Hear Me Out

Hear Me Out

Everything is terrible right now from Fx, to the Fed. But, is it really that bad?

Today, Thursday September 22, 2022, I bought the most stock I have all year.

I believe it’s safe to say that I am in the minority so it goes without saying here that I don’t expect anyone to “believe” my thesis. The purpose of today’s memo is to, more or less, hear me out and see the lessons of history I am looking at to develop my thoughts about the future. There’s a lot more to be bullish about than bearish about, for the patient investor, today.

My thesis is derived from the concept of a “nail in the coffin” central banking approach to inflation, as well as a peak in the current market cycle. This peak would signal a major low in the equity markets and bond markets.

Let Me Debunk a Bear Argument, First, Before I Share My Thoughts

“The Fed needs to ease for the markets to go up.” This is NOT true. We don’t need to go back too far to debunk this thesis.

In those scenario’s the Fed pivoted when Corporate earnings and the economic picture became shakey.

My thesis is not based on the Fed cutting rates to zero, but rather, markets getting used to a “new normal” with an era of higher interest rates. I believe investors, and market participants, somehow believe that we need to be at 0% interest rates for the market to go up. This psychology has likely developed from the past 13 years post GFC.

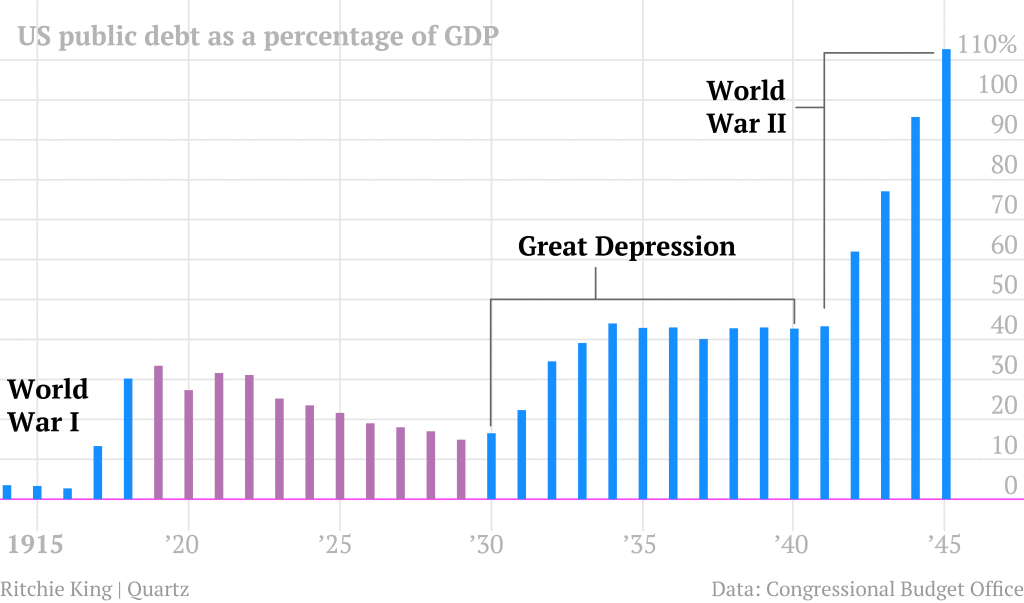

After World War II (1945), We Entered a Period of Higher Interest Rates, Higher Inflation and a Secular Bull Market Still Took Place Till 1969

In many ways, our economy today looks like that of the recovery period following the stock market crash of 1929 - 1932 and the return from WWII. We had a prolonged period of deflation after a major credit super cycle in 1929, which is similar to 2008. The difference between now and then is that the Federal Reserve, today, did accommodative monetary policy to prop up the economy.

