Growth Has Become Value - 10 Stocks I Track and Their Multiples

Growth Has Become Value - 10 Stocks I Track and Their Multiples

Laying out where multiples lie today using EBITDA, Gross Profit, Earnings, and PEG ratio

The Markets are on Irrational Mode

Growth stocks continued to get pummeled and the NASDAQ is almost 10% down on the year, ARKK is down 20%. Nearly an entire year of gains wiped out, leaving only 5% left on the table. With momentum still trending down, a hawkish fed, and a preference for “value stocks” it seems all is lost. It’s getting to a point that it doesn’t matter what you own. This is a massive unwind.

The IWO, Russel Growth ETF, has officially hit another 52 week low today, as well. Heading into tomorrow, we could experience the same thing. Looking at my watch list, it’s pure devastation. It doesn’t matter what valuation the business is, what the business does, or what the future of the business could be. This leads me to the title of this news letter.

Growth Has Become Value

During periods of extreme sentiment, valuations provide investors a rules based approach of reason and rationale. Both in euphoric highs and pessimistic bottoms, it allows us to ask, “how far is it off the mean, or average, of where it wants to be?”

Last year, it was the complete flip of the script when it came to the markets and growth stocks. Valuations got to nose bleed levels and in many cases, some company’s didn’t even have a valuation because they didn’t have earnings, or revenue. Think of how bearish it is today, flip it upside down, that’s how euphoric it was then. When we looked at valuations, we could get a good idea exactly how extreme and high prices where.

Today, we’re going to do the same thing. I’ll run valuation multiples on some of my favorite growth stocks. I’ll do my best not to use price to sales and will use price to gross profit, EV/EBITDA, P/E ratio, or PEG (price to earnings growth). With each, I’ll provide a brief business description and each has a vetted, healthy, balance sheet. The goal of this is to show, whether you own these stocks or not, the valuation multiples of growth stocks as a whole. Expected stocks to cover:

Confluent $CFLT

SentinelOne $S

DigitalOcean $DOCN

Upstart $UPST

Monday $MNDY

Global-E $GLBE

PubMatic $PUBM

MercadoLibre $MELI

DLocal $DLO

Digital Turbine $DLO

All forward valuations will be based on Wall Street consensus as of January 18th, 2022 and is subject to change based on business performance

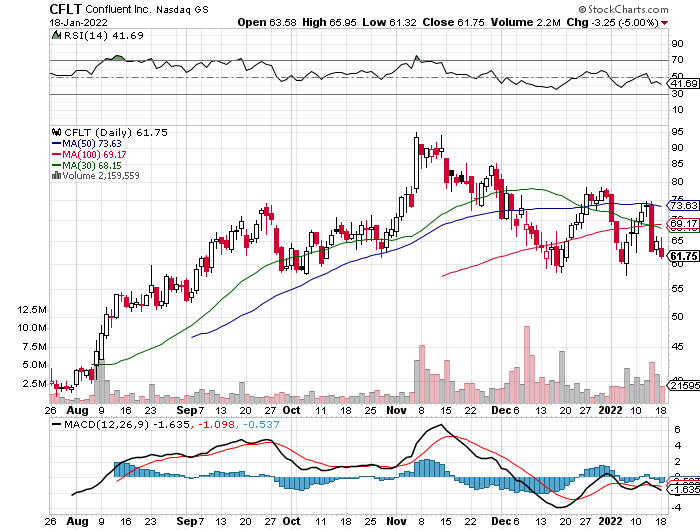

Confluent

Specializing in Apache Kafka and “data in motion”, Confluent runs an infrastructure to manage Apache Kafka for the enterprise. Kafka is a type of code that produces real time data processing rather than running a batch process to extract data. In other words, think of getting a notification on your phone from Facebook Messenger, Email, or Twitter. The push notification is derived from Apache Kafka. You didn’t need to go and submit a query to extract the data. Confluent helps with this, but at an enterprise level. Think of their platform acting like a brain and they manage the central nervous system of an enterprise. If this sounds exciting, it definitely is. They have years, and years, of growth.

Their valuation is one of two software stocks that are trading at high valuations still. I do think it’s currently experiencing a technical break down as the trend is moving bearish. If the market is continuously weak, it could begin to trade down to a good/great valuation.

