My Warning to ALL Investors: 2008 Global Financial Crisis to Now

All Investors both Passive and Active Need to Understand What We Are In

This may be the most important Substack I have ever written. Not because I am actively looking for clicks and views but for the sake of all investors understanding the severity of the situation we are in. I believe today, we are making history and only a few people know or understand it, so far.

We have never seen elevated inflation (almost hyper inflation) since first implementing QE in 2008.

This is relevant for all investors; passive and active. It’s even relevant for the average American with a 401k and who is seeking to understand what inflation means and how it is going to impact their net worth. More importantly, our global economic position and financial system as a whole.

I am trying to emphasize the importance because it is important. Inflation is a bigger problem than just gas at the pump being too high. It begins with what the Federal Reserve and U.S. Government did during the 2008 financial crisis.

I believe it would be beneficial for all investors to read this through to the end.

2008 Was Supposed to be a Great Depression

The history books have already been written about the 2008 GFC. Many people interpret it as the housing market crash but truly, it was more important than that. It changed the way our economic system as a whole operates with the first ever introduction of QE, or quantitative easing, in the U.S. financial system. To explain:

Quantitative easing is the Federal Reserve (U.S. central bank) actively buying U.S. treasuries (U.S. Government Debt) on the open market to influence asset prices and control economic growth.

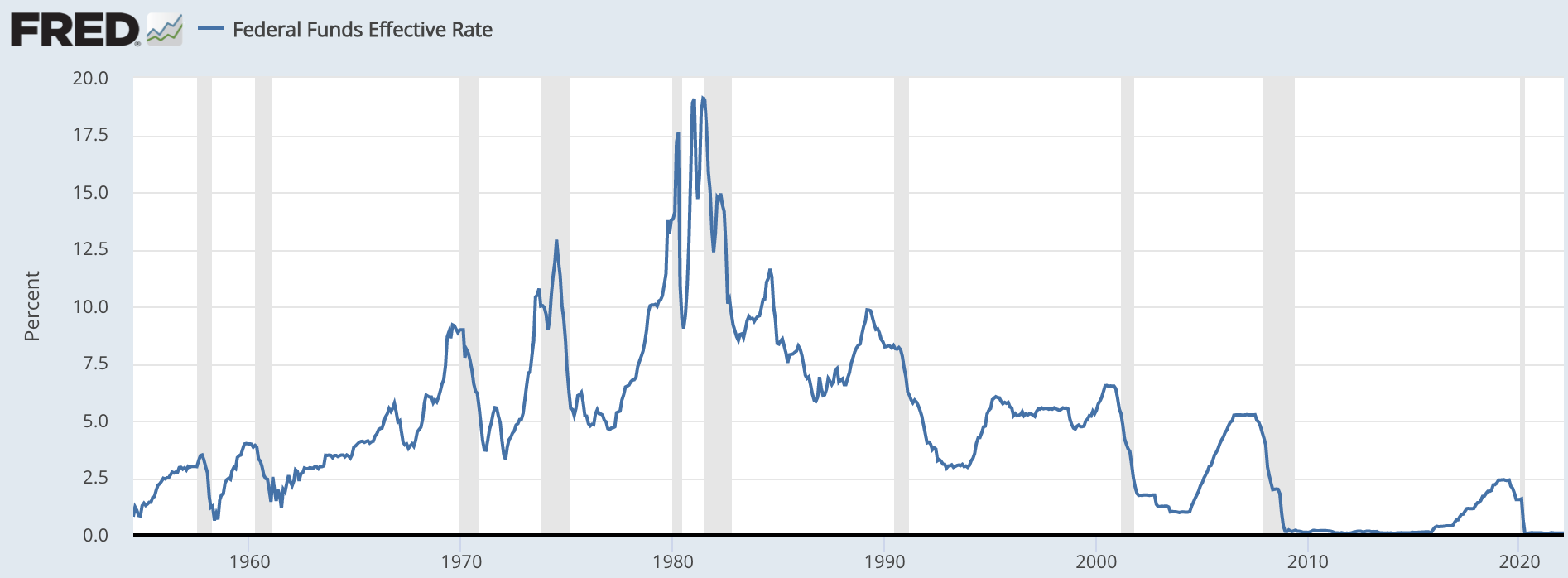

The Federal Reserve has been silently working in the back ground for the past 100 years and is the culprit of every major economic and market bust. Prior to QE, they have been using interest rates to influence economic booms and busts. If you recollect two of the biggest market crashes in recent history; 1999 and 2008, you can see the Federal Reserve hiked rates too far too fast which created a recession and a market crash.