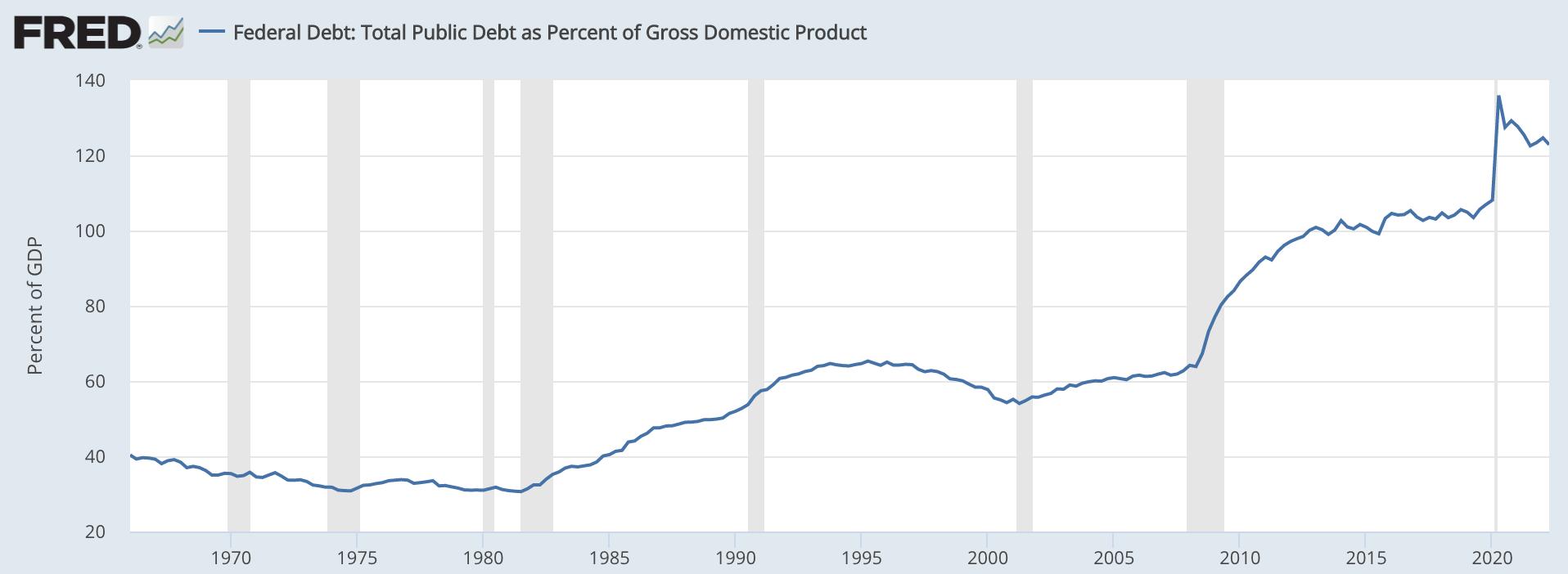

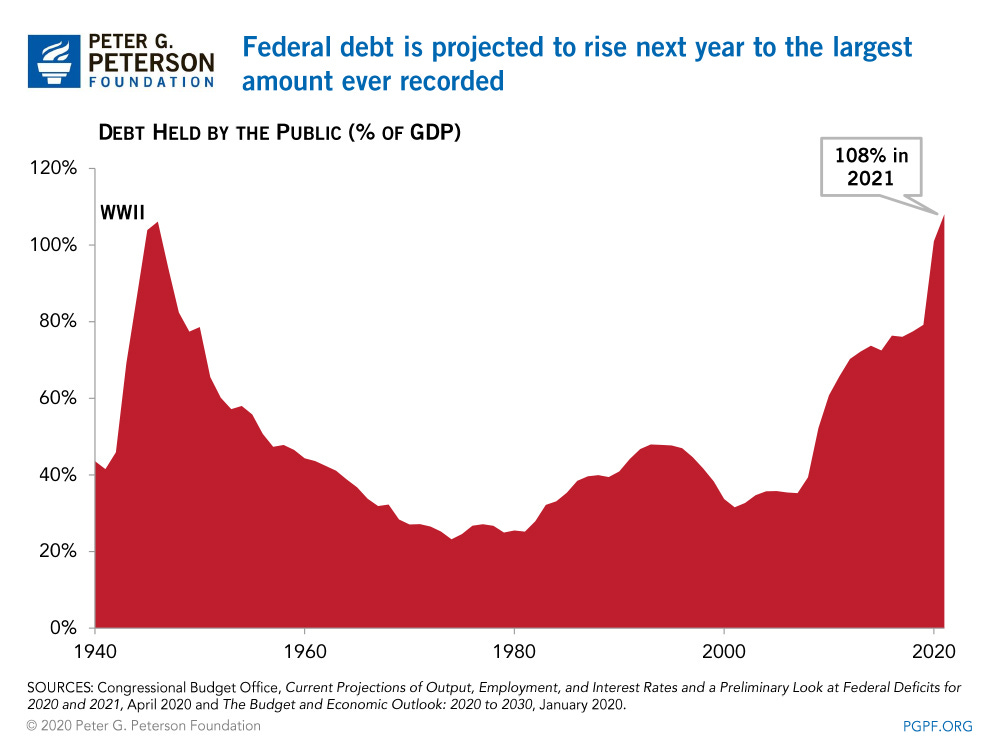

The most important similarity, however, to take from this period, was the U.S. Government Debt as a % of GDP following World War II. It is similar to the debt levels of the U.S. today following the COVID response.

