New E-Commerce IPO: Brilliant Earth - Disrupting a $300B Market

New E-Commerce IPO: Brilliant Earth - Disrupting a $300B Market

Profitable, 77% YoY Growth, & Massive TAM

Digital transformation has not only affected the business and how it operates. It has impacted our every day life and what has emerged is a new way to do commerce in the form of “e-commerce”. Much like in the 1960’s where we began to see “super stores” like Target and Wal-Mart, some of the biggest business winners have sold direct to consumers. In some cases, it may not be as exciting as the hot new biotech stock, but having exposure to this secular growth trend is a must and should be on every investors radar. Every now and then I run across a truly simple, exciting and original business model. I believe Brilliant Earth has the potential to yield incredible long term investor returns as it disrupts an industry as old as man.

The pandemic was like putting fuel on an already growing fire, especially to a few different secular shifts: AR/VR, Telehealth, cord-cutting (streaming) and e-commerce. These trends were already trending upward, as Millennials began to represent the largest portion of the U.S. workforce, which is approximately 35% today and is expected to be 75% of the work force by 2030.

I am a Millennial, we were born during the first stages of the internet. Unlike our parents, we were just kids when we began experimenting with these new electronics and various different forms of connectivity. Think of millennials as the generation to be comfortable being early adopters of various different technologies.

With accelerated adoption of digital commerce, this new aged business model is all but certain to disrupt nearly all brick and mortar locations. The reason why has been and will continue to be disruptive, it offers a few key customer facing value adds that traditional retail cannot:

Customization

Optionality

Better pricing

Convenience

In addition to this, many e-commerce businesses run more capital efficient models due to the ability to maintain a low work force and low over-head from running an in-person location. An interesting stock that few people know about that has run a very successful model like this is LoveSac $LOVE. They allow people to come into small retail locations, customize their option, and it’s delivered to them a few days later. Small, simple, and efficient.

Brilliant Earth, the business this publication will cover, runs a similar model to LoveSac. However, they operate uniquely, covering multiple different segments of Jewelry rather than LoveSac really getting their bread and butter from couches. In this review, you’ll walk away knowing:

Their business model and case for accelerated growth

The market opportunity the operate in

Past financials and operating margins

Growth strategy by management moving forward

My conclusion and plan of action

Brilliant Earth - Technology First Jeweler

Business Model:

If I were to describe Brilliant earth with one line, I’d say it’s a digital first jeweler. They adopt many different technological trends to drive value to their consumers. It would be misleading to categorize them as only an e-commerce business. At first, they began in 2005 primarily an e-commerce centric business but they’ve integrated product visualization, AR/VR, blockchain to bring a unique omni-channel customer experience.

