Let's Zoom Out and Look Forward

Let's Zoom Out and Look Forward

The Markets are Turbulent and Investors are Panicking. What's the Strategy and on "What's Next"?

I want to make sure I publish this prior to tomorrow’s Fed meeting because I believe that catalyst will potentially change the direction of the markets in the near term. There’s been a lot of selling and “de-risking” ahead of the Fed’s monetary policy decision for 2022.

For followers of the BluSuit Substack, we often look to the Fed to get an understanding and guidance of “what comes next” for the broader markets as a whole. Although I do take more of an investing approach, focused on the secular trends that may only be disturbed through market cycles, I do believe that understanding when/how a secular bear begins is crucial to protecting risk/downside. This is based off the philosophy that markets are predominately driven by two things: 1.) Earnings and earnings growth/contraction, 2.) Liquidity fueled by the Fed. Obviously debt, speculation and international conflict may influence markets but you can always bring it back to how that impacts future corporate earnings.

Focusing on liquidity and future earnings has led me to make the best judgement/positioning for 2022, knowing returns may be reduced but it shouldn’t collapse into a secular Bear Market. In other words, expectations should be tempered and should be thought of as accumulation period for assets until the Fed fuels a new round of stimulus for the broader markets as a whole. Trust me, they will, they don’t have a choice.

Previous sources to reference:

Snippet from the linked portion above

Thesis:

Growth stocks and long duration assets are likely to out-perform next year due to overly bearish speculation of monetary policy and general fear of “what comes next”. The secular trends of growth in leading industries remain in tact and so do the macro tail winds, leading me to believe this has been a massive overreaction that may result in a market reversal contrary to popular held belief.

On a side note, for those wondering how my COVID journey is going; it was rough for a few days but I’ve began feeling better. I do know this lingers for awhile and plan on slowing down in the short term to get back to 100%. This community’s support has been incredible and I am thankful for all of you.

What the Markets are Telling us and Why We are Selling

The reason for this market crash is best described in the original publication I wrote “The Coming Market Crash” but, to simplify, it’s due to a contraction of liquidity while the Fed tapers. However, the severity of this correction/crash has not been the result of taper alone. In this particular instance, it’s directly related to what the market expects in the future.

Based on the latest inflation data, the market is completely shifting away from “inflation is transitory” and knows that the Fed is going to need to intervene to kill inflation. The way the Fed stops inflation is by raising the Federal Funds rate, which creates a credit contraction and eventual economic slow down. In other words, the best way to kill inflation is by creating deflationary pressures.