Expected financial performance:

Full year 2021:

Revenue: $378m (50%+ YoY)

EPS: $-.87

Full year 2022:

Revenue: $519 (37% YoY Growth)

EPS: $-.77

Full year 2023:

Revenue: $700m (35% YoY Growth)

EPS: $-.54

Valuation - Market Cap: $16B with 70% Gross Margins

FY 21: EV/GP (enterprise value to gross profit) 58x

FY 22: EV/GP 42x

FY 23: EV/GP 31x

Summary

I don’t currently own Confluent and I genuinely wouldn’t be surprised if these analyst estimates are sandbagged tremendously. I would think that 50% - 60% growth over the next 3-5 years would be reasonable. But, the returns at this valuations is less than favorable. In one of few instances here, this is a stock I am hoping would go down. I’ll take what I can get at the end of this bear market.

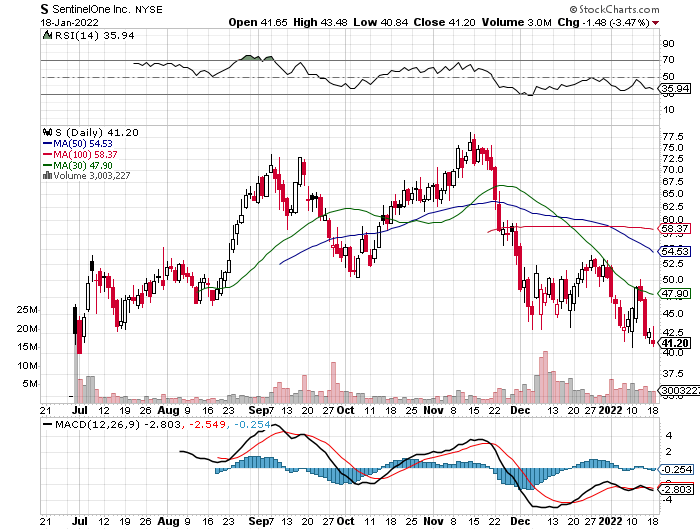

SentinelOne

A cyber security stock and one of the main competitors to Crowdstrike. They specialize in XDR technology which focuses on both the endpoint and the cloud which provides a better detection and response system, according to SentinelOne and Mitre report. This is a natural progression from many other players EDR technology, which is cloud first.

SentinelOne is very capitalized with over $1.5B of cash on the balance sheet and no debt. Their growth is the story that makes me the most excited. More importantly, cyber security is a “need to have” in every organization rather than “nice to have”, the market isn’t going anywhere and enterprises typically seek the “best” infrastructure. SentinelOne is a leading player here and getting better, fast.

Their valuation isn’t cheap but the company is growing well over 100% a year and continues to show acceleration in growth. It wouldn’t be difficult to for-see years of growth 60%+ CAGR while enhancing the bottom line as they scale. They’re expected to be profitable within three years.

Expected financial performance:

Full year 2021:

Revenue: $200m (128% YoY Growth)

EPS: $-.77

Full year 2022:

Revenue: $345m (72% YoY Growth)

EPS: $-.69

Full year 2023:

Revenue: $570m (65% YoY Growth)

EPS: $-.35

Valuation - Market Cap: $16B with 67% Gross Margins (expanding to 70%+)

FY 21: EV/GP 64x

FY 22: EV/GP 33x

FY 23: EV/GP 20x

Summary:

If you look at SentinelOne on a TTM basis, it may never make sense to buy them. But, it’s their growth that’s priced into the stock. In this case, their NTM EV/GP is 33x with expanding underlying metrics. If SentinelOne continues to surprisingly outperform, there is plenty of upside. However, if they don’t and leadership stumbles, it could send their stock price to levels it’ll never get to again.

I have a position and think they’re a multi-bagger in the next 3-5 years. If they perform or outperform, this is a fair valuation with 50% lower growth baked into the price this year. It’s been a gift from the markets this year to push it down this low.

Big risk if they underperform though.