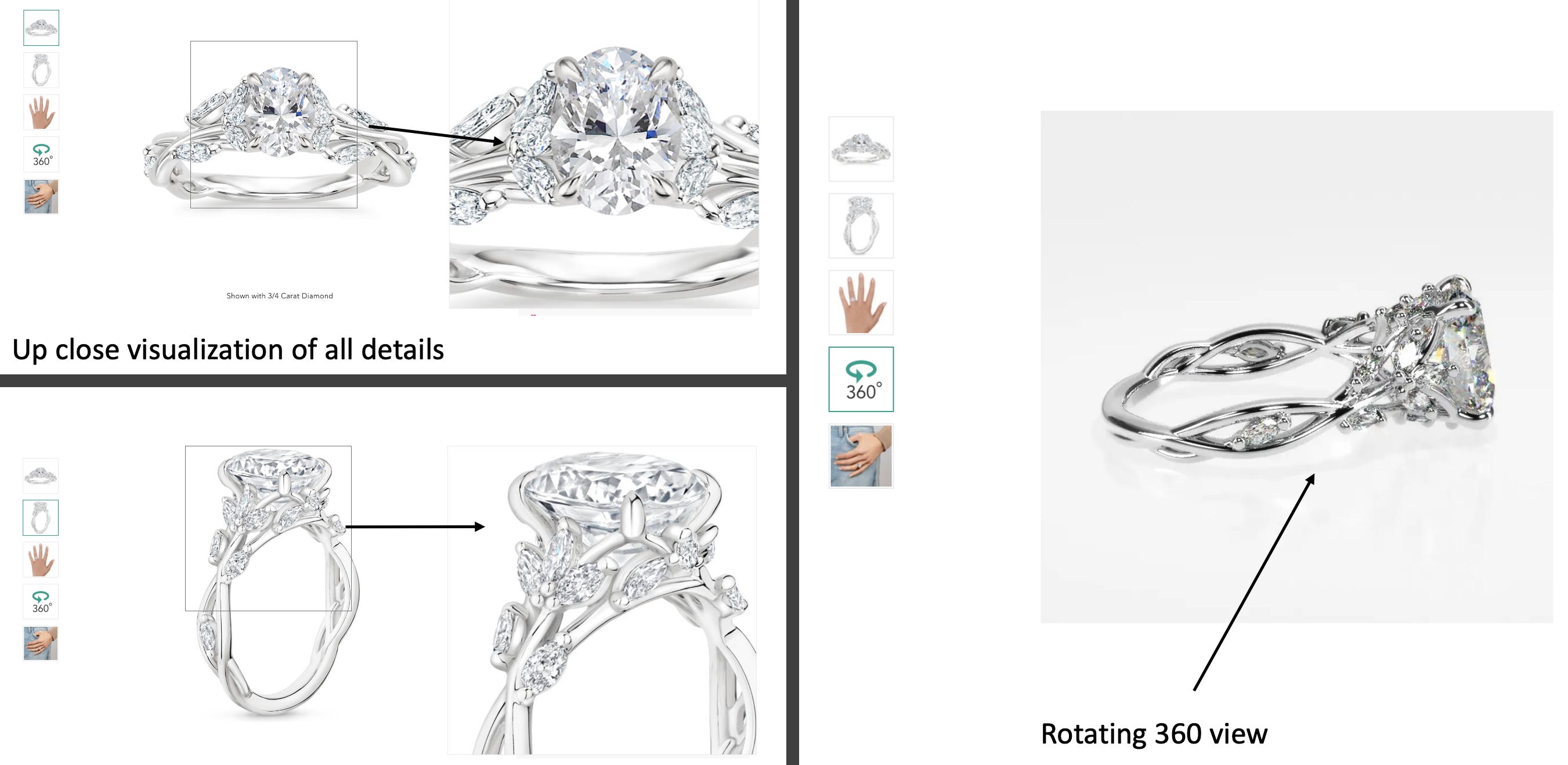

Brilliant Earth’s website has many unique capabilities, starting with product visualization (above) consumers can custom make their own ring/jewelry. I’ve found this was a major benefit to the ring I bought for my Fiancee’, she could customize the ring of her dreams rather than a limited selection at a brick and mortar location.