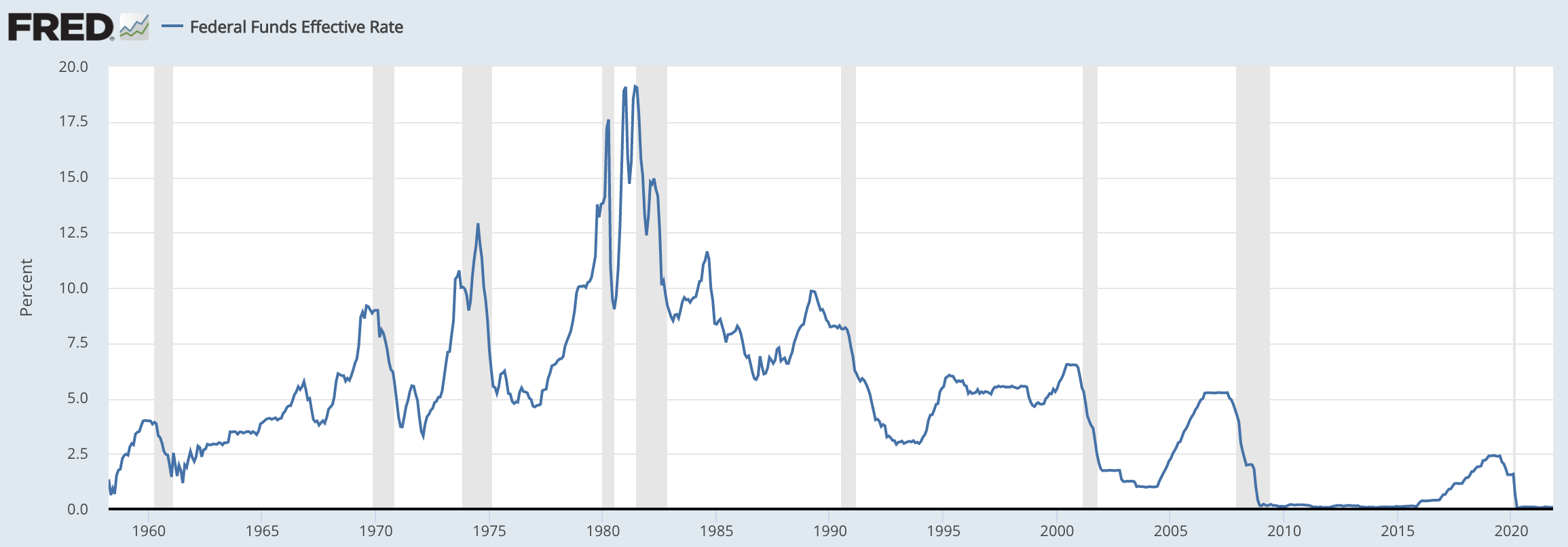

Above, you can see a historical reference of the federal funds rate since the 1950’s. This graph tells a bigger story than what originally meets the eye. Essentially, what you see is that an economic recession (the grey areas) is almost always induced when the federal funds rate got too high. These recessions are almost always counteracted with an instant slash in rates and as of this latest recession, reduced straight back down to 0.

What you can quickly notice is that each time the Federal Reserve slashed rates, it was dropped lower than the previous cycle. This is important to keep in mind as I progress in the conclusion I’ve made about where we are going.

Essentially the markets are front running and, dang near, panicking about the future. This has created an extreme “risk-off” environment to a point that anything with growth priced into it is selling off, it doesn’t matter about profitability, opportunity or underlying business fundamentals. Fund managers are moving all money away from anything with risk and pouring into the most stable companies and other risk-off assets.

This mentality explains the EXTREME bifurcation in the markets that we haven’t seen since the 1999’ tech bust. I think this is a similar situation, but not identical.

In my opinion, this is an overreaction and I think the markets are destined to reverse in the near/intermediate term.

In the above graph showing the difference in valuations, specifically forward P/E, between large cap and small caps, you can come to a conclusion that it’s almost inevitable that the two markets will collide/normalize. Small caps typically underperform in risk-off environments while over perform in risk-on environments. I am led to believe that many economic and monetary policy uncertainty’s have many institutions positioned defensively.

