right.

Because of this, I am announcing a new series of the top 10 stocks I have followed for the past few years that I believe will not only sustain through this turbulent economy but continue to thrive.

For each company, I will provide my thesis on the business, potential risks to pay attention to, and provide in depth analysis on their financial statements. The purpose behind this is to maximize this opportunity to a point where people look at us and say, “that’s an amazing cost cost basis, how in the world did you know?!” 3-5 years from now.

I have already done 1 of 10 with DLocal and I received wonderful feedback with the format. Because of this, I will keep it consistent with today’s company ,Global-E, where we will cover:

Business product & thesis

Analyze latest financial results, balance sheet and cash flow statement

Provide an update to the thesis from the latest quarterly results

Global-E Thesis & Earnings

The best way to think about Global-E is an extension to the businesses that they work with. To make sense of this more, we must first understand and define exactly what they do as well as the challenges their customers face.

In the most simplest form, they provide a direct international business to consumer platform for their customers. That means that a company in the U.S. does not need to hire its own international team to both sell and distribute their products internationally, they can just hire Global-E. There are three layers to this type of logistics platform:

Localization: They are able to integrate directly with the native platform they are currently using (think Shopify stores) and quickly translate all language barriers to 200+ countries all over the world. For example, somebody in Singapore can log in to an American merchant store through Global-E’s integration without having to create something new or write new code for a different language.

Payments: They have the ability to accept payment from 100+ different currencies all over the world with the payment methods that work best for the consumer in that specific region. In addition, they are also able to guarantee a ForEx rate for their consumers to decrease volatility in markets and handle any sort of cross boarder regulations or taxes when it comes to the transactions.

Shipping & Logistics: Rather than the merchant seeking to find, or hire, their own supply lines they can lean on Global-E to take care of all this for them. Because they specialize in international trade and cross boarder commerce, they have a robust network of shipping partners that make for a seamless experience for their customers.

By leveraging all three of these components to Global-E’s business model, they find a deep rooted competitive advantage through data collection. In plain english, they specialize in the logistical frame work with international e-commerce so all their merchants need to do is produce their goods and do what they do best. This deep integration with more clients globally creates a larger moat for Global-E because, with scale, they become more efficient at what they do. Their platform becomes a mission critical component for their merchants long term expansion opportunities.

