Mid-Week Memo: The Market Pauses on Fed Minutes

Mid-Week Memo: The Market Pauses on Fed Minutes

Markets stalling, is it time to hedge?

The story this week was the release of Fed minutes. As of writing, it’s Wednesday and the new data came out today at 2:00 PM EST.

The Federal Reserve is the biggest player on the block, meaning it’s the biggest player in the markets. The best way to think of this is that, if the Fed was a business, they would be more profitable and bigger than Apple. Now, imagine if Apple (or a company bigger than Apple) had no other job than to buy fixed income (bonds) and set the interest rates in the economy. This company could also move financial markets by influencing how the entire banking system works through various “tools”.

The Federal Reserve is the beating heart to the economic and financial system as a whole. This is why paying attention to the Fed is so important. They set the tone of the direction of the financial markets and the broader economy, as a whole.

In this weeks memo, I am going to bring to your attention a few key data points I gathered from the Fed Minutes, my take-a-ways, as well as what I think this means for the direction of the markets on a go forward basis.

Estimated time to read: 5 minutes

Fed Minutes

First, I am going to provide you a few key highlights from the minutes and translate them to condensed plain English. Then, I am going to provide a conclusion tying all the data together to make an assessment of what to expect moving forward based on the Minutes.

1.) Markets are pricing in and expecting inflation to come down because commodity prices are going lower

2.) The market expects a .75 bps in June, .50 bps in September and to top out at 3.4% federal funds rate by end of year. In 2023 - 2024, the market is expecting rate cuts with a higher likelihood of moving down toward accommodative rate levels.

3.) When it comes to QT, the Fed appears to be judging overnight reverse repurchase agreements to be a gauge of excess liquidity. They believe further QT will bring the demand for reverse repo’s down in the coming months.

Basically, they need this chart to come down. If you notice in early 2021, reverse repo’s sky rocketed. This had to do with a policy adjustment done by the Fed which relaxed requirements to do reverse repo’s.

The Fed perceives this as excess liquidity in the financial system. We will see what the financial system needs and doesn’t need. I believe the Reverse Repo market places a big question mark on the Fed’s QT goals.

4.) The financial markets have already tightened financial conditions. I talk a lot about how the market has done a lot of the tightening for the Fed, this is why the 2-year yield and 10-year yield ran up so much higher than the FFR (federal funds rate)

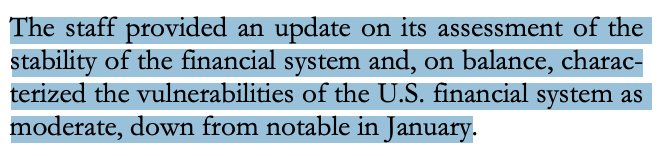

5.) The Fed does not see any stresses on the U.S. financial system currently. This is bullish and eases concerns (currently) of a credit bust.

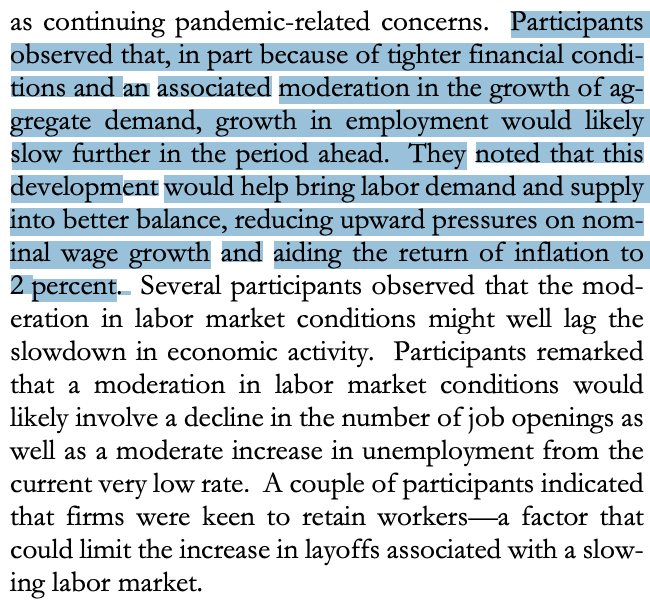

6.) The economy is expected to start slowing down and the job market will cool off

7.) They expect tighter financial conditions to moderate growth and bring supply and demand back into balance but that higher unemployment appeared unlikely