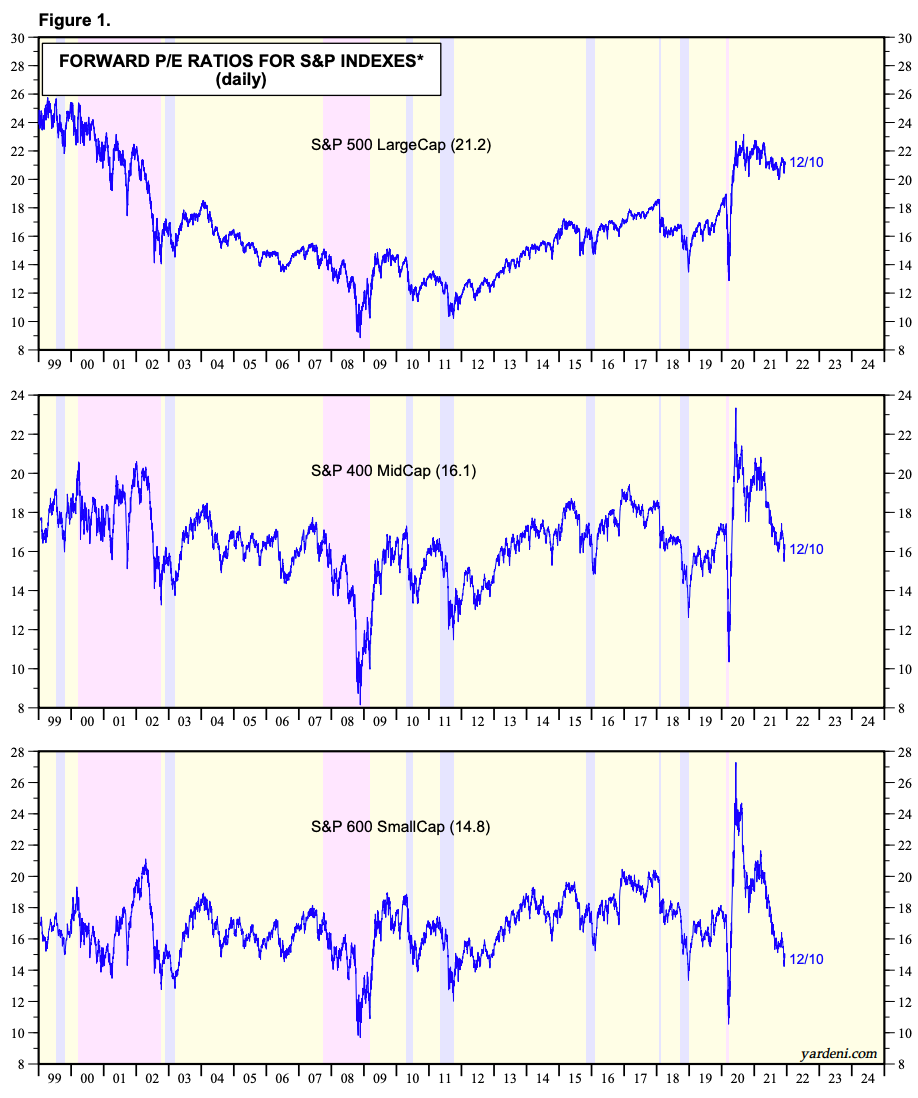

It is also important to be aware of how low the valuations have gotten for small caps which now exceed 2015 market lows and is nearly at the 2018 market bottom.

Either large caps are coming down or small caps come up. The likely scenario would be that they meet somewhere in the middle in 2022.