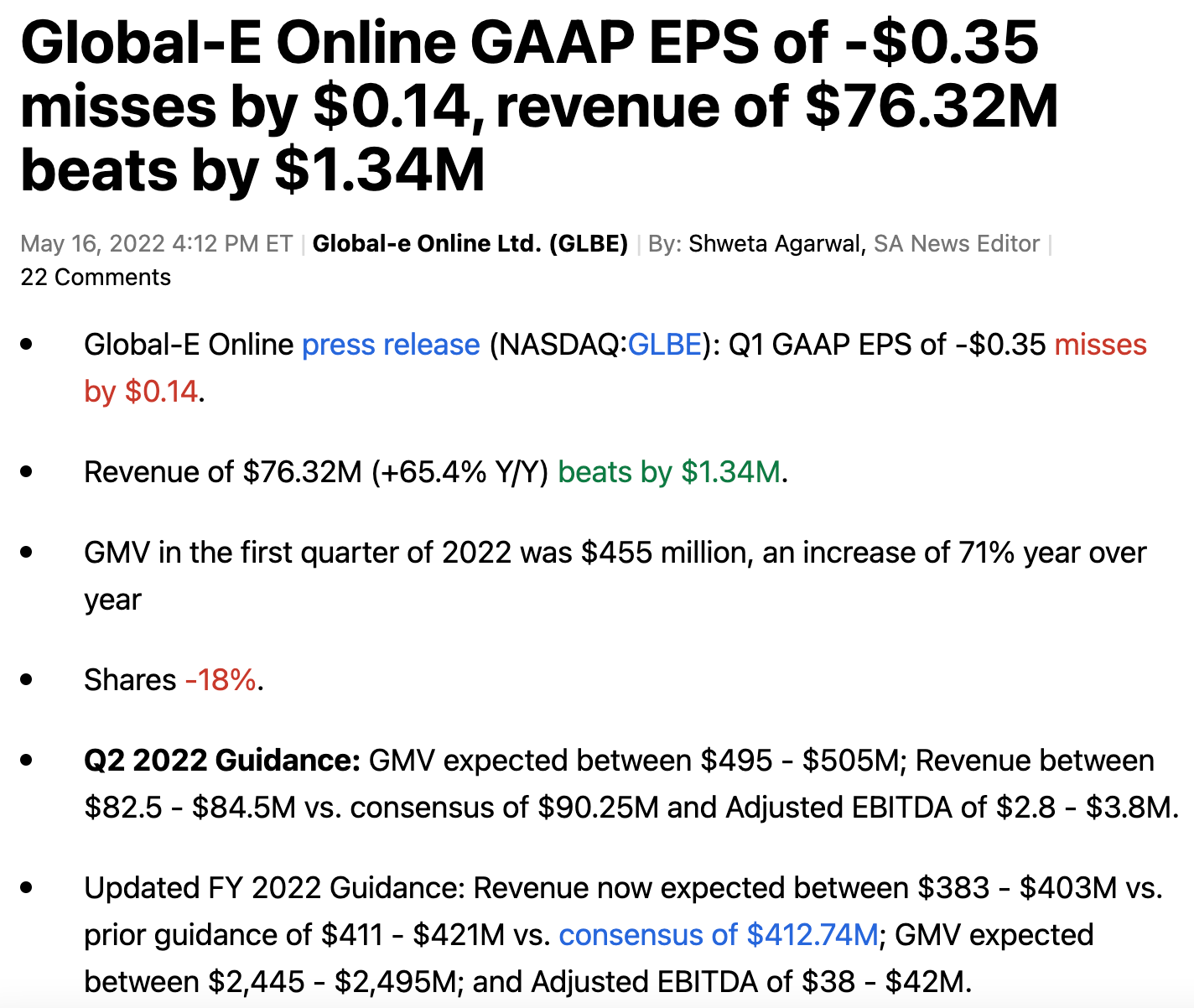

Q1 Results

Global-E sold off on earnings when investors overreacted to the guide down in their full year guidance. From where it was, it was about a 5% decrease. On their earnings call, they mentioned that approximately 2% - 2.5% of their revenue was tied up in Russia/Belarus/Ukraine, so it appears obvious that pulling out of Russia/Belarus would have an impact on their top line. However, they noticed that all of eastern Europe was disrupted economically because of the war and that they believe that, in total, they may see about a 5% impact in their revenue guide. Usually I don’t give a pass to businesses when they guide down but being an international e-commerce business, geo-political risks will always be present.

For their recent quarters results, they missed on the bottom line, beat on the top line and lowered Q2 guidance. What frustrates me is that “analysts” are setting these expectations and apparently this is what creates short term fluctuations in the stock. The details are what matters. Here are a few key points that I find very important:

They still managed to grow 65.4% during a period many businesses are reporting less than 20% growth

They guided for strong, and expanding, adjusted EBITDA, which will be closely correlated to free cash flow

Their guidance, as mentioned on the call, has macroeconomic risks baked in. As they mentioned, they don’t expect the macro environment to get better, especially in Eastern Europe.