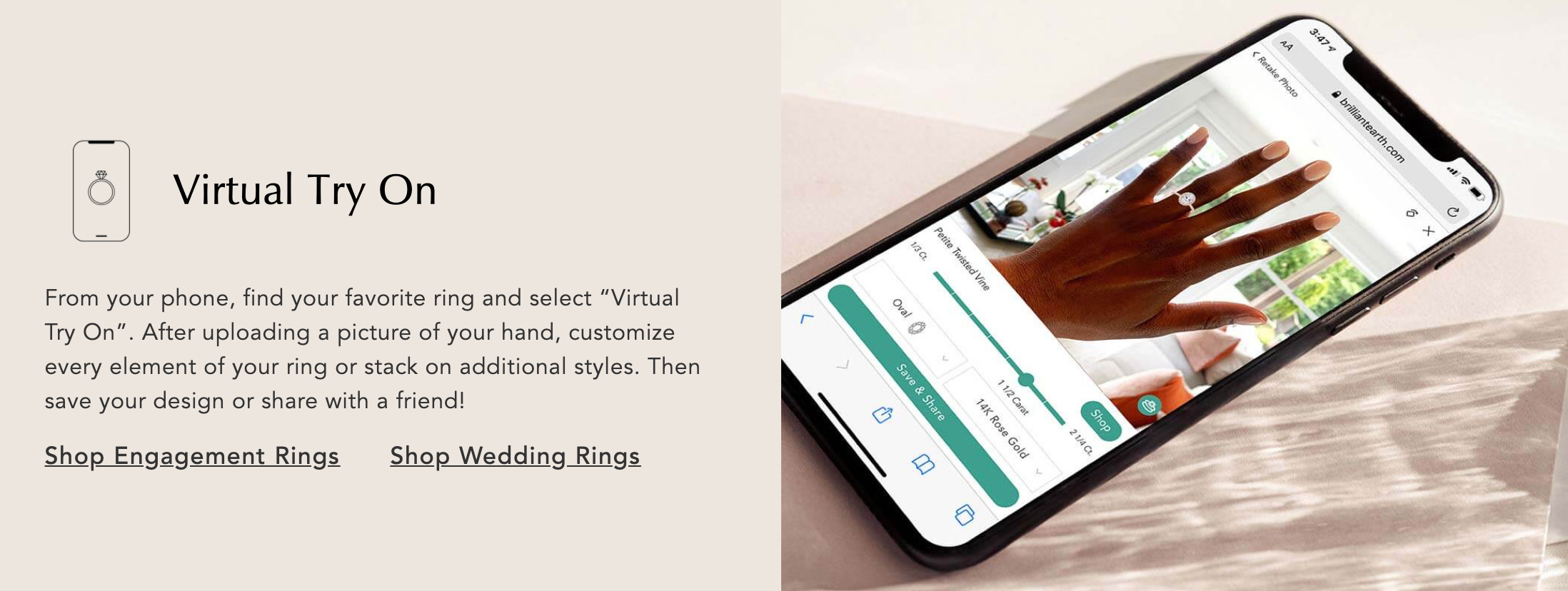

After ring customization, customers can leverage the virtual try on feature. This is AR/VR enabled tech, which is predominately in its very early phases of adoption. In the future, Jewelers that implement this feature the best could have a major competitive advantage to create the best, frictionless, and personal experience. I always assume a healthy amount of speculation on any investment decision. I could see (speculate) this becoming significantly more improved and important within Brilliant Earth’s business model.

Once the customer finalizes the ring (or piece of jewelry) of their dreams and it looks good through their virtual try on feature, placing an order is as simple as placing an Amazon order. Affirm can be used to break-up the payments with a 0% interest rate as well. This payment experience (from a Grooms perspective) is incredibly beneficial. Most American’s will find it difficult to pay for a $5k - $10k engagement ring out of pocket, this is why Affirms service is so valuable and businesses who offer their services instantly obtain an advantage. You don’t find this at brick and mortar locations. Typically there’s a long and complicated process for any sort of financing, or, you just have to throw it on a Credit Card.