What The Bond Market is Telling Us

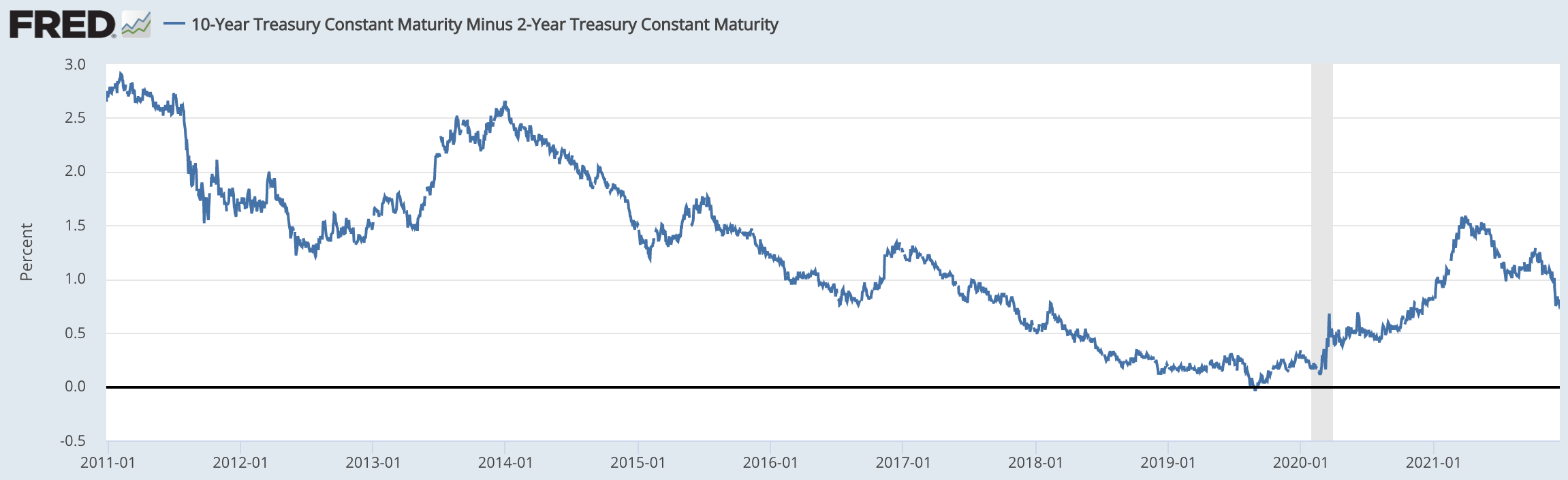

This is the most unusual part of this whole ordeal because the bond market is telling us a different story/narrative than the stock market. This is best observed in the flattening yield curves between the 30 and 5 year bond.

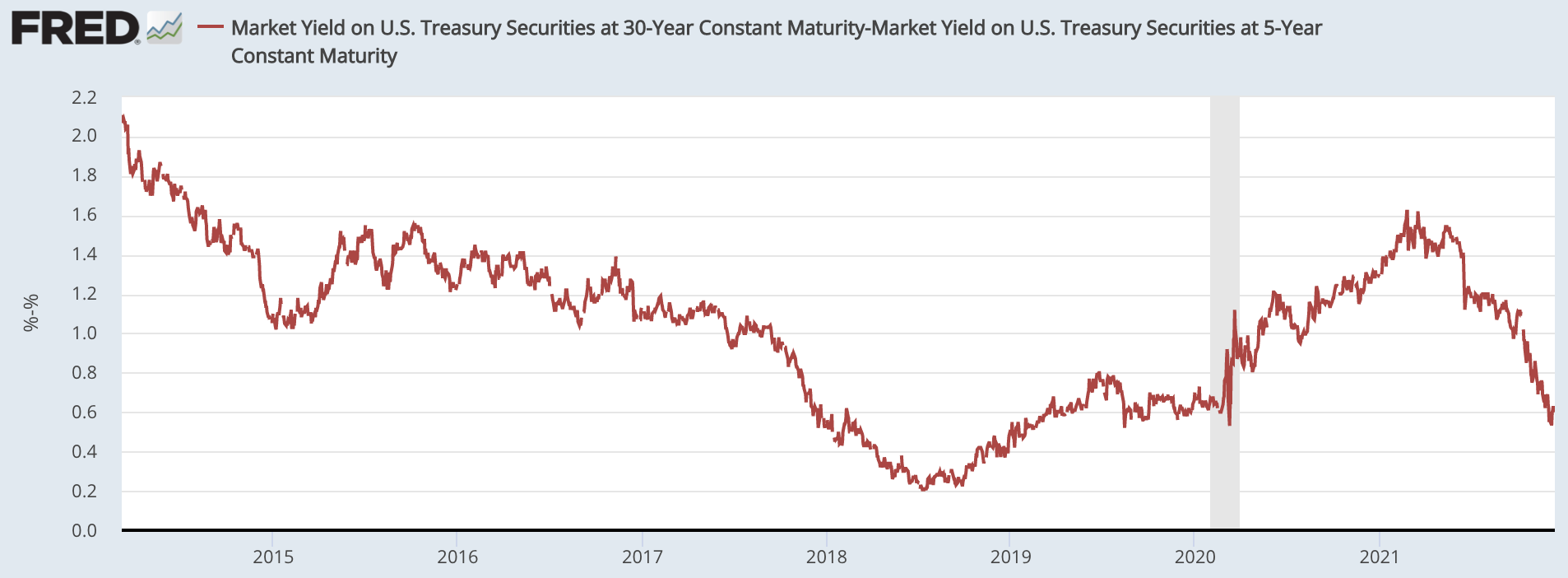

The 30 year bond has remained relatively unchanged, signaling that long term rates are likely to stay very, very low but the 5 year appears to be showing that we could be heading toward an economic slow down and/or short-term hawkish Fed policy. The story is the same with the 10 year over 2 year spread. You notice the 2 year yield has rallied upward since early 2021 while the 10 year has remained relatively flat.