The grey lines are periods of economic recession. Notice how the blue line (interest rates) spike before every major recession.

But, 2008 - 2009 was different

Prior to 2008 and 2009 the Federal Reserve would simply lower interest rates to stimulate economic growth during struggling economic periods. They did this because it stimulated borrowing by making the cost of credit cheaper. Basically, when you let people borrow money for cheap they can “afford” to buy more things, creating economic growth. The long term problem with this is that the Fed couldn’t ever get interest rates back to the previous high since the 1980’s. It’s complicated why this is but it can be simplified by how, structurally, economies have evolved due to lower population growth and productivity of that population.

The recession in 2008/09 bore striking similarities to another period of our young American history, the Great Depression. For many who are not entirely familiar why this happened, it had to do with lending practices of mortgage companies. Essentially, they were structuring bad loans to people who were not credit worthy. Then, they would package these bad loans with good loans and sell them to investors on Wall Street. The problem with this is that these packaged loans were supposed to be low risk investments. But, when the housing market began shrinking, many people began defaulting on their loans.

When otherwise low-risk assets began becoming worthless, this drastically impacted the banking system and financial institutions. Banks like Lehman Brothers evaporated over night because a large portion of their assets disappeared. When banks began going bankrupt, this created a chain reaction in the entire banking system that was going to lead to an economic collapse. Economists would call this a credit super cycle.

There was one other time in recent history that this happened, 1920 - 1929. The principle was the same but it was different. The bad lending practices happened in the stock market. When the stock market began collapsing, people began defaulting on loans they took out to buy stocks. When they defaulted on the loans, the banks assets evaporated over night creating a collapse in the banking system. 2008 was identical except it was in the housing market this time.

This leads to the question, why didn’t we experience a Great Depression in 2009?

The Federal Reserve Got Creative

Politicians began scrambling by 2009. They knew they had to do something. Every day the stock market was falling. American’s 401k’s evaporated, houses were declining in value, people were losing jobs and banks began disappearing over night. What’s even worse is that it wasn’t just Lehman Brothers that defaulted. The financial crisis was going to impact Goldman Sachs, Bank of American, and JP Morgan. In the event these financial institutions went bankrupt, it would be at a point of no return. We would experience the worst depression since the 1930’s and possibly even worse.

There was Only One Solution to this Problem; Congress Had to Pass the Infamous Wall Street Bailout.

There were multiple factors that had to go into this when thinking about how to keep our economic system in tact. Keep in mind, during this time we were in economic turmoil and a near collapse of the banking system was taking place. In response, the Federal Reserve enacted a few radical policies to boost lending and stimulate economic growth. The first being aggressively slashing interest rates down to near 0%.

Remember, as mentioned above, the Federal Reserve lowers and raises interest rates to influence economic growth. In December 2008, this was the first time interest rates got to near 0%. But, it was clear that this time was different and simply lowering interest rates wasn’t enough.

The Emergency Economic Stabilization Act of 2008 was passed as a way to provide relief for the banking system. Essentially, it was a $700b bill that purchased troubled assets (mortgage securities) of banks and provided new liquidity for the banking system. Despite this being very unpopular among the general American population, this saved our financial system.

The Introduction of Quantitative Easing

As a response to the 2008 global financial crisis, the Federal enacted QE for the first time in American history. Quantitative easing is a new and experimental method of financing/monetizing debt, most often government debt. Many would think of this as “money printing” but it’s not necessarily a direct money printer. As mentioned above, it’s a way for Central Banks to buy debt. They can buy mortgage debt (like they did in 2008) or, they can buy U.S. treasuries.