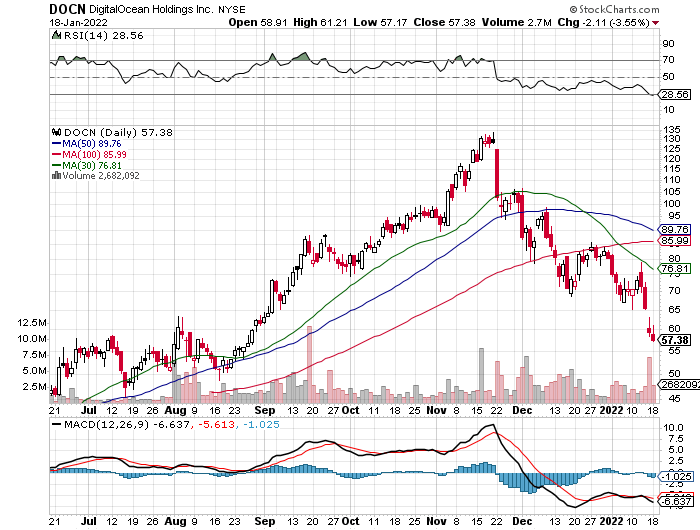

DigitalOcean

Specializing in cloud infrastructure for the SMB market, Digital Ocean is an excellent option for small companies to build their company on top of. AWS, Google, and Microsoft all participate in this space but they all end up being too expensive or offer complicated packages. Where Digital Ocean gains their competitive advantage is obviously, on their performance, but their simple approach to teams that don’t necessarily have the capital to invest like some of the bigger players do. They offer courses, blogs and community’s for developers to work together and learn.

The most important thing to know about Digital Ocean is that they’re very profitable, with accelerated top-line growth and an expected 70% growth in earnings over the coming years.

Expected financial performance:

Full year 2021:

Revenue: $428m (34% YoY Growth)

EPS: $.34

Full year 2022:

Revenue: $562m (31% YoY Growth)

EPS: $.59

Full year 2023:

Revenue: $734m (30% YoY Growth)

EPS: $1.03

Valuation - Market Cap: $6B with 30% EBITDA Margins (expanding to 70%+)

FY 21: EV/EBITDA 47x

FY 22: EV/EBITDA 36x

FY 23: EV/EBITDA 27x

Summary

The exciting thing about DOCN is that it finds itself at a very interesting market niche with market tailwinds at its back. In addition, their infrastructure is very sticky to a lot of different businesses. 30%+ growth over the coming years should be easy to obtain and there’s years where 40% could easily be in the picture. Forward EV/EBITDA of 36x with years of 30%+ revenue growth is more than fair.

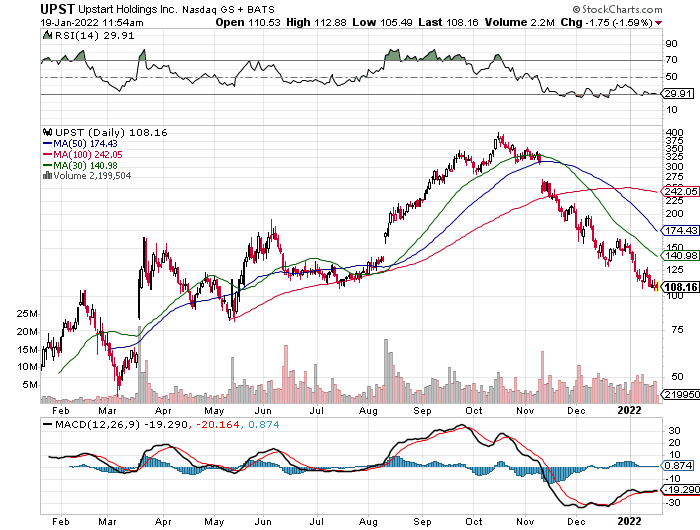

Upstart

Upstart has a complex business model, I’ll let my friend Josh show you his understanding:

Essentially, they’re on the conquest to replace the credit system with their AI. However, they’re still new and with their current business model it’s in this in between stage of proving itself and mass adoption. This is important because that’s the bet here. From a bullish perspective, do you think Artificial Intelligence can replace the credit score system or do you think legacy systems will continue to out perform.

I do believe part of their sell off has been attributed to 2 major factors, on the fundamental side of things: 1.) Expectations became unreasonable and they only moderately beat expectations rather than crush expectations. 2.) Wall Street is concerned how Upstart will perform in a slightly tighter environment when it comes to liquidity. The data trends pointed toward Upstart having a lower default rate over time, especially in 2020. But, liquidity was abundant. It’s at a cross roads where if it can continue to show improvement, based on their AI modeling, it could see a surge of cash flood back into the stock. Not only that but their valuation is more than reasonable here.

Upstart has about a 40% contribution margin. I will use this metric because they operate as a financial institution and EPS can be difficult to judge. They are currently profitable on a GAAP basis.