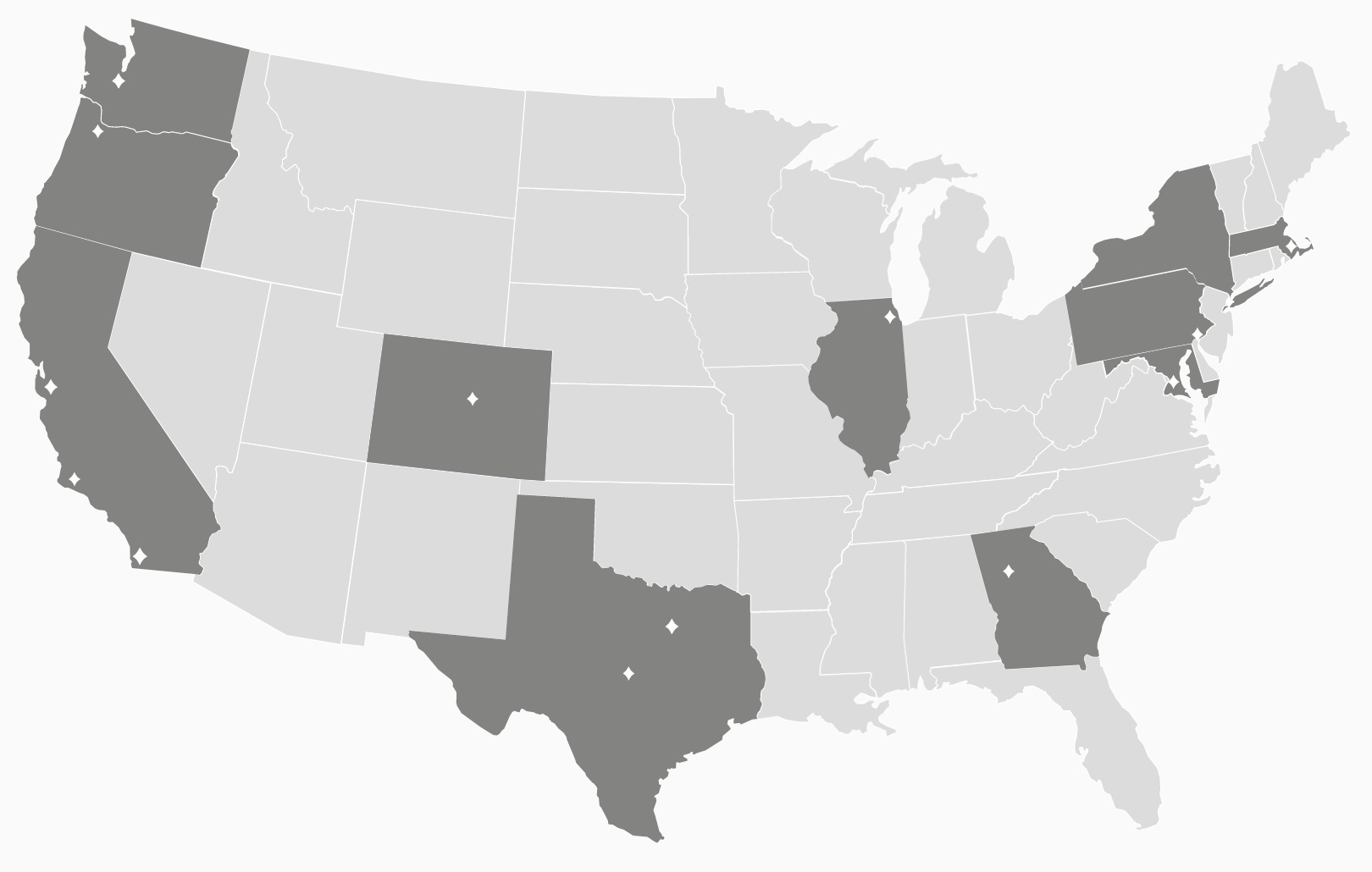

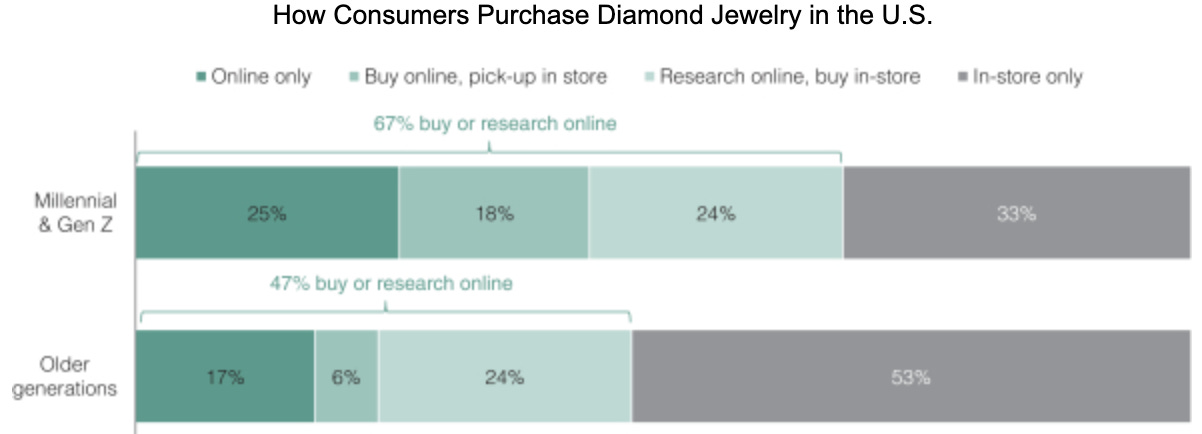

In addition to their superior digital experience, they have enabled an omni-channel experience through their show rooms. This is a crucial aspect to this investment thesis. They currently operate in in all 50 States but only have 14 show room locations. For every show room they institute, they have seen up to 80% growth in that designated area. This presents a massive area of growth as they expand nationally and even internationally by leveraging their digital omni-channel business model.

This show room and digital enabled experience has been carefully enabled through their data driven decision making. The important thing to understand about this business model is that, referring to the above, there’s a secular shift in millennial and Gen-Z spending and research habits.

Leveraging an e-commerce first but leveraging an omni-channel experience appears to have Brilliant Earth positioned for exponential growth.