The explanation why central banks will buy government debt is subjective with what they are trying to accomplish. I can write an article publication on QE and its inner workings but this is about why and how this is important. Simply, we know a few key important details about how QE impacts the financial system:

QE heavily influences asset prices in both stocks and housing

QE creates inflationary pressure, which can be good in the event we are struggling with deflation (think 2008)

It allows the U.S. government to have unlimited spending ability (probably not a good thing but sometimes not terrible)

It is important to understand that central banks have an absolute monopoly on money supply. When you have a monopoly on money supply you have an unlimited ability to expand and contract that money supply. In addition, it does not matter if a central bank holds good debt or bad debt because if somebody defaults on a loan, it simply disappears and is absorbed.

2008/09 was the First Time the U.S. Introduced QE

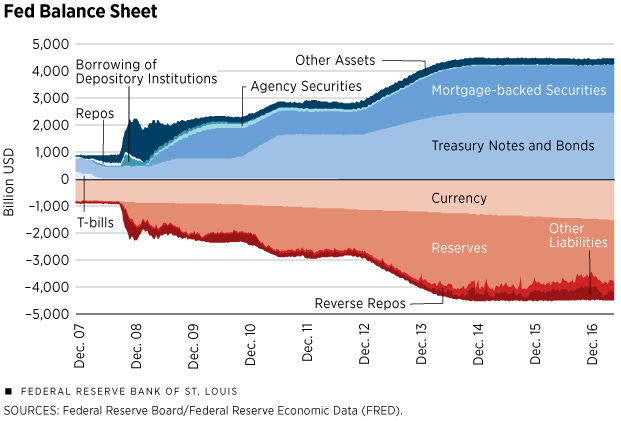

In an attempt to combat the defaulting domino effect that originated in the housing market, the Federal Reserve announced on December of 2008 the purchase of $1.25 TRILLION in mortgage backed securities.

In the image above, you can see the Federal Reserve began increasing its balance sheet in December of 2008. In particular the MBS’s and treasury notes. Effectively, this brought an extraordinary amount of stability to the housing market because banks (JP Morgan, Chase, Goldman Sachs, etc.) didn’t need to hold the bad loans anymore. The Federal Reserve would simply purchase these, thus bringing stability to the financial system.

The Economy Didn’t Only Stabilize, All Assets Began Stabilizing Shortly After.

Almost immediately after, stocks bottomed with one final leg down in March of 2009. From peak to trough, the S&P declined 50%. What’s scary is that stocks would have likely experienced a 1929 decline of 90% in stocks had the Federal Reserve and U.S. Government not intervened.

Quantitative Easing Was Supposed to Be Temporary but the Federal Reserve has Done it Four Times Since 2008

QE dramatically impacts asset prices and there’s no more clear way to see this when correlating the S&P 500 with the FOUR QE programs done since the bottom of the 2008 financial crisis. QE dates, amount and Federal Reserve Balance Sheet:

Note: The asset column on the feds balance sheet reflects the amount of assets (government debt and consumer debt) it has purchased and holds. Notice how closely it is tied to the S&P.

QE1: December 2008 - March 2010, the first round purchasing $175B in agency securities and $1.25T in mortgage backed securities

QE2: November 2010 - June 2011, purchases of $600B in long maturity treasury securities

QE3: September 2012 - October 2014: Purchases of mortgage backed securities and long maturity treasury securities (bonds). This came in the form of $40B per month of MBS’s and $45B of long-term T-Bills (government debt).

QE4: March 2020 - March 2022: Purchases of MBS’s and T-Bill’s valued at $40B per month for MBS’s and $80B per month in T-Bills.

Every time the Federal Reserve implemented the QE program, this dramatically influenced asset prices. This is the most apparent when you can see what happened during QE4, which has been the most aggressive program yet. As many of you still have the Corona Virus pandemic/lockdowns fresh in your memory, this was the time that the stock market absolutely ripped form the depths of the crash to all time highs. From top to bottom, the S&P rallied 100%+. The NASDAQ is a similar story where it bottomed at 6,600 in March 2020 and rallied to 16,000 by November 2021.