Expected financial performance:

Full year 2021:

Revenue: $806m (245.6% YoY Growth)

EPS: $1.95 (+745%)

Full year 2022:

Revenue: $1.17B (44% YoY Growth)

EPS: $2.35

Full year 2023:

Revenue: $1.5B (29% YoY Growth)

EPS: $2.83

Valuation - Market Cap: $9B with 40% Contribution Margins

FY 21: P/E 56.3x, P/C.M. (contribution margin) 26x

FY 22: P/E 47x, P/C.M. 18x

FY 23: P/E 39x, P/C.M. 14x

Summary

Upstart grew 245% this year and this is currently being over looked. The “why” behind this is likely rooted in business execution, adoption and acceptance of the idea that Upstart could yield superior yield for investors willing to buy originated loans. Their default rate is the number one thing coming into view for larger investors. They need to see how Upstart will fair in an environment where liquidity is tighter. Then, we’re likely to see upward revision in its forward guidance.

There is a strong scenario where Upstart performs extremely well for years and could grow 50%+ again next year.

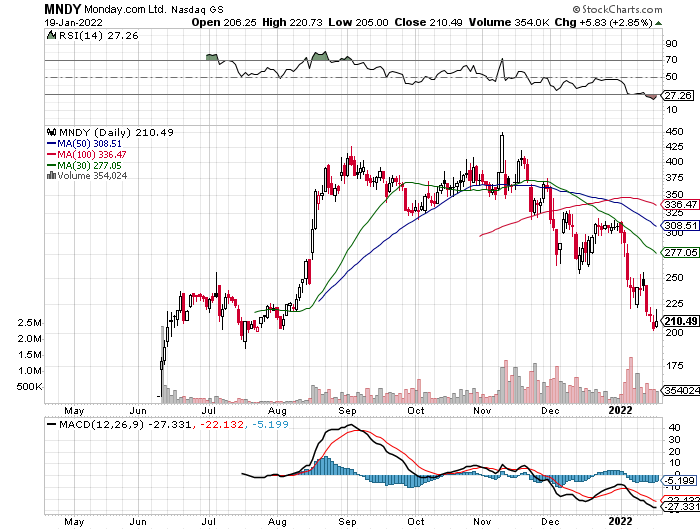

Monday

Monday.com is a collaboration software, much like Asana. However, the uniqueness to their business model that they’ve taken is that it’s highly customizable and is very appealing to non-tech organizations. They call it “low code/no code” programming. What’s most appealing is the long term ability for this to become a “Microsoft Office” type of system where you can create and manage your own infrastructure for many different type of projects. This includes CRM, project management, DevOps, and many more business functions. The customizability and universal applicability is its unique competitive advantage.

The valuation under some context may not make sense if you primarily use it from a price to sales perspective. But, Monday has 90% gross margins, cash flow positive and growing 90%+ YoY. At this rate, there’s a massive TAM with a ton of room to growth.

Expected financial performance:

Full year 2021:

Revenue: $300m ( 90% YoY Growth)

EPS: $-1.64

Full year 2022:

Revenue: $443m (47% YoY Growth)

EPS: $-2.63

Full year 2023:

Revenue: $602m (35% YoY Growth)

EPS: $-1.70

Valuation - Market Cap: $9B with 90% Gross Margins

FY 21: P/GP 33x

FY 22: P/GP 22x

FY 23: P/GP 17x

Summary

Monday’s valuation at first glance doesn’t make much sense but their operating leverage and high gross margins allows them to continue to invest into growth. Because of this, I do think that leadership has the ability and flexibility to continue to grow above analyst expectations for years to come. A forward P/GP of 22x is a “reasonable” valuation for a hyper growth business. It’s still not cheap here. 15x would product excellent alpha.

I do have a position.

Global-E

Enabling cross boarder e-commerce, Global-E is a platform for merchants around the world. When a merchant thinks about selling their products into other countries, there are many complexities from legal barriers to understanding the demographics. Merchants, typically, would have to hire and train an entirely new team in a different country to sell their products. Or, you could just use Global-E’s offering.

The long term bull thesis here is that Global-E is a major play on global trade and closing the gaps to international e-commerce. In addition to facilitating global trade, Global-E is also partially owned by Shopify.