If we take Milton Friedman’s economic/inflation philosophy of; “Inflation is always and everywhere a monetary phenomenon, in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.” We can deduce that inflation is predominately caused by too much government spending in a rapid way. I.E. the U.S. spending trillions of dollars in response to COVID pandemic.

WWII Debt % to GDP

Today’s Debt % to GDP

World War II is not only similar to the U.S. Governments spending response to the crisis over sea’s but also, the “re-opening” when soldiers came back from the War.

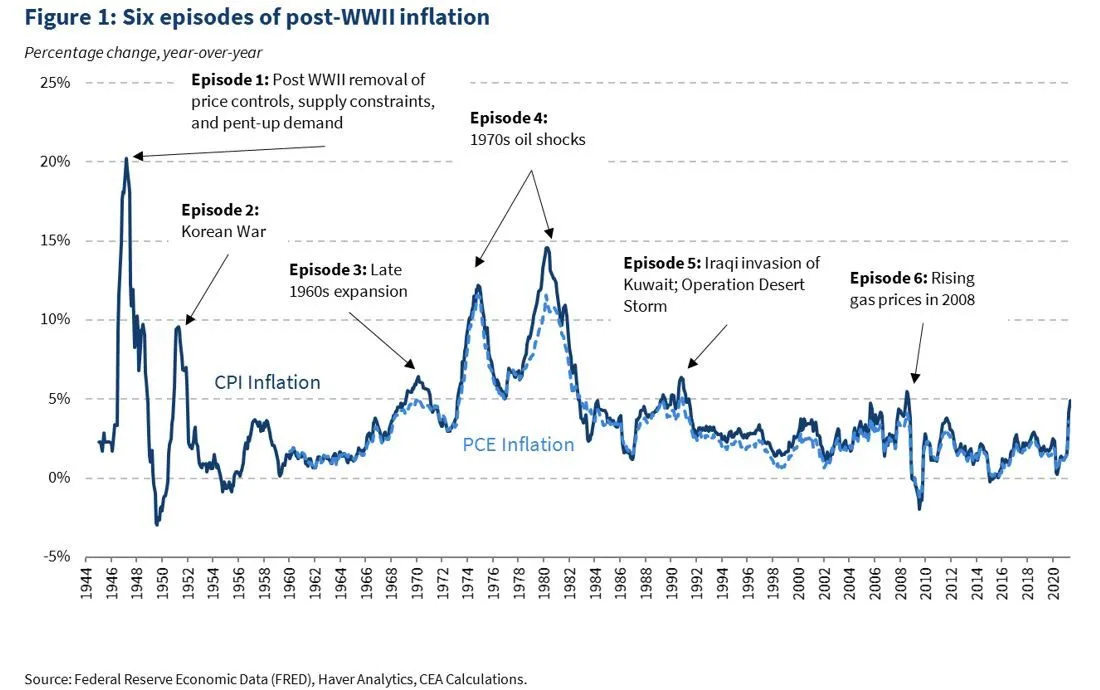

Knowing this data set is important for the reader to understand my thesis because the 1970’s is, for some reason, the only inflationary period referenced in today’s market. The 1940’s is similar to today because of the short term “shock” and “response” of monetary and fiscal policy. The 1970’s was much more hallmarked as the period of “guns and butter” economic philosophy, Vietnam era spending and the oil shocks of the 1970’s.

Yes, we have Russia/Ukraine energy issues now but American’s are not standing in line waiting for their gas rations on any given day. It was a different type of “oil shock”.

My Thesis is Based on Two Factors: 1.) Jerome Powell Will Crush Inflation & 2.) The Economy is Strong Enough, Finally, to Handle Higher Rates

Both factors will be important to hear out to fully grasp as to why I am still bullish.

As Much as I Hate it, Jerome Powell is Doing the Right Thing

My friend Josh did an excellent job explaining what Jerome Powell is doing.

After you have read Josh’s thread, let me build on top of what’s happening here.