Basically, the Bond Market possibly saw rate hikes and possibly QE taper months before the Fed announced it in early 2021. Now they appear to be pricing in something else, which would be likely be lower than anticipated rate hikes and potential QE in the not so distant future.

Is QEternity hard to believe? Above I mentioned that each time we entered a recession the Fed has previously slashed rated. Now, we have a problem. Rates are currently and will stay near zero. How can the Fed slash rates even further if that’s what they’ve always done before?

If you guessed further QE and creating more inflation, that is beginning to look like the likely scenario. The only way to slash rates is by reducing the “real return” interest rates which essentially make debt so cheap, you’re forced to put your money into other assets. In this particular case, creating a massive secular tailwind for growth stocks.

It appears very likely that the Fed can’t/wont aggressively raise the federal funds rate past even 1%. Keep in mind the U.S. Government Debt just exceeded $29T, they can’t afford higher rates either.

My Personal Strategy Moving Forward

Full disclaimer, I am not a financial advisor and these publications are designed to provoke thought and debate among the investment community. It wouldn’t be wise to make short term moves based on macro trends either, these are much bigger moves and take time to develop.

Looking forward to 2022, I wouldn’t be surprised in the least bit to see a flip in market sentiment toward growth and small caps. The only reason I say this; is that is NOT what’s currently being priced into the markets today. Markets historically reward sectors that haven’t had best case scenario priced in. Remember how value/travel was left for dead this time last year?

I think it would be likely to see the index’s struggle next year, but many stock pickers portfolios (including $ARKK) outperform the S&P 500. The reason why I say this is that many money managers have fled to the S&P 500, cyclicals and FAANGM for safety. It wouldn’t be surprising to see money begin flowing to new, profitable, opportunities as many of these businesses are likely to continue to perform very well. Their earnings will inevitably continue to impress.

In Summary

All long term trends that support a case for secular growth stocks to outperform the markets long term are intact. The Bond Market is not signally a substantial move in the Federal Funds rate which leads me to believe that we wont see significant rate hikes for 2022 and even if they do raise rates, I think it will take effort to get over 1%. If they do go over 1%, I wouldn’t be surprised to see them quickly shift their policy to more dovish especially when they begin to witness further economic slow down.

Based on these factors, I will continue to take my “recently” underperforming investment strategy and double down. Growth stocks are unlikely to be out of long term favor. Currently, the market is likely over reacting and we could see a quick reversal in this sentiment within the next few months. Let me emphasize sentiment here, because that’s why the markets are selling off. Why would a bear market happen now, breaking the rules of history, when rates are at/near zero? History suggests we need lift off first and multiple quarters of it.

I’ll keep all you updated on BluSuit’s research findings and once again, thank you so much for the support. This is a special place and an excellent community. Also, if you haven’t seen the Discord group yet:

If you’d like access but any links aren’t working just shoot me an email or comment here.

You guys are appreciated, stay tuned,

AAAAANNNNDDDD AS ALWAYS, Stay classy,

Dillon

<applause> Well done, Sir. Way to step back and open up the perspective. There's no doubt we will see accelerating tapering and most likely some hikes in 2022. But we don't know, and the selloff is only based on future expectations. Do promising growth companies with strong balance sheets, innovative business models just melt down and vanish during normal economic cycles? Absolutely not. Will astronomical valuations on stocks that are 2-3 years away from profitability be normalized? Most likely. Just be cautious about where you place your bets.

Excellent write up Dillon. I really look forward to these updates