The valuation of Global-E has become phenomenal as of recent, given the sell off. It’s very strange to see sentiment change so much on a stock just based on price action, as nothing has changed about the story of Global-E.

Expected financial performance:

Full year 2021:

Revenue: $240m ( 77% YoY Growth)

EPS: $.11

Full year 2022:

Revenue: $367m (52% YoY Growth)

EPS: $.16

Full year 2023:

Revenue: $562m (53% YoY Growth)

EPS: $.40

Valuation - Market Cap: $5.4B with 40% Gross Margins (expanding with scale)

FY 21: P/S 22x

FY 22: P/S 15x

FY 23: P/S 10x

Summary

With Global-E, I did use P/S because its gross margin is difficult to calculate currently. They have successfully raised Gross Profit over the past 6 or 8 quarters (maybe longer) and has expanded the ability to be profitable as well. In this case, I don’t know what maturity looks like when it comes to margins and they’re on hyper growth so I’ll use P/S to get an idea.

According to analysts, their growth will be 50%+ for the for-seeable future and with a TAM like global commerce and a Shopify partnership in their back pocket, the long term opportunity is incredible. All growth investors should keep this on their radar as it has gotten to “cheap” or discount territory from a P/S perspective.

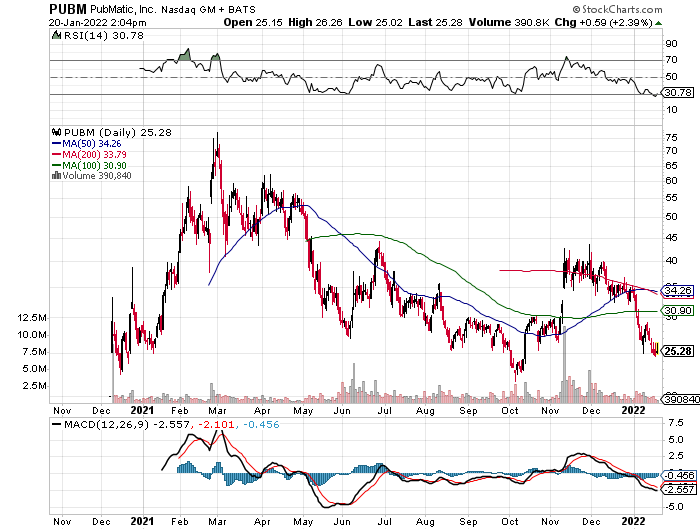

PubMatic

PubMatic is an AdTech SSP, or supply side, business. In AdTech there are two sides, demand side and supply side. A company you may be familiar with is The Trade Desk, who is a demand side AdTech company and not a direct competitor to PubMatic. With Supply side AdTech they typically work directly with companies looking to sell space on their platform for advertisements. Demand side AdTech works directly with the Chief Marketing Officer to a company that’s looking to spend ad-dollars.

PubMatic finds them selves drastically competitively differentiated among its peers due to owning its own cloud infrastructure. By owning their own infrastructure, they create their own flywheel approach and strong competitive advantage. Essentially, this allows them to charge less than their peers (giving them pricing power), operate more profitably, and innovate faster to adjust to the rapidly changing AdTech environment.

PubMatic, I believe, has been caught up in the growth stock crash and small cap destruction since IPO and bubble pop. When the market pays more attention to growth stocks, I anticipate on PubMatic doubling in price from $25/share and going on a long lasting bull run. Their valuation is dirt cheap too.

Expected financial performance:

Full year 2021:

Revenue: $226m ( 56% YoY Growth)

EPS: $.80

Full year 2022:

Revenue: $283.55m (25% YoY Growth)

EPS: $.70

Full year 2023:

Revenue: $350m (23% YoY Growth)

EPS: $.93

Valuation - Market Cap: $1.3B with 30%+ EBITDA margins

FY 21: P/EBITDA 19x

FY 22: P/EBITDA 15x

FY 23: P/EBITDA 12x

Summary

Pubmatic valuation is very cheap and it should be considered by growth stock investors. Their balance sheet is A+ with cash and no debt. In addition, they are cash flow + with future expected earnings. Essentially, they are a very strong company that hasn’t received the respect it deserves, yet. It will be exciting to see if they meet or exceed their 25% growth guidance for 2022.

