Portfolio Update: 1970's Fed Policy Applied to Today

Portfolio Update: 1970's Fed Policy Applied to Today

Fed Policy Evolves Over Time but Let's Apply Yesterday's Theory to Today

The other day, I had the opportunity to talk to one of the members in BluSuit’s Discord group and he brought up, “there’s a lot of news out there and a lot of bearish information but almost none of it is relevant to my portfolio.” This is something we all experience every day, as investors and traders. How do we know what news impacts our investments? In other words, how do we filter through the noise?

Russia/Ukraine War

European Gas Crisis

Inflation

Federal Reserve Tightening

Economic Recession

California Energy Crisis

China’s Debt Crisis and Real Estate Bubble

The list goes on and on, it doesn’t stop here. I am sure many of the readers today can list another 2-3 “crisis” in today’s macroeconomic environment that we “should be” paying attention to. The problem here, and the truth is, that, 90% of the things we read/hear about don’t impact our investment’s or our investing decisions. At the end of the day we are either investors looking to attach our wealth to an investment vehicle or traders looking to extract money from the financial markets.

*Partnership Update*

I am happy to announce that BluSuit has recently partnered with TradingView. By using our affiliate link (below), you can get $30 off a new annual subscription ($10 off a monthly subscription) through TradingView.

I use TradingView daily and it has always been my go-to platform for high quality charts and data. This partnership makes a lot of sense, is a good fit for the BluSuit brand and I am happy to look forward to what the future holds for our partnership.

*End*

Climbing the Wall of Worry

Dow Jones 1913 - Today

The Federal Reserve was formed in 1913 due to a series of banking crisis that happened over the last 100 years in the 1800’s and early 1900’s. During these periods, before central banking, there was a relatively common event called bank runs (I am sure you’re familiar with what that means). These crisis’s were typically fueled by a lack of liquidity in the banking system as the demand for dollars sky rocketed during periods of distrust in the banking system. Thus, the Federal Reserve, or Central Bank, was formed