The Market Opportunity:

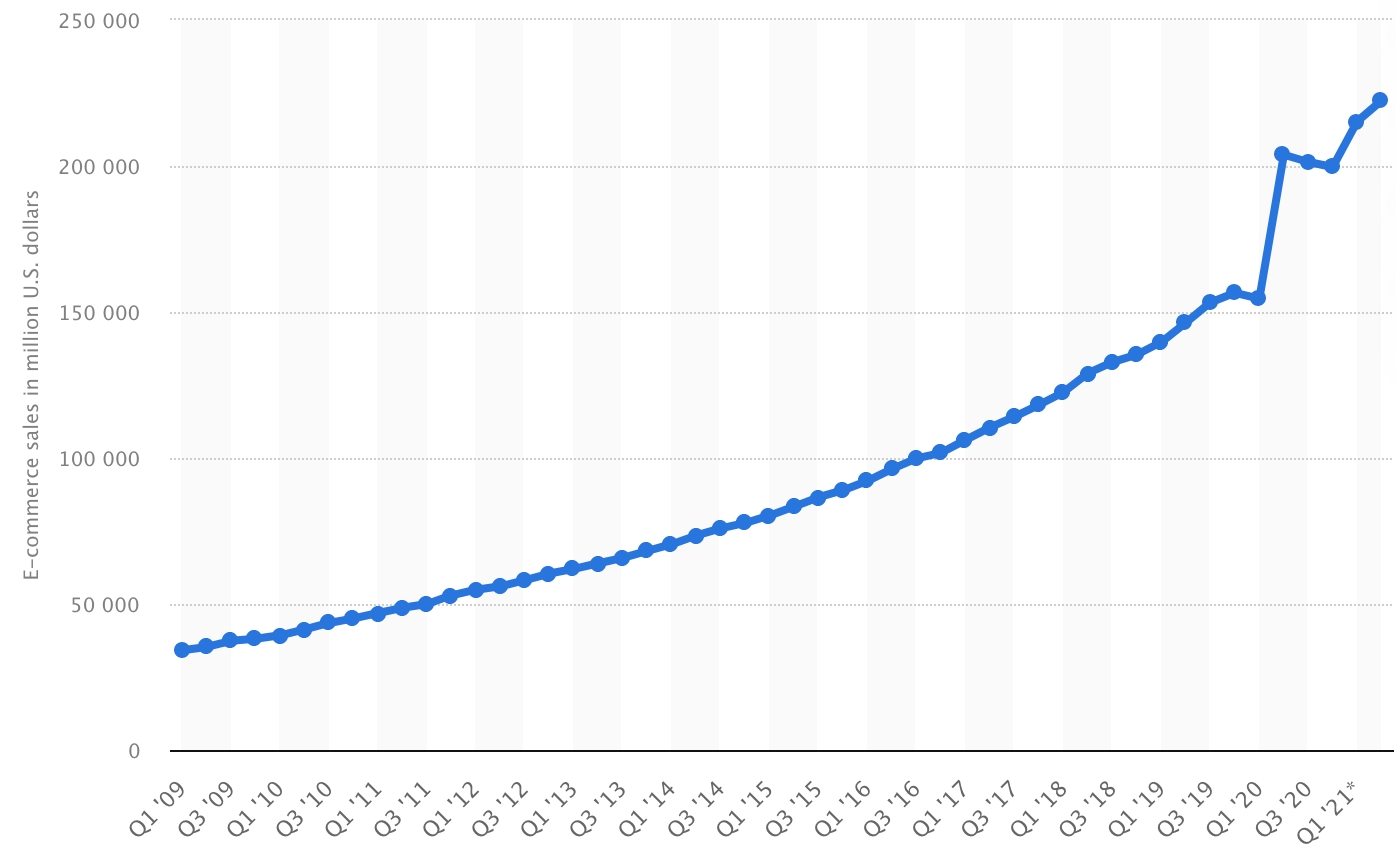

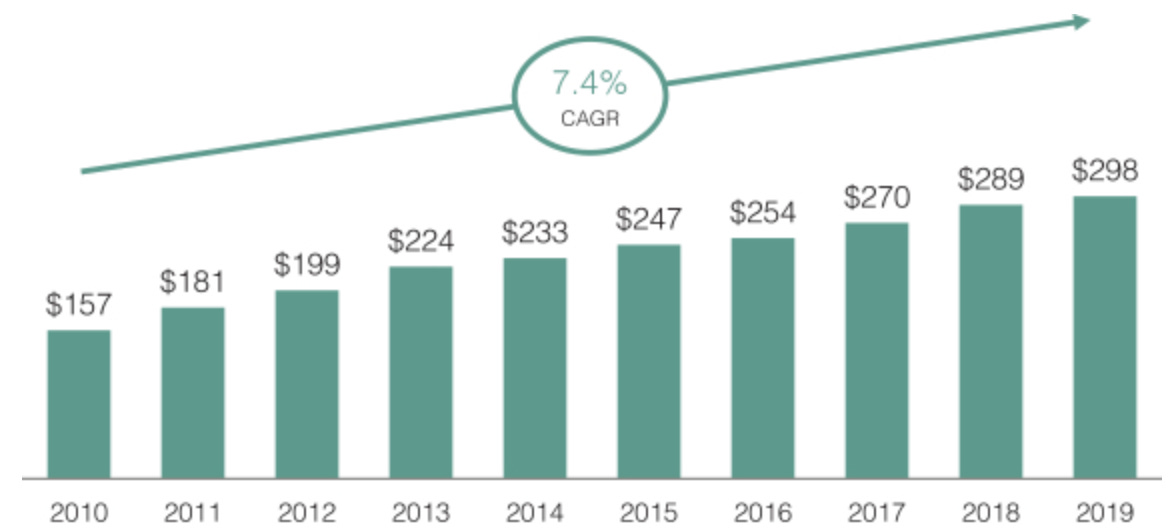

The jewelry market is massive being approximately $300B on an international scale and $60B in the United States. This market is expected to continue growing at a 3.7% CAGR until 2027. From 2010 - 2020, despite a 7.1% CAGR in the overall jewelry market, e-commerce was the fastest growing segment at a 15% CAGR. E-Commerce sales in 2020 consisted of 20% of all retail jewelry sales but per Bain.com, 90% - 95% of all consumers still prefer to purchase in store.

What is interesting with this market opportunity is that on a global level, no single business has more than 4% market share. Approximately 65% of the entire industry are composed of thousands of independent jewelers. The problem here is that they must maintain a high inventory and are struggling to meet consumers e-commerce demands. Unfortunately, Brilliant Earth is not the only online Jeweler that has recognized this with the primary competition coming from:

Blue Nile

Brian Gavin

James Allen

Leibish & Co

The competitors are well established each serving their own unique niche’, however Brilliant Earth appears to have the most show rooms of the online retailers and has the best technology available especially with their AR/VR offering. Arguably their biggest competitive advantage is their blockchain-enabled diamonds. They pride them selves on ethics. Customers can track exactly where the diamonds were created or mined, to where they are polished, all the way to their door step. They are one of the first jewelers to do this.

This ties directly with their mission statement, “To create a more transparent, sustainable, and compassionate jewelry industry”. They have approximately 10,000 block-chain diamonds today.

Financial Performance

There’s always a common theme to many stocks I am seriously considering or planning to buy, the most common trait is that they’re all profitable or could be profitable if they chose to be. Brilliant Earth is no exception.