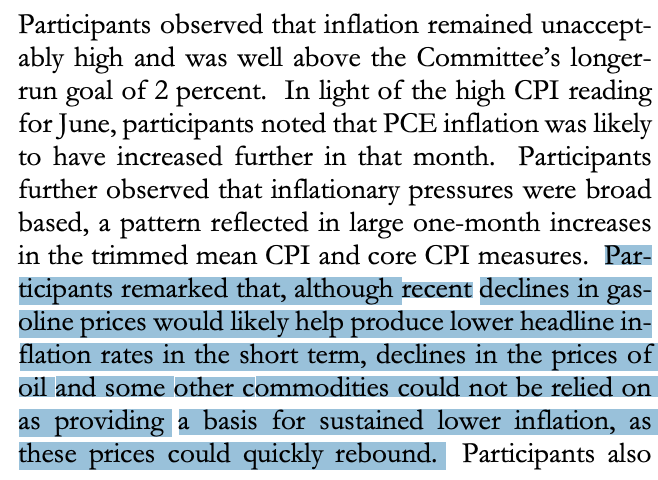

8.) Investors and traders should not rely on gas prices alone to be a leading indicator of inflation. In my opinion, a lot of the inflation was a result of increased energy prices but they are volatile. This means broad based prices are likely to move slower than the price of gas will in the coming months. They are related but gas could spike in any moment.

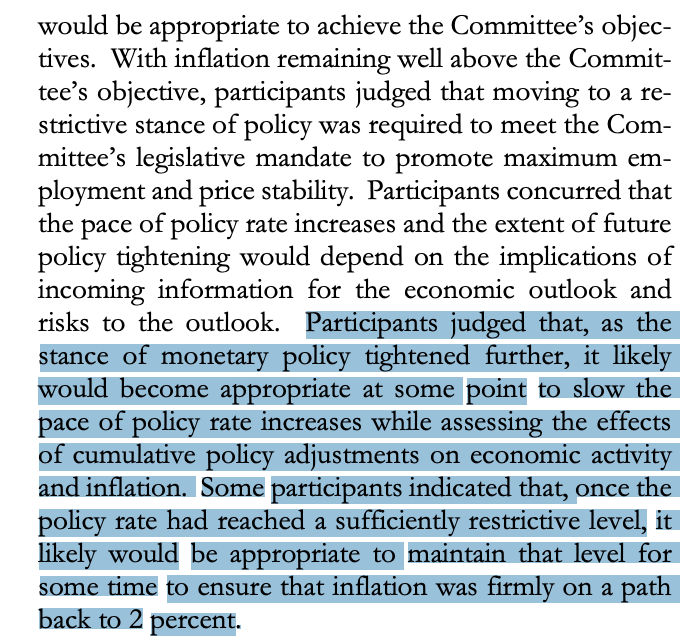

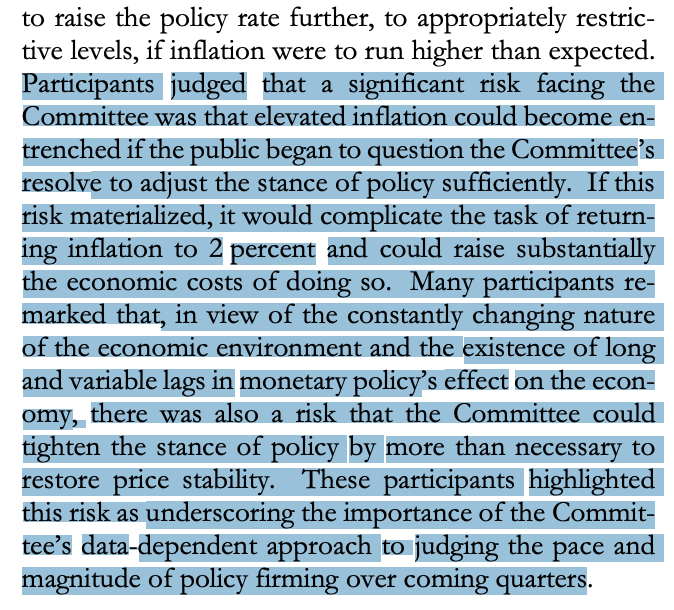

9.) This (below) was more hawkish. They are effectively observing that they ‘think’ that we are at neutral but neutral may actually be higher because of inflation. This would be a bad thing because that means rates will rise and equities will move lower. More on that in the conclusion portion of this memo.

10.) The Fed is going to remain data dependent. That means that nobody truly knows what the Fed will do because the Fed doesn’t know what they are going to do. It depends on incoming data in the new few months.