November 2021 is when QE began to taper, reducing asset purchases from $120B/Month to $0 in March 2022. This has been the most aggressive tapering process.

My Warning to All Investors and Why Inflation is the Cause of a Major Market Top

All the information I have described to you above is meant to support the point of the article. I understand that many investors haven’t sought to understand, were unaware or haven’t had the time to understand what our government and central banks have done. The Federal Reserve has created the largest everything bubble in stocks, crypto and real estate because of quantitative easing.

Yes, I am aware of what I am claiming right now and I believe with the NASDAQ down 22% and the S&P down 12%-13%, this is only the beginning.

A Bubble That We Have Never Seen

The Federal Reserve and Central Banks all over the world have created a bubble through money printing (QE) and have kicked the can down the road since 2008. This was all fine and dandy until inflation became out of control. The reason why; QE is extremely effective in a growing globalized economy but becomes extremely inflationary when globalization slows. Globalization in itself is very deflationary because this prevents any sort of wage push inflation and also distributes the printed American dollars to economies all over the world.

To understand why globalization is so deflationary, think of America as a centralized hub of the global financial system. If we print money, it’s not a big deal if we continue to run trade deficits and send many of our dollars overseas to other countries. But, if we restrict trade or globalization practices, those dollars don’t have anywhere to go. The dollars are printed and stay in America, which increases the money supply domestically at home. Increasing the money supply devalues the dollar because you have MORE of it sloshing around.

Originally, the secular forces of deflation were going to take hold this year probably around this time. But, TWO major events have taken control over the past 2 years that have disrupted everything:

COVID-19, lockdowns, and governments restricting interaction with each other

An escalating conflict with Russia/Ukraine where sanctions are being implemented all over the world

When COVID-19 abated the ideal situation would have been that we re-institute globalization practices and continue to integrate our economies. Unfortunately, this hasn’t been the case because the lockdowns and restrictions lasted longer than originally thought (Canada, Australia, California & China). In addition, we added the icing on the cake for our destiny with extreme global sanctions due to Russia/Ukraine war.

The United States has written their own destiny with poor policy and excessive spending. The worst part of all of this, a recession is becoming a likely scenario in the months ahead. You can read about that here:

The Asset Bubble Doesn’t Have an Option, it Has to Deflate

If I still have your attention, I congratulate you because this has been something I have struggled with for months. In November 2021 at the market top, I knew what was coming when I published this article:

But, it wasn’t that easy. How am I supposed to truly believe that we are going to experience a major down turn? Since 2008, the Fed has saved us every time the market began to stagger. During this time, I knew asset prices were going to decline but not to this extent. In addition, in the unknowable future, I decided to wait and see how everything would evolve. By nature, I am an optimist and always believe things will work out. But, the worst case scenario is evolving and the war was the icing on the cake. The war has added fuel to the fire by:

Adding to the bull market in oil & gas prices

Increasing recessionary risk from sanctions

Increasing inflationary pressures through higher gas prices and trade/globalization restrictions

When thinking of asset prices, because of inflationary pressures, there really is only one way they will head… Down. The number 1 reason why, we were already in an asset bubble and inflation/war is the pin that popped the balloon. We cannot implement QE like we have for the past 14 years to keep inflating asset prices and the economy. THE FEDERAL RESERVE HAS TO FIGHT INFLATION, they cannot implement QE or ease monetary policy like they have done in the past during every other Bear Market since 2009.

CPI is at levels comparable to extreme periods of inflation in American History. In 1973, the S&P declined 45% when fighting that period of hyper inflation.

Where Asset Prices are Going

To get an understanding how far this bubble has been extended by the Fed’s QE program, we have to look at a few charts that paint the appropriate picture.

Net worth by % of disposable income has superseded the global financial crisis. This means that wages have not gone up but net worth has. This tells us that asset prices have gone up too fast and too far.