Narrative is a strange thing and so is herd mentality. I quickly picked up that every time I opened Twitter spaces it was nearly always an echo chamber of, “the Fed is behind the curve, they have no credibility” etc. Now, since the last meeting on Wednesday, I received 3-4 different newsletters essentially covering the same material and Twitter is chiming in, “we are going to a recession, brace for impact!”

Consensus is not always wrong, they could be right. We could absolutely be going into a more severe recession (more on that in the economy portion of my thesis). What I find unusual is that now, after inflation appears to be genuinely peaking, the market NOW believes them? This seemed incredibly strange to me but what they, the Fed, are doing is blatantly obvious.

The Federal Reserve is “Putting the Nail in the Coffin on Inflation Expectations”

The Fed, Jerome Powell and friends, clearly see that inflation is actually peaking. From their latest meeting, they came out with some of the most aggressive forward guidance and dot plots on their “Summary of Economic Projections” (SEP). If you’re not familiar with the SEP and not sure how to read the data, YouTuber “Meet Kevin” does a wonderful job explaining the data here:

To summarize what he mentioned:

The Fed guided for rate hikes of 4.6%, which could lead to 5% rates by end of 2023.

They are basically saying the economy is in trouble in the SEP with lower than expected (revised down) GDP growth for 2022.

They mentioned multiple times that employment needs to come down and unemployment needs to rise. In other words, pain.

One important part from Josh’s Twitter thread was found here:

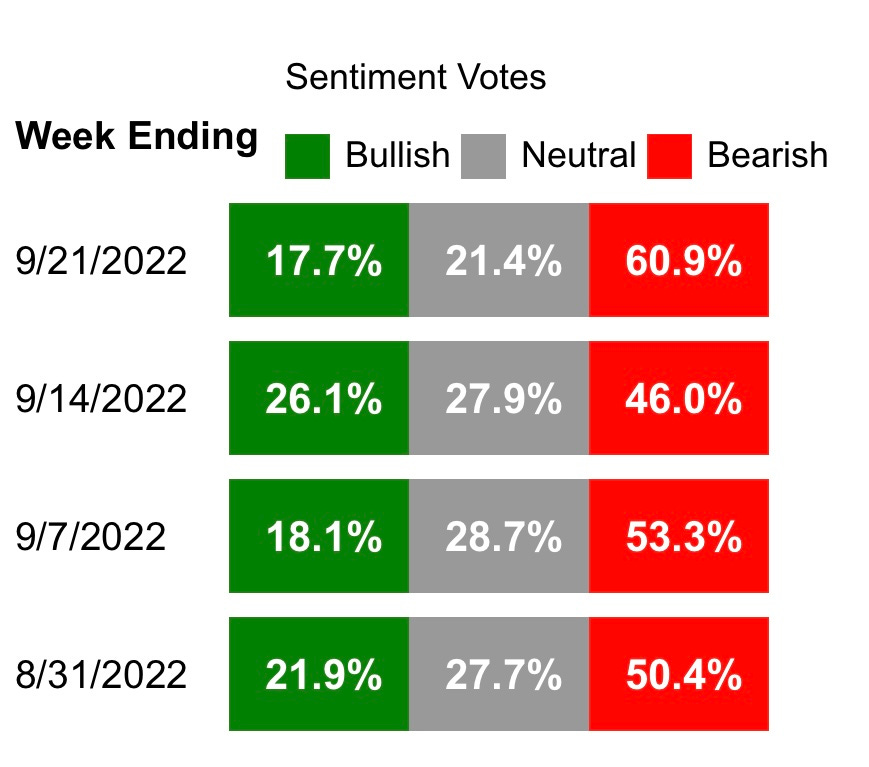

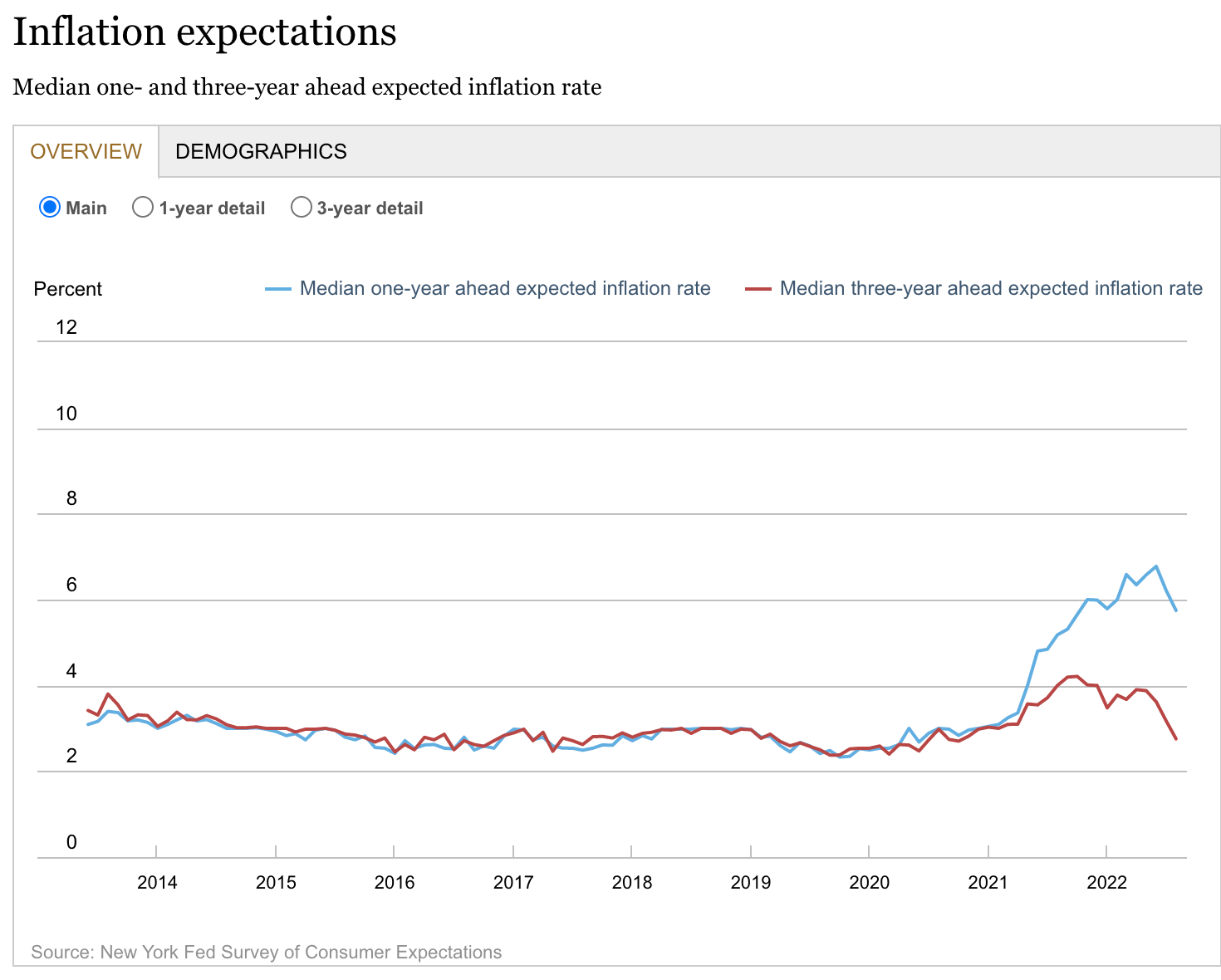

Paul Volker knew that in order to combat inflation, after many failed attempts, he did not have to structurally change the economy. The Federal Reserve Theory about inflation that came from the 1970’s is that you NEED TO BREAK THE BACK OF INFLATION EXPECTATIONS. Guess what, it’s working. Data below taken from the New York Fed.

1 Year and 3 Year Inflation Expectations

Gas, Good and Rent Inflation Expectations

The Federal Reserve Knew They Needed to Come Out Ultra Hawkish Here to Finally Kill Inflation Expectations Once and For All