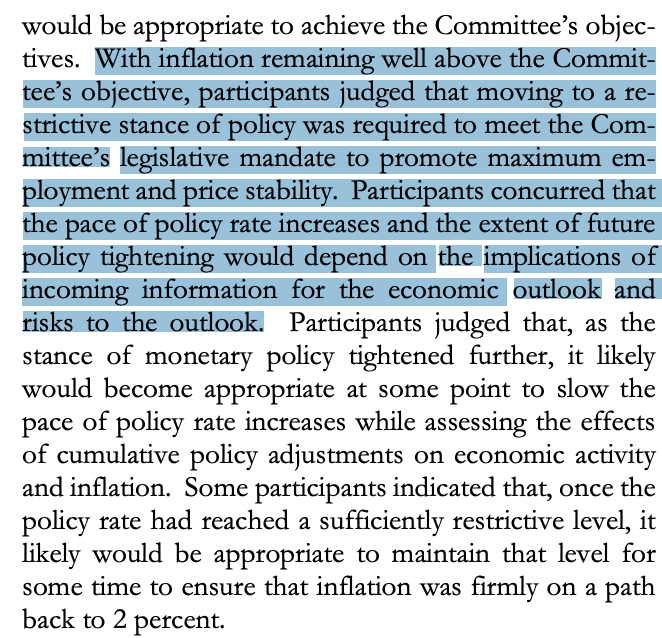

11.) This (below) was bullish. They are hinting toward a pause in rate hikes to see what happens with the economy. Essentially, they are not trying to break the financial markets or the economy. They want to raise interest rates above neutral to slow inflation, they think they are currently at neutral and it would be appropriate to go slightly above and stop for quite some time. Until the data suggests otherwise.

If we are at neutral and the Fed thinks we are at neutral, we will go slightly above and likely stop hiking. This will lead us toward a restrictive economic environment but the restrictiveness is at peak, which would be bullish for equities because there is “no where to go but up”. That means the worst is behind us. We will likely see a massive rally (far past ATH’s) when the Fed takes the foot off the breaks and actually cut rates.

12.) They are basically saying, “take us seriously because if you don’t we will crush the economy and financial system” in order to combat inflation

Tying All The Data Together

First let’s look at the yields at of close of business today.

The Federal Funds Rate is currently at 2.25% - 2.5%. This means that the markets have already “priced in” rates to be at approximately 3.25% - 3.5% as you can see on the 1 year and 2 year yields. I can explain further why, but I’ll simplify by saying that banks and lending institutions use the risk free yield (treasury bills) to set interest rates for riskier assets (lending to people and consumers). This means credit conditions are already restrictive today.

In the Minutes, it largely told us nothing new. We expected everything and a majority of the move has already been priced into the equity markets and bond markets.

The reason why the markets crashed since November was that markets were “re-rating” valuations as credit conditions became more expensive. This impacted credit sensitive areas (like growth stocks) and re-rated their valuations to their more historical norms. Basically, growth stocks became fairly valued and so did the broader markets as a whole.

Do currently bond valuations justify further down side in the markets?

No, they don’t. From a multiple stand point, valuation re-rating is likely behind us. Our biggest risk at this point is deflation, or a credit bust. However, above, you can see that on a historical basis rates as still low.

The Economy, at these levels, is likely going to be ok assuming nothing “breaks” or we don’t begin a credit super cycle.

Looking Forward this is What We Can Assume About the Markets

Markets are going to continue to climb their wall of worry and the technicals support this thesis. The market momentum is clearly to the upside as we begin our trend higher.

Because multiples have stabilized, and so have interest rates, I expect the markets to move faster in some areas and slower in others. What I mean specifically by this is that I believe organic business growth will yield return on investment in the quarters to come.