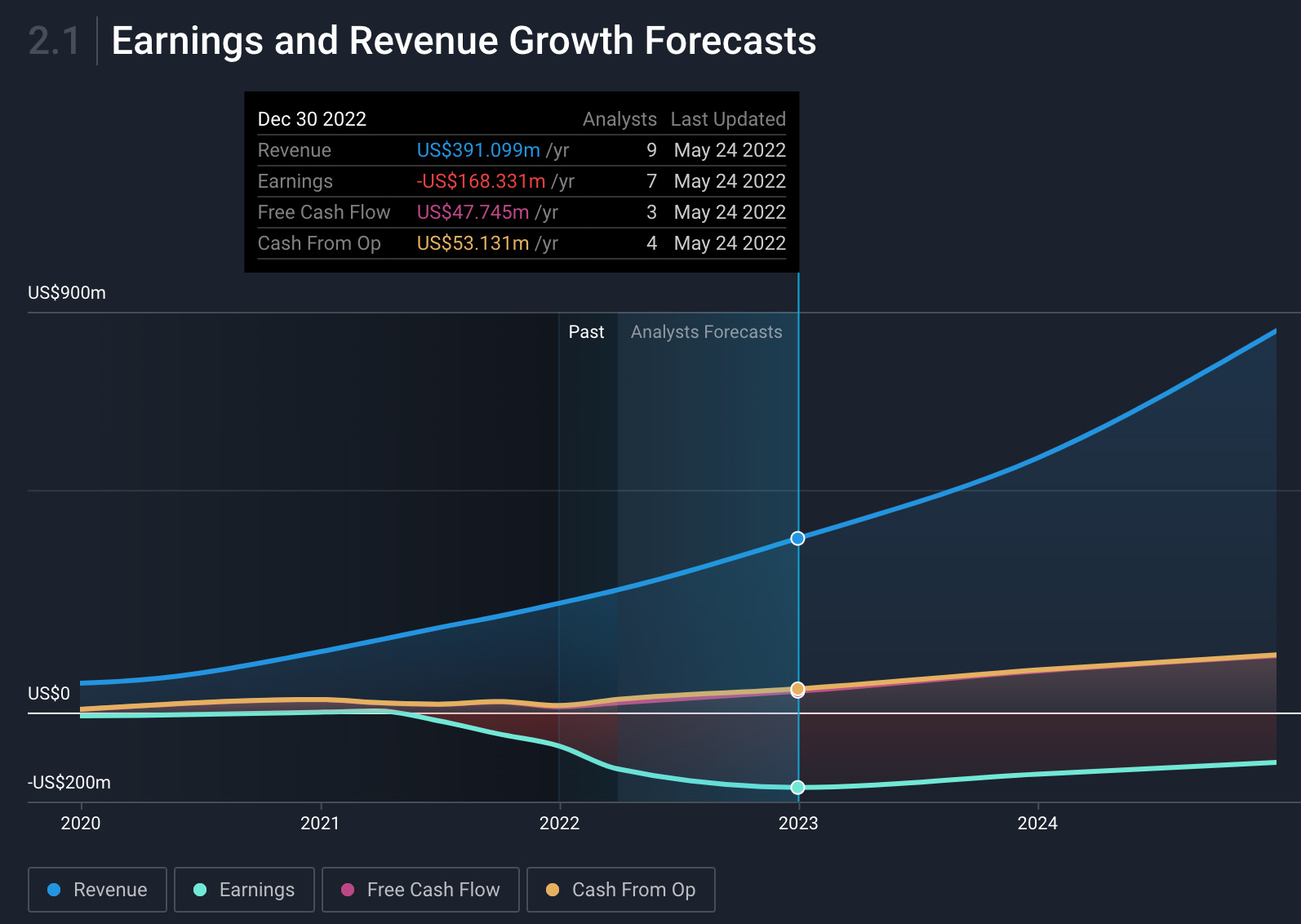

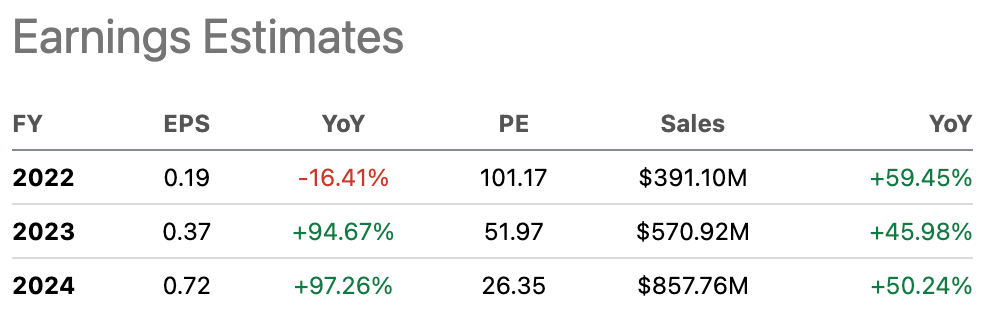

Despite missing analyst expectations, they are still projected for exponential growth and cash flow in the years to come

From today’s valuation, Global-E is expected to continue high revenue growth and have a projected P/E of less than 30 by 2024 with 45%+ growth CAGR in the in years to come