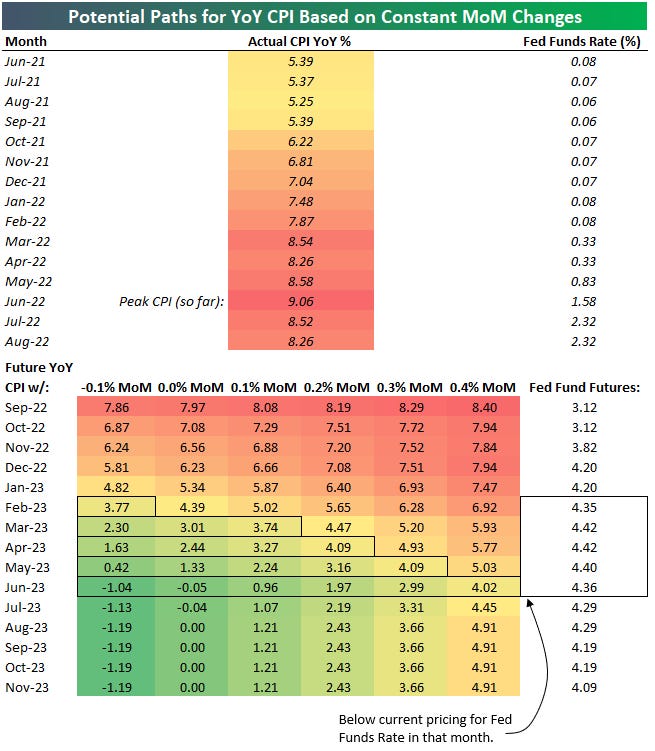

Remember, I mentioned above that they came out projecting 4.6% on the Federal Funds rate. Below, we can see the projected path of CPI. Let me explain why this is important.

The second part of managing inflation, aside from inflation expectations, is to raise rates to “restrictive”. Paul Volker raised rates aggressively higher to be higher than the YoY CPI change in the 1980’s and kept them there. The idea is that this is “restrictive’ on a real basis. In economics, you usually hear “nominal” and “real” when thinking about inflation adjusted or non inflation adjusted yields.

On a real basis in this case is when the Federal Funds rate is higher than the annual change of CPI. In the chart above, you can see that May/June is currently expected to be the zone where we will reach “real” restrictive monetary policy.

To simplify what I am trying to say, Jerome Powell is doing a good job and he is doing what he needs to do to jaw bone the markets into thinking he is going to crush the economy to control inflation. In many ways, I think he is crazy but that’s exactly what he wants us to think. He needs the markets to believe that he is the second coming of Paul Volker so that he can control inflation, bring it down, and bring back stable prices. This is why I am bullish.

If inflation comes down, truly, in the coming months, the markets will rally. But all time highs are not in the books till we are convinced inflation is coming down.

The Final Piece to This Puzzle is the Economy, Can it Handle Higher Rates?

As mentioned above, the idea that the Fed “needs” to be accommodative for the markets to go up is just not true. My impression is that many who think this have only looked at Fed/Market history since 2020 when QE-Infinity took place and have only experienced a massive (Fed induced) boom and bust cycle. The truth is that as long as corporate earnings continue to grow, the markets will continue to improve.

But How is it Possible for the Economy to Improve (or Hold Up) During this Hiking Cycle?!