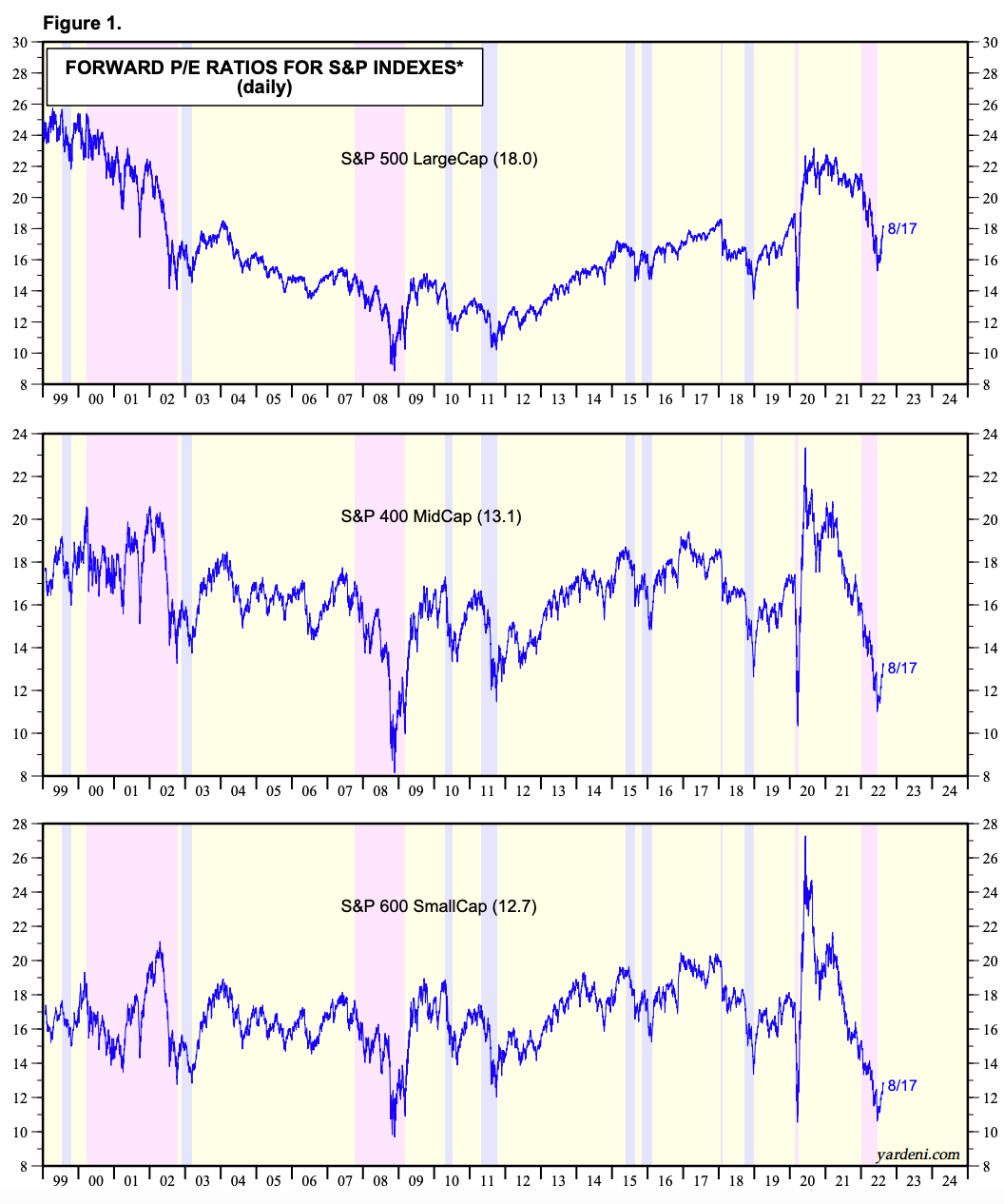

On average, the S&P 500 yields approximately 9% a year as this is reflective to intrinsic earnings growth. I find that strong growth stocks with good business fundamentals will outperform. As indicated below, small caps have clearly been decimated and offer attractive upside.

Have you seen my SubStack on STEM 0.00%↑ as a small cap business idea?

In Conclusion

The Federal Reserve hiking cycle is priced in. If inflation persists higher, then yields will re-rate and stock multiples will come down. This has the potential for markets to move lower but undercutting the lows as some on FinTwit suggest EVERY DAY, I am not sure about that. I think the market low was in June.

The Federal Reserve will hike to 3% - 3.5%, depending on incoming data, but they should actually cut rates shortly after to approximately 2.5% - 3% (depending on the data). This will, in the Feds eyes, still be restrictive and above neutral but will yield to a more stable growth for the economy. The goal of the Fed was a soft-ish landing, which meant that we could see a few quarters of negative GDP but as long as the financial system doesn’t break, we should realistically get through this in one piece.

If the Fed somehow pulls off this soft-ish landing and it’s clear that the inflation has finally subsided the Fed can move toward a more accommodative stance. When this happens we are going to resume the secular bull market rally for the next few years. In my opinion, all of 2022 has been a good time to buy especially in certain areas of the market like small caps and growth stocks. I still think now is a good time to buy from a dollar cost averaging stand point.

Incoming data will be crucial to monitor, don’t skip a beat as I continue to keep you guys all updated. Paying subscribers get the opportunity to see all my stock picks, my growth portfolio and access to our Discord channel where hundreds of members are.

Until then…

Stay Tuned, Stay Classy

Dillon

Nice overview! I've heard the the below statement translated as they may hit what the consider to be peak rates and hold, and that the market may be too ambitious in thinking rates will be immediately cut in 2023. No opinion, just another theory being tossed around. I do think they will slow the rate of hikes and see how the existing rate hikes manifest themselves.

"Some participants indicated that, once the policy rate had reached a sufficiently restrictive level, it likely would be appropriate to maintain that level for some time to ensure that inflation was firmly on a path back to 2 percent."