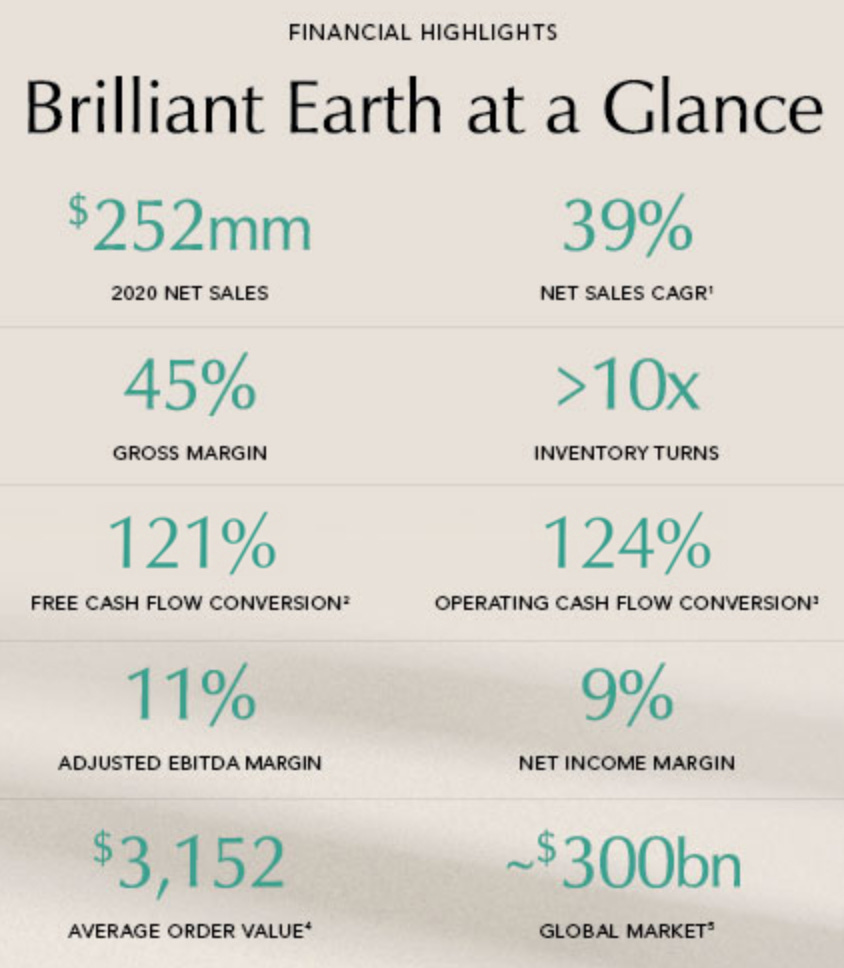

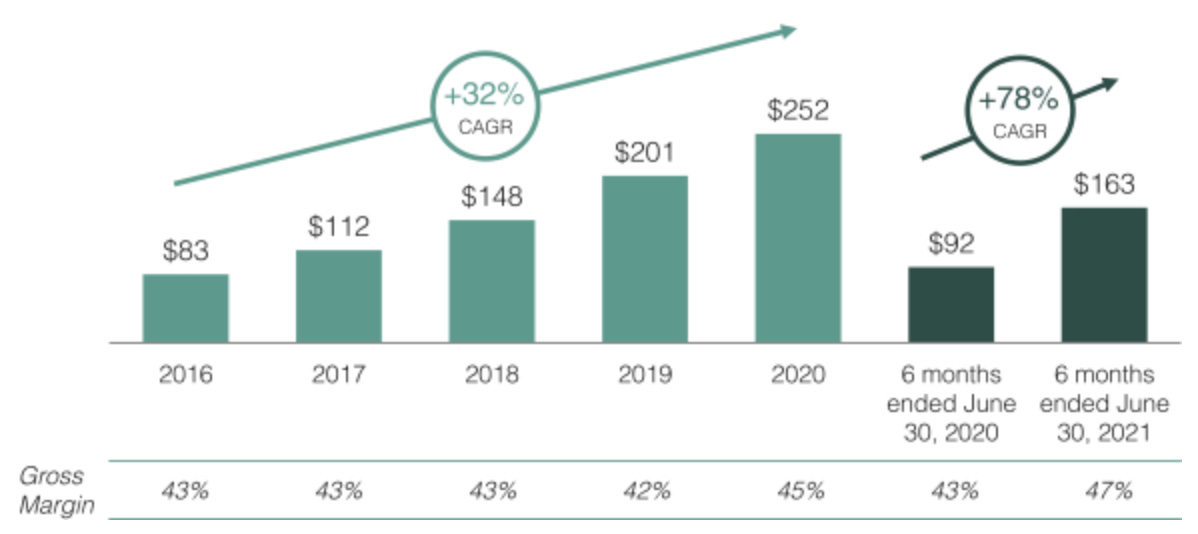

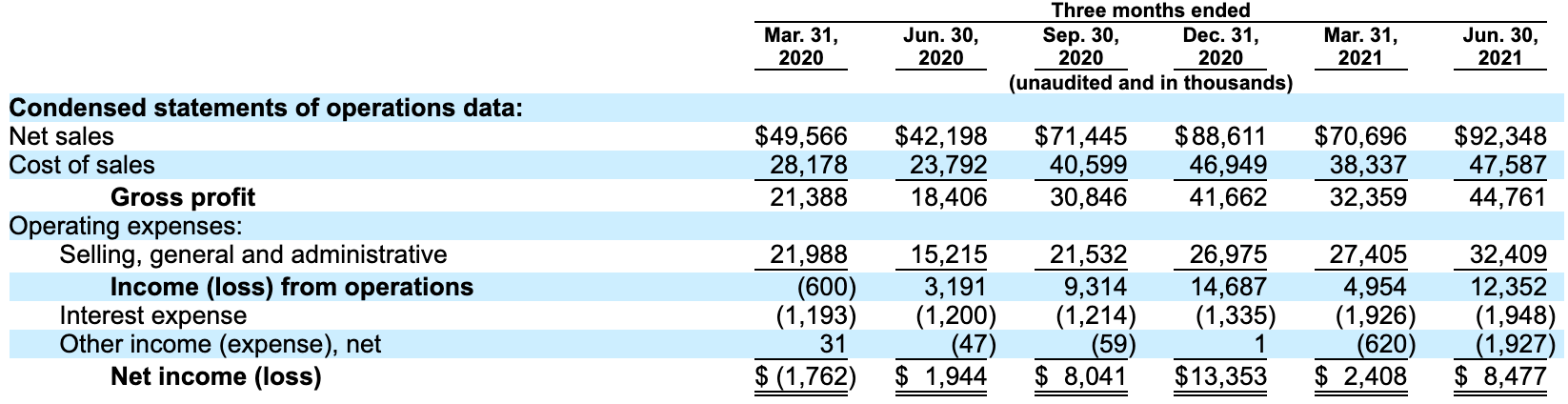

Their growth has been impressive for many years growing consistently at a 32% CAGR but first became profitable in 2020. Their revenue has recently grown 77.7% YoY for the first 6 months of 2021 over the first 6 months of 2020, but I do believe this has to do with a slow down in the business from COVID and growth becoming more normalized. I also this is a result of an accelerated shift toward e-commerce purchasing from a macro perspective. But, history has shown they don’t need lock-downs to successfully grow their business.

Operating margins and gross margins appear to be getting better with scale. Notice how in 2016 gross margins were 43% and in the first 6 months of 2021 it’s now 47%. Currently their operating margins have been consistent on a YoY basis, staying steady at 10.6% and then, obviously, their net-income is an impressive 9%.

It is important to mention that their business is seasonal with approximately 30% of their business coming in the fourth quarter. This is to be expected with Christmas being in Q4.

They expect to raise approximately $250m at a market capitalization of $1.4B which will put its valuation at an expected P/E of 35 for FY21 and a FY22 P/E of 27 leaving room for multiple expansion.

Strategy for Growth

I covered this briefly in the business model portion and I usually don’t do that when analyzing companies but it’s such an important part of this business. Leadership provides the following for area’s of expected strategic growth:

Increase brand awareness - Their brand awareness is currently 54% which grew from 43% - 54% from 2018 to 2021. They believe they can continue to increase this, especially with the Millennial and Gen-Z demographic. They have many social media initiatives and will continue to advertise and expand through various media outlets.

Expand omni-channel reach - They currently have 14 locations, which has expanded their e-commerce capabilities and sales. However, long term, they expect to expand to as many as 100 stores nation wide. This is a massive opportunity for growth, especially as they move internationally.