MercadoLibre

An E-Commerce and digital payments business in Latin America. This proven winner has traded down to pretty crazy valuations. Growth isn’t necessarily supposed to accelerate here, but will likely stay over 30% for years to come. It’s hard to imagine a future where MercadoLibre doesn’t become the dominant player out of LatinAmerica as it takes advantage of two major secular trends.

When it comes to their financial statements and opportunity, it’s their expanding profitability that excites me the most. Their earnings are expected to grow 100%+ over the next few years as they gain operating leverage with scale. In my opinion, this is something you just shouldn’t overthink.

Expected financial performance:

Full year 2021:

Revenue: $7B ( 75% YoY Growth)

EPS: $3.59

Full year 2022:

Revenue: $9.4B (35% YoY Growth)

EPS: $8.41

Full year 2023:

Revenue: $12.65B (35% YoY Growth)

EPS: $17.65

PEG Ratio currently .99, PEG is price to earnings growth

Valuation - Market Cap: $57B with Earnings

FY 21: P/E 295x

FY 22: P/E 126x

FY 23: P/E 60x

Summary

Although from a P/E ratio, it would appear MercadoLibre is overvalued but their earnings growth cannot be ignored. The PEG ratio, which is a good measure for profitable growth stocks, is currently less than 1 showing it is in undervalued territory. PEG ratios greater than 1 could mean the stock is overvalued and PEG ratios under 1 can mean it is undervalued.

This secular compounder has an extremely bright future despite competition concerns with SE. I have a position.

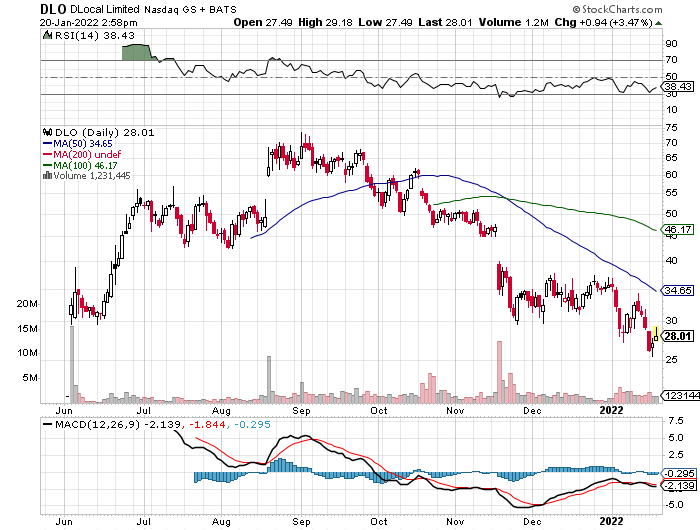

DLocal

My largest position. There are few companies with metrics like this and a future like DLocal. They operate pay-ins and pay-outs within emerging market economies. Essentially, they handle payment processing for some of the worlds largest companies like Microsoft, Amazon and DiDi (the Uber of China). They are the leader in their space, when it comes to emerging markets, and their growth has been nothing short of astronomical.

DLocal doesn’t only come from the growth of their own business and ability to onboard companies. It comes from a merchant’s ability to scale their presence in an emerging market economy. Let’s say Amazon wants to offer its store in an emerging market, they can work with DLocal and DLO benefits from increasing Amazon sales over time.

At first glance, DLO may look expensive but it’s PEG is less than one. Growth is currently at a point where it’s not priced into the stock and growth estimates appear to be conservative. From this price, there’s a ton of upside in the stock price and could double this year if they maintain a similar growth trajectory as before.

Expected financial performance:

Full year 2021:

Revenue: $242m ( 123% YoY Growth)

EPS: $.25

Full year 2022:

Revenue: $403m (67% YoY Growth)

EPS: $.41

Full year 2023:

Revenue: $623m (55% YoY Growth)

EPS: $.67

Valuation - Market Cap: $8B with Earnings

FY 21: P/E 107x

FY 22: P/E 66x

FY 23: P/E 40x

Summary

On a P/E basis DLO makes sense when looking to the future especially since it’s growing so fast. I have noticed that many traders seem to look one year out or twelve months back and say, “that’s the P/E”. But, if they’re in a massive TAM and they’re the market leader within that TAM, it usually indicates that there’s massive opportunity ahead for the business.

If this isn’t priced in this presents massive opportunity for share holders and I believe that’s what we’re witnessing today, massive opportunity for this stock.

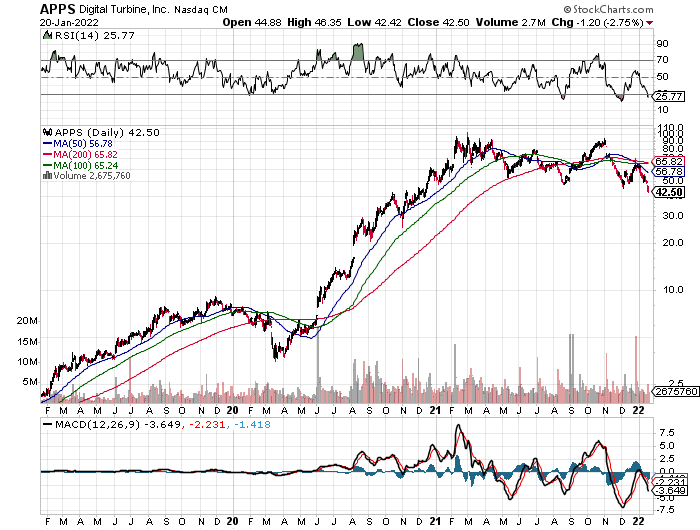

DigitalTurbine

Digital Turbine was originally a software business that could be installed on Android phones. They were growing very nice and profitably. In 2021, they acquired three different AdTech companies to expand their portfolio of products. Fyber, Adcolony and Appreciate are all advertising businesses. These additions work extremely well for the organic DT model.

Originally, DT was used as a on device software that installed applications and could automatically pre-install apps on new phones. Once they added their AdTech businesses, they became more of a complete solution for their business partners. The bull thesis behind digital turbine is that they can operate on any device these days as long as it requires apps to be installed or advertising.

There are few stocks in the market that can combine both growth and value. Digital Turbine is one of them. Their financial performance so far and their expected performance in the future is nothing short of incredible.

Expected financial performance:

Full year 2021:

Revenue: $1.21B ( 285% YoY Growth)

EPS: $1.65

Full year 2022:

Revenue: $1.6B (31% YoY Growth)

EPS: $2.16

Full year 2023:

Revenue: $2.16B (36% YoY Growth)

EPS: $3.31

Valuation - Market Cap: $4.5B with Earnings

FY 21: P/E 27x

FY 22: P/E 20x

FY 23: P/E 13x

Summary

Digital Turbine presents one of the most compelling opportunities in the market.

It is the definition of a value stock as it generates income and cash flow. In addition it offers long term growth prospects and upside that may not be baked into the price. Investors should consider looking into this more.

Conclusion

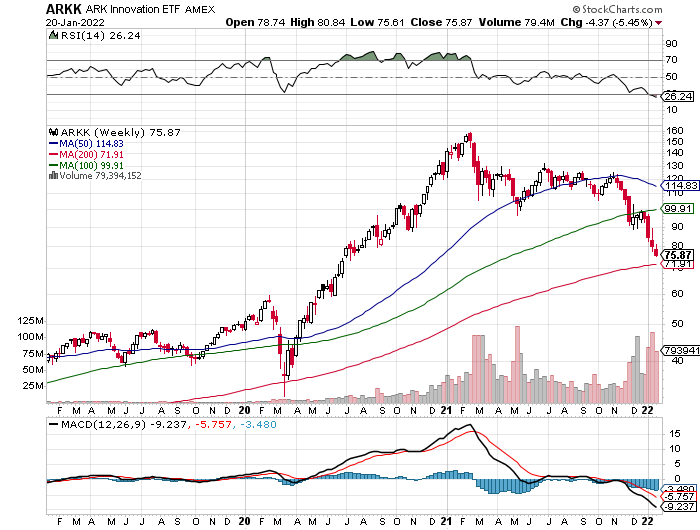

The 200 week moving average provided a lot of support for ARKK during the COVID crisis. I anticipate it will do the same again which would mean we’re at or near the bottom for many growth stocks.

If the indices continue to break, it seems like there would be weakness. But, it was Bifurcated all year last year. Why wouldn’t it be bifurcated now till this market cycle is complete?

There are opportunities every where for the patient investor

If you liked today’s content and found it valuable, please consider subscribing. Thank you for taking the time to read today’s letter and I can’t wait to write for you guys again soon.

Stay Tuned, Stay Classy,

Dillon

Such a valuable write-up !

Didn't know $GLBE trades at only 16.88X next year's sales... Adding!