Income Statement

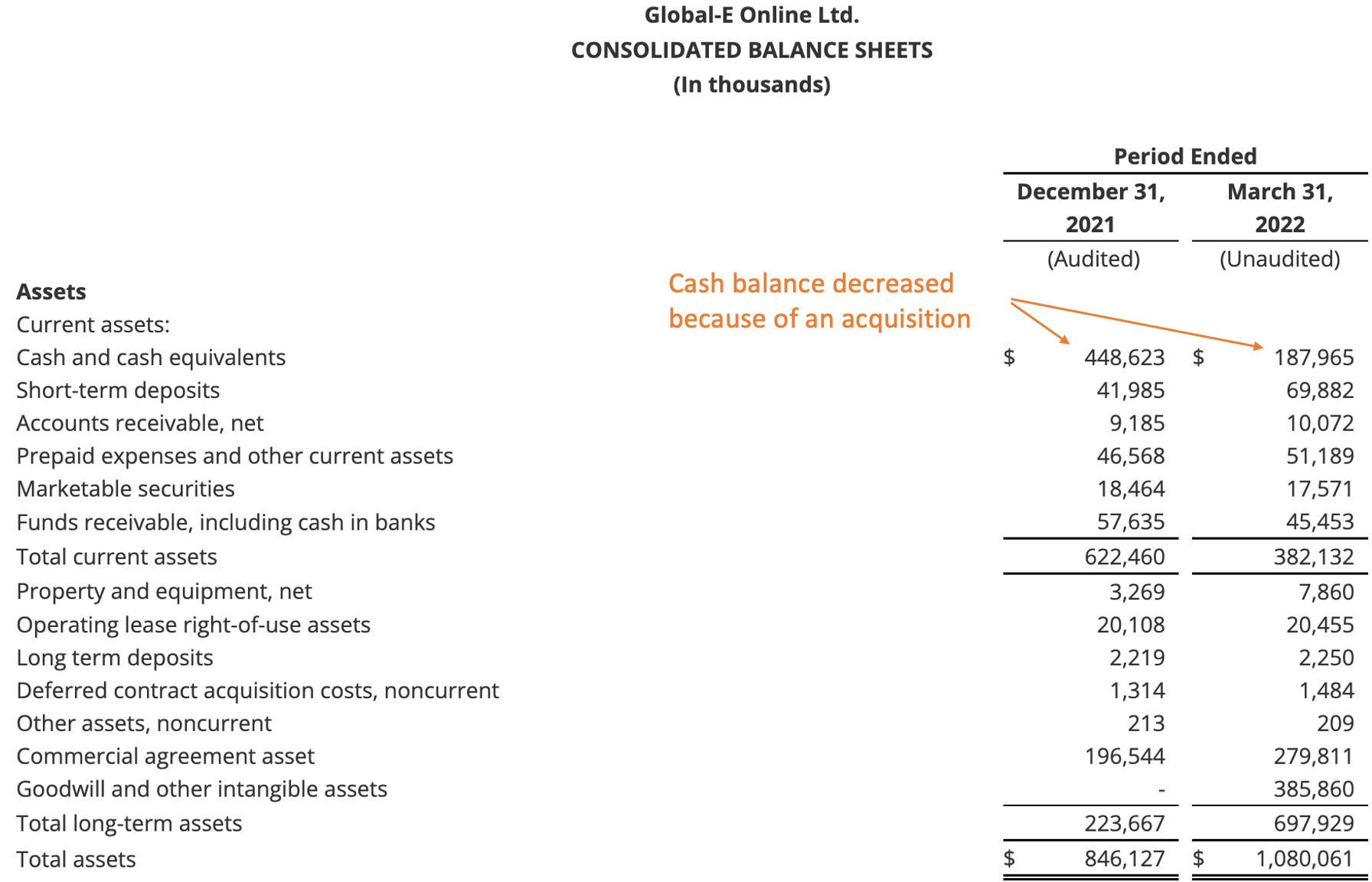

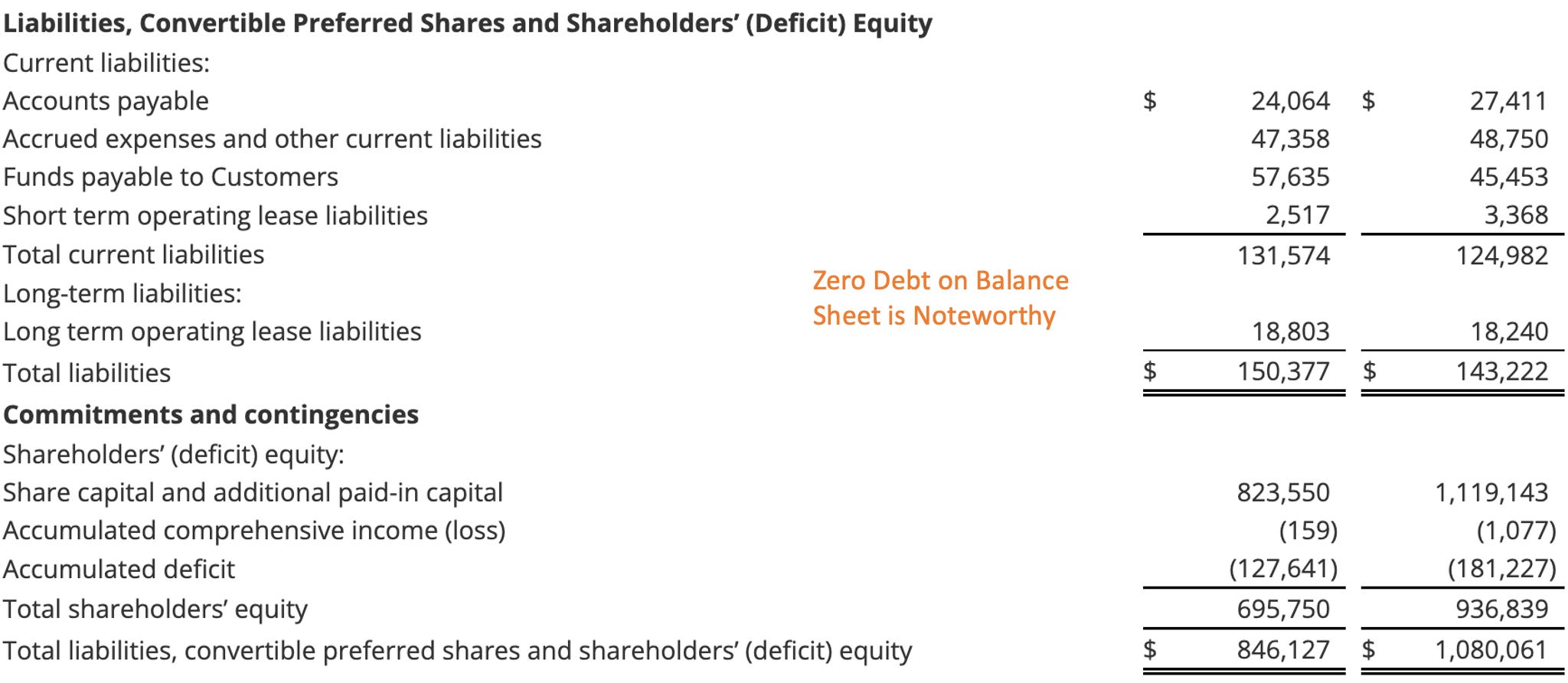

Balance Sheet

Interpretation of Financial Results

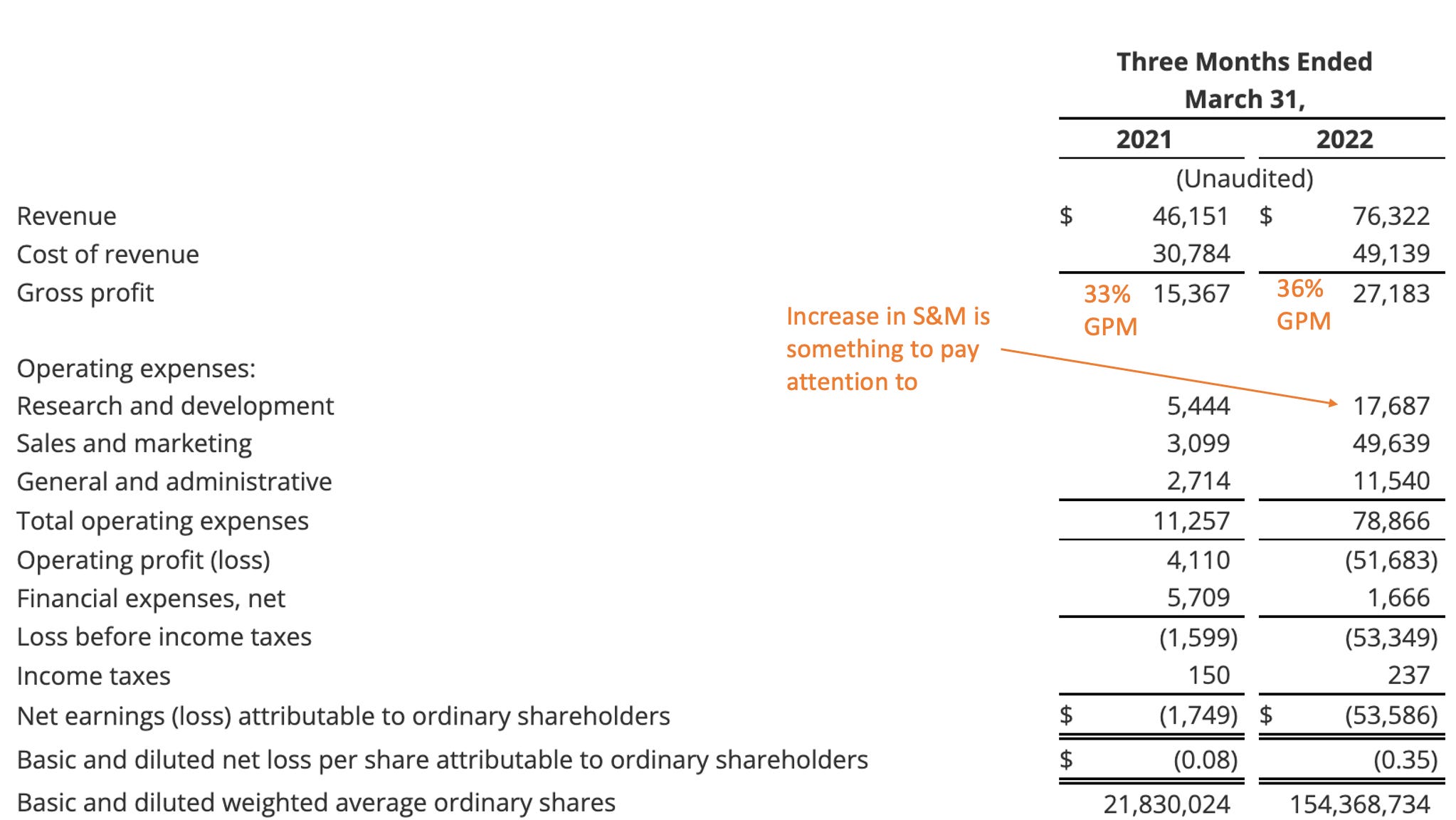

Global-E’s growth and business model are the first things that attract me the most to this long term investment. From there, my mind usually goes straight to the cash on hand and their financial flexibility to execute their long term goals. Above, I annotated a few of the areas we, as investors, should be paying attention to. Let’s touch on each briefly:

Their gross profit margin continues to expand and it did decline slightly from Q4. I do not expect it to continue to keep going up but YoY expansion will be important. Long term, with scale, I believe they can get to roughly 50% GPM which will increase their ability to be profitable.