Expand purchase occasions for new and existing customers - The fine jewelry segment is an extremely fast growing segment and a largely untapped potential. 65% of the $300B jewelry market is considered in the “fine jewelry” market. They have just began investing in this category and they’ve already seen 100% growth YoY. They believe both new and existing customers will continue to purchase within their omni-channel approach.

Expand internationally - $239B of the $300B market is international and they believe there’s massive opportunity for global expansion. They’ve launched in Canada but Brilliant Earth anticipates there’s massive potential in the rapidly growing Asian market.

Obviously, I anticipate on them focusing on their digital capabilities. From my research, I’ve noticed they’re one of the most innovative jewelry businesses on the market. In just my opinion, I think AR/VR can represent a massive opportunity in the longer term future. However, in this particular case their national expansion of show rooms from 14 to 100 stores clearly presents an immediate opportunity to scale their business quickly especially in conjunction with their new, “fine jewelry” segment. There’s a case here for exponential growth after a fresh round of a new cash injection post IPO.

Conclusion

Brilliant Earth is expected to IPO on September 22, 2021. Just a few days from this publication. I expect on purchasing a few shares but will watch price action on day 1 at first. I am not 100% sure how the market will take this IPO, I’ve been surprised before. With a reasonable valuation, my guess is that they’re going to do well and see a moderate multiple expansion right out of the gate. I do hope it still hovers around $1.4B. I can for-see the market initially pricing in the risk of competition but Brilliant Earth appears to be special and operationally executing on all fronts. There’s a strong case for hidden upside and this should yield excellent long term share holder returns for the investor patient enough to let the business execute on their growth strategy.

Up next, I plan on doing a publication on So-Fi where we’ll uncover the uniqueness of this super app and uncover all the components of their business. I am excited to share my research with all of you guys!

Remember, always, stay tuned… stay classy…

Dillon

what are the avg buying price for BRLT, RELY and FRSH if you dont mind sharing? I saw your twitter post but i cant DM you since need to follow me as well. This will be for learning purposes for future IPOs and how i should be thinking about it.