The price of homes have already began ticking downward. Low interest rates and QE have brought homes to record high levels. The Federal Reserve needs to raise interest rates, making the monthly payment more expensive for mortgages.

The S&P 500 has risen to extreme valuation metrics comparable to the 1999 .com bubble. The black line below represents where stocks have historically bottomed out in every major market crash aside from the 2008 global financial crisis. If we end up in economic turmoil from fighting inflation (and possibly war), stock prices can get down as low as they were in 2008. The conservative case is stocks falling to a forward P/E of 13/14, roughly 30% lower from here, similar to stock bottoms in 2018 and 2020. The worst case is a forward P/E of 8/10, 50% lower from here.

The key take away here is that stocks are NOT safe despite what the past 14 years have told us. This means that 401k’s are at risk of declining 40%, depending on the structure. This means that growth stocks, the NASDAQ, and unprofitable stocks don’t have a bottom and could fall to bare bone valuations. Lessons that we have learned since the bottom of the GFC bust need to be evolved and looked at differently. Valuations will need to come down before stocks think about bottoming.

Something important to note, in 2018 and 2020 bear markets the Fed stepped in and implemented a more accommodative fiscal policy. This is something that wont happen now until inflation comes under control. While combating inflation, a recession is a very likely scenario. We haven’t seen a real recession since 2008.

The One Asset that Historically Performs Very Well During Times Like These

There is one asset that historically performs well during periods like this and it’s not oil, it’s Gold. There are a few charts I want to show you so you can see what I am seeing as a possible “safe haven” to put your wealth while the Fed and the U.S. Government works through this challenging economic period.

Gold

During the 1970’s hyper inflation, the Fed finally raised rates to 20%+ in 1981. We can use this period as a moment in time when fiscal policy became extremely tight, similar to what we are likely to experience. Gold rallied from $200 - $800. From 1981 to 2008, you can see Gold formed a “cup and handle” pattern where it rallied from $700 to $1900 an ounce over the next 4 years during the GFC.

Gold is now showing a similar cup and handle pattern. The benefit here is that it historically acts as a “risk off” asset. It wouldn’t surprise me to see Gold rise by 150% or 300% over the next few years much like it has in the past during Federal Reserve tightening cycles and economic recessions.

Summary & Conclusion

The goal of this publication was to explain the historical context of how the markets got here and how the market bubble has formed. Essentially, it was the Federal Reserve buying U.S. treasuries (debt) and MBS’s (mortgage backed securities). This trickled to the equity (stock) market where valuations have gotten to levels last seen during the 1999 bubble. Previously, the Federal Reserve has kept this bubble propped up by reversing monetary policy, keeping it accommodative, and stimulating economic growth.

CPI inflation is currently at 7.9% with no sign of slowing down because of the war and supply chain challenges. Inflation has become public enemy number 1 and the Federal Reserve must combat it. Because of this, the bubble created by and propped up by QE CANNOT be used. In addition, the risks for a recession and credit unwind are very high just as it stands today, without tightening monetary policy. If you throw in tightening monetary conditions, a recession is a certainty.

The recession risk is the biggest risk of all because the Federal Reserve has no play book of how to deal with a recession when CPI is already at 8% (this is called stagflation). The have lost control, creating a bubble and inflation, and now have no choice but to let the system unwind and “reset” itself. There is no telling how long this will take, what will happen next. There is only one conclusion:

This is NOT the time to take risk. It is smarter for investors to be in risk off assets like Gold, Bonds, or Utilities until this clears up and the Federal Reserve gets the financial system under control.

BluSuit Moving Forward

I have historically covered growth stocks since I began this SubStack. During this time, we will be covering all asset classes, macro-economics, fiscal policy, and market direction. In addition, I will still cover growth stocks because innovation is real and a secular force in the economy. But, in order to best manage risk and provide the best value for BluSuit readers, I will discuss risks, uncertainties, and market outlook on top of stock picks.

Stay Tuned, Stay Classy

Dillon

So what shud be the action plan for investors. U didn’t comment on that at all.

Excellent article Dillon like all your other articles. Thank you.