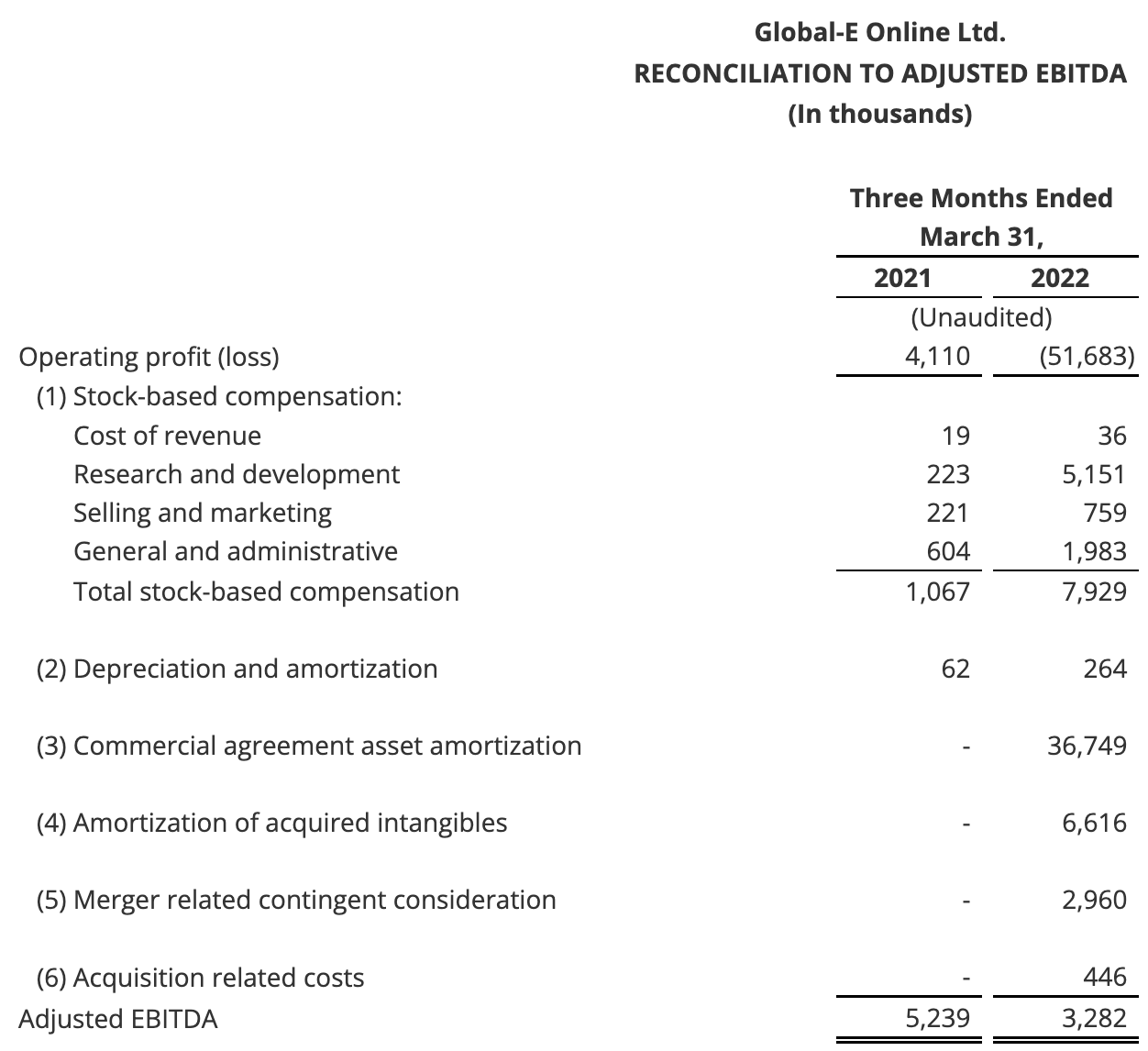

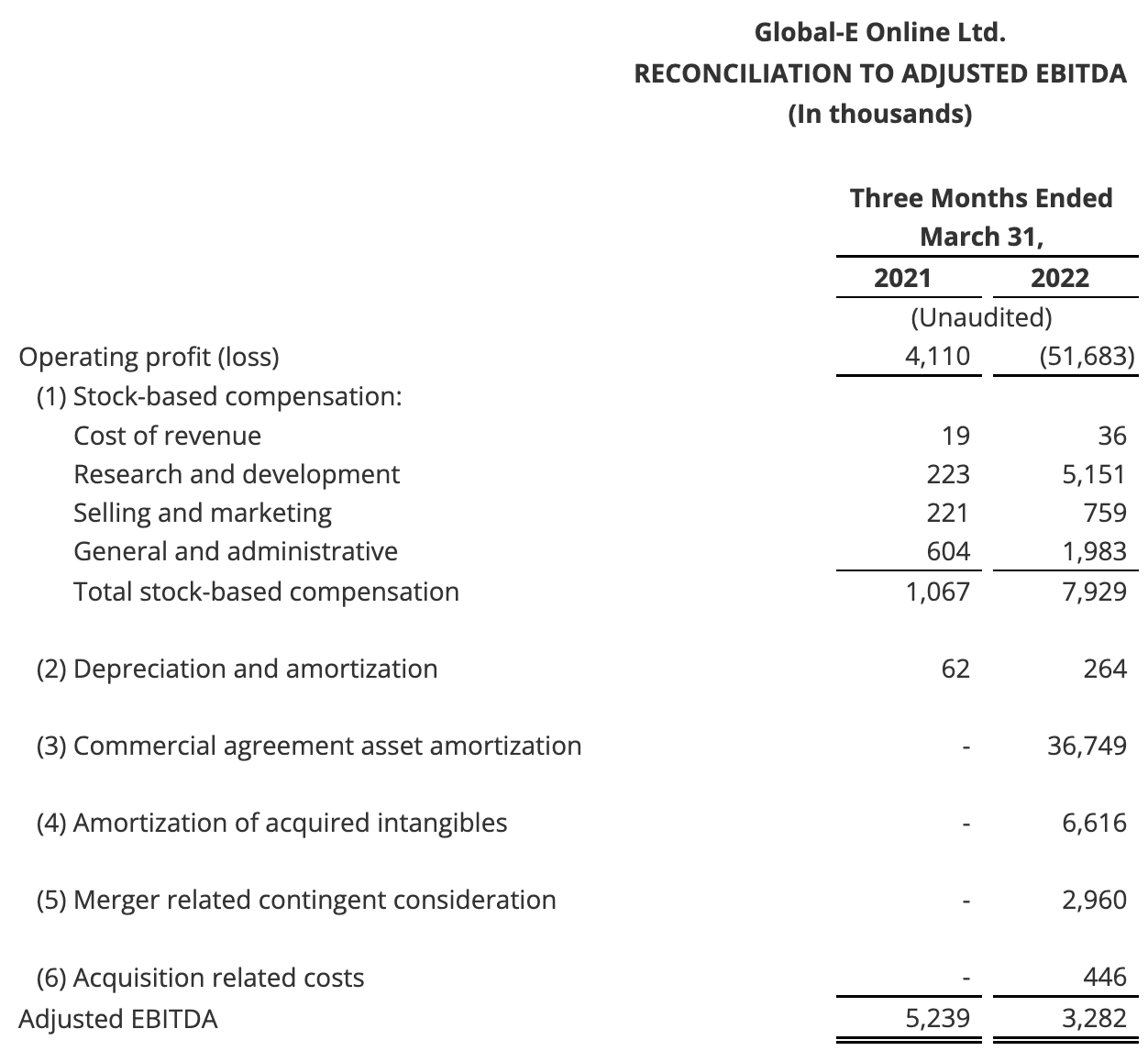

I did notice that they increase spend with sales and marketing which is typically an issue especially if they are not being efficient. However, there are two important details here. 1.) Their adjusted EBITDA (their operating profitability excluding one time expenses as well as stock based compensation) was still positive. This metric should never be relied upon soley but it gives you an idea where they are at and how they are managing cash.

2.) Refer back to their guidance (above) where their adjusted EBITDA for the full year is expected to be $38m - $42m. In their earnings call they mentioned that this will roughly be their free cash flow for the business. This tells me that, in the quarters ahead, we should see better cash management for the year. This is something investors should be paying attention to.

Cash balance is getting low, but they have no debt. Typically, I invest into companies that have a high cash balance with little to no debt. The reason why I do this is that it provides flexibility to fund growth initiatives. The decreased cash balance is of concern but I do not worry much about this because they guided for positive cash flow for the entire year. In addition, their balance sheet is exceptional on an assets vs liabilities perspective. Total assets exceed $1B with total liabilities roughly $143m, meaning this provides them flexibility to take debt if they need to. I doubt they will take any debt or do an equity offering till the macro environment improves.

There are risks that we need to pay attention to, like any company, but the long term growth story is fully intact and their have the financials to execute their long term growth goals. Nothing comes without risk but it’s important for us as investors to be aware of the financial risks.

Updated Thesis & What I Plan to Do

I recently added to my Global-E position. What’s exceptional is that they are continuing to grow during a period e-commerce as a whole is struggling, which tells me there is a A LOT of demand for their services. Also, during the call this thesis was validated by them mentioning that they continue to see an acceleration of clients onboarding to their platform. Accelerating client demand is a major reason why I did add more GLBE.

In addition to listening to their conference call, I also tuned into a few of their investor conferences to see what their long term vision is. Everything I am seeing, as far as the story goes, continues to improve. A few important take away’s:

They expect to have EBITDA margins of roughly 20%+ in the next few years with continued growth of 40%+

Client demand is massive and they are seeing that merchant psychology is shifting toward digital international commerce

Globalization of commerce is not going away despite temporary macro headwinds in Eastern Europe

They are still a tiny company with a very large, massive TAM

Their exclusive Shopify partnership is a crucial piece to this story. Shopify owns roughly 10% of Global-E which makes them an exclusive provider for Shopify’s biggest clients

The biggest risks I see, after their call, are:

Macro risks, obviously, with higher interest rates and the high possibility of a global recession.

The state of the global economy and potential for world war three. This is a thesis changer.

A decrease in the cash balance making it a little too low for my liking. I need to see an improvement in cash balance on their next call. I would like to see them get closer and stay above $200m in cash & equivalents.

Let me know what you think about Global-E’s thesis or perceived risks:

I already have added more and my ultimate plan is to keep adding to them in this year of uncertainty. After all, this is the year of accumulation. In addition, I will continue to keep you guys (members) updated on what I do with Global-E long term. When I move on from stocks there’s usually a business reason and not just because the stock price goes down. As far as I see it currently, Global-E’s market cap is currently $3b making it possible to be a 10-bagger stock from its currently valuation. If they manage to grow their revenue to $2b, continue improving their gross margins and achieve the 20% EBITDA margins this will be a company people will look back on and wish they added during this time.

For my next article, I plan on doing Confluent. Confluent is a data infrastructure stock growing very fast, with a ton of cash, and nearly operating cash flow positive (expected 2024). You’ll be surprised with what they do.

Stay Tuned, Stay Classy

Dillon

Nice work here, Dillon. Really appreciate the thorough overview as well as getting your take on their risks. They'll face a lot of execution pressure in the coming months, but they're building the groundwork for something special.

Looking forward to more company updates like these!

Your content is fantastic. Really appreciate it man. I tried reaching out on Twitter but do you use stop losses using technicals like $DLO for example with its recent price action of doubling from ATL. My Twitter handle is @MC34878943 if direct messaging is easier