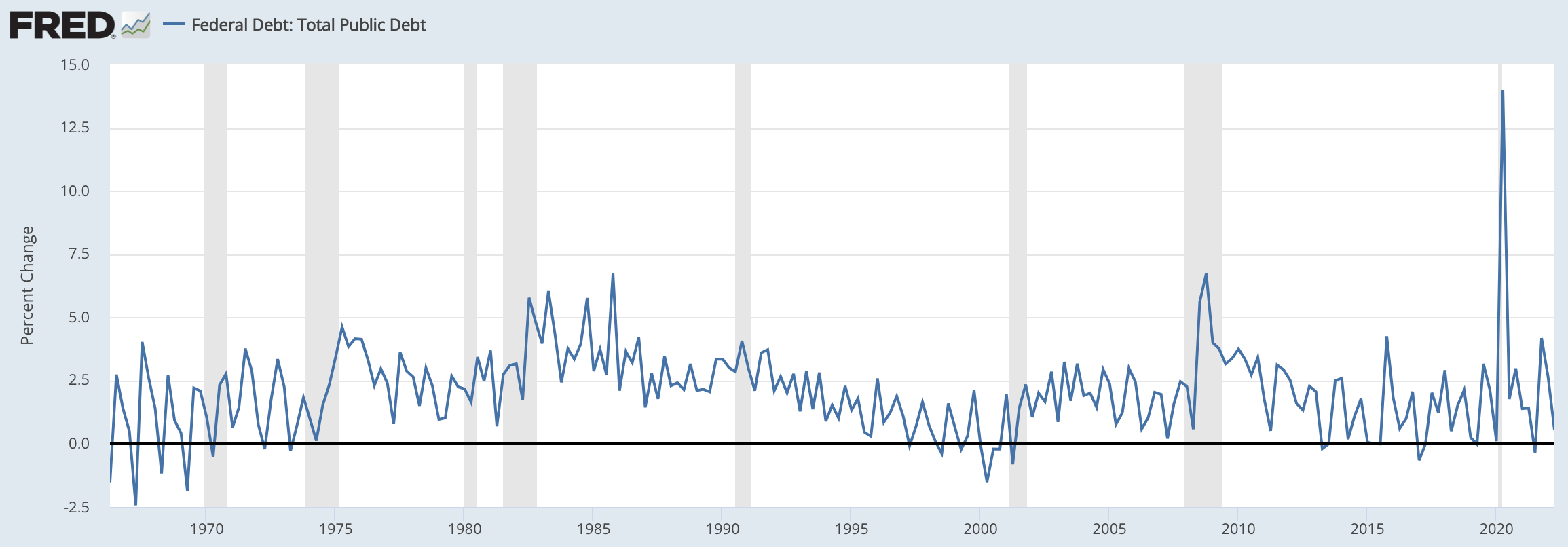

The single most important data point I RELIGIOUSLY see the narrative overlook is just how MASSIVE the Monetary and Fiscal response was to COVID. There are a few charts to show this point.

The reason why this is important is that U.S. Government Debt (not an increase in bank reserves, or QE) is injectable, real U.S. Dollars, that are inflationary because it’s usable money that’s created out of thin air and pumped into an economy. In the future, I will write a SubStack about the difference between banking liquidity (QE) and real money creation as well as the effects each have on the markets and economic growth.

Most investors just say “liquidity”, “QE”, “QT” without understanding what’s actually happening within the banking system.

Fiscal and Monetary Stimulus has a Lagging Effect to it

The rule of thumb, and understanding, is that the economy is a very large machine. When the Federal Reserve, or U.S. Government, makes a change in policy it takes time for the full effects to effectively take place. Think of it like a wave that sweeps through the economy.

Our economic system was flooded with excess liquidity and there is no other period in history where we saw such an aggressive monetary/fiscal response followed by an aggressive tightening cycle.

There is a huge argument to be made that we still have abundant stimulus and lagging effects from the recent, historic, accommodative period. A few examples I can think of:

In the U.S. Housing market, sales are down 20%+ YoY but prices are still rising. I can’t help but believe home owners are reluctant to sell their homes because they have a 2.5%, or 3%, 30 year fixed on their current mortgage. Why would they change homes now while prices are high?

Americans purchased cars at record levels during 2020 because the cost to borrow was so low. I could imagine that Americans don’t necessarily need to buy a new car, today.

Lingering wealth effect is still very real. Asset prices are still higher than COVID lows and many house hold balance sheets are above historical averages. The consumer, in this case, is still strong.

Unemployment is still very low. During COVID, I have a thesis that the de-globalization of the U.S. economy brought jobs back home, suspended legal immigration (legal immigrants have work visa’s that can be eligible for W-2 work) due to covid concerns. Couple the de-globalization with the mass retirement from many older working Americans and I think we have created a structural (not cyclical) labor force shortage.

There are many factors that we could think of and this is just a portion of examples. More or less, the point I am trying to make is that stimulus is likely still in the system at historic levels which can structurally create an economy that can handle higher interest rates.

There Has Never Been a Time in History Where We Have Seen Stimulus to the Extent We Did, Followed by a Rapid Tightening Cycle

We are making and writing history today, which makes this so difficult for investors to navigate. It is confusing to see economic data still come in strong with rates as high as they are. The only thing that makes sense is that the lingering effects of fiscal stimulus have created a structural change in the economy. More or less, we don’t know what the economy will do because we don’t have a play book to look at.

There is a scenario where the economy proves resilient while inflation comes down from the shock of COVID, as long as inflation expectations are controlled.

In Summary, Why Did I Double Down Today?

My conviction lies with the future not being as terrible as investors may think. Today, investors believe that a repeat of 2008 will happen before it’s even happening. Or, comparisons to 2000 bubble burst is a common narrative as well. But here’s the thing, this is not 2000 or 2008, this is 2022. Our bear market is unique which means a unique outcome.

The real danger lies in aligning your thesis with the majority of investors who believe they know the future, with certainty, to an unknown future.

Also, technicals justify and favor a meaningful bounce. If I am right and institutional investors agree/see the same thing, this will be the major low for the foreseeable future.

Stay Tuned, Stay Classy

Dillon

Thank you, Dillon, for another great article.

It is remarkable how quickly you post such a well written and detailed article. You are helping me a lot not to be too afraid of the next weeks and months.

The points you make are very coherent, yet I worry that the Fed is once again pivoting way too late and the economy is struggling with recession while the reactive Jerome Powell is once again taking forever to cut rates to get the economy going again and the recession we are currently in is taking longer than expected.

Either way thank you for this great output.

Appreciate how adamantly bullish you are without mentioning any hedging in such a market environment. I applaud your bravery 🫡. As you know, I’m opposite your thesis and have been on the right side of the trade for awhile now. Long-term (5-10 years) out, these prices could be good since market is bull biased long term.

Sentiment has been bearish biased for 40+ weeks, you’re fighting this and buying to be a contrarian is not actually a good reason to buy. 2020-2021 bull market if you were contrarian bear you’d be dead. Sentiment was overwhelming bullish and stayed bulllish for awhile during 2020-2021. Overbought conditions stayed overbought for a one time. Because liquidity, balance sheet, to fiscal policy all supported inflating asset prices and growing aggregate demand. Now it’s mostly the opposite.

The previous periods where the Fed hikes and stocks rise were periods of strong economic growth and none of those years had the same global macro backdrop and risks. They are not comparable periods. If you are bullish then share were you think we are seeing economic growth? Most earnings have peaked and many companies are slowing down against crazy 2020-2021 post covid comps. There’s a lot of data saying high economic growth is behind us and slower growth is here.

This market will need a lot more time than a few months to adjust to this “new normal” you talk about. We had decades low interest rates, markets don’t adjust in just a few months. The rate hikes started in March 2022. Cheap money was trying to find returns anywhere you parked money, I think you are severely underestimating what higher rates for longer means from a macro economic impact longer term into 2023, the market is pricing this into the future. Why do you think the yield curve inversion is widening and staying elevated. You’re not only fighting the Fed but the bond market! You are BRAVE as hell!!

I had a substack post that dissected Inflation Expectations. I agree that Powell is doing the right thing and trying to break inflation expectations, but from a macro economic analysis, lower inflation expectations means lower aggregate demand and lower growth. That needs to get priced in first before we then recover from how much aggregate demand adjusts and falls because inflation expectations are falling (again, a good thing like you said). But in order to break inflation expectations that remain anchored, Powell has to keep financial conditions restrictive “until the job is done.” Restrictive financial conditions = restrictive to demand and growth.

We are ALREADY in a recession like right now. Check on this message in a few months, you’re not looking at the datapoints close enough. The market is pricing in significant recession risks and I argue the bond market to eventually equities market once we reach below SPY 350 are pricing in recession. Need to let it all price in before I start nibbling and buying long on my favorite companies. Market leaders like CELH, ENPH, FSLR, COST are all pulling back, I believe you are buying too early but that’s what I think.

You mention Paul Volcker and he caused 2 recessions because he let the market determine the rates while he targeted the balance sheet. So I dont know how you are using Volcker and say bullish? Until he achieved price stability we went from the Great Inflation to the Great Moderation and that was one insane of a bull market.

The markets could rally but most rallies will be bear rallies. Inflation is structural and cyclical where the structural aspects will take longer to bring down, it will stay elevated still. We’re in an inflationary period and do not know yet the extent of the monetary policy impact to the economy--like I said you are brave to be bullish in the middle of all this uncertainty. I like to hedge uncertainty until things become clearer in the data and earnings.

Regarding liquidity and QT, net liquidity is being removed from the system. Bank balances and reserves are dropping, reverse repo is increasing (which sucks liquidity out of the system), and the balance sheet is being reduced (last week was -$16.7B reduction). You even said it yourself it takes time for the full effects to take place. I shared in an article that it can be up to 18 months. We just started hiking rates in March 2022 and QT acceleration is barely started this month (Sept 2022). I think you’re jumping the gun early here.

You might have a point that we still have remaining stimulus and wealth effects to continue given the strength of the US consumer, so that’s something I’ll have to look closer at but the data is pointing at a decrease and some earnings reflect that (some companies like Lululemon are exceptions hehe).

Btw Dillon unemployment is still very low and like Powell said, the labor market is “out of balance”. However, the trend now is that unemployment is rising due to labor participation, etc. What happens if we rise to 4%+? Wouldn’t you want to wait until unemployment stabilizes and stops rising? We normally bottom once that is the case, it’s one of the best indicators of a healthy, growing or stabilizing economy.

Anyway, good luck as I like bull markets over bear markets due to the real pain of bear markets. I applaud you for being bullish, it’s brave when a lot of people are just not and you make some good points that I believe is too early, so I would say in 6 months to a year or so when sentiment is way more fearful where we have capitulation and just despair, would be time to buy and load up. So I’m with you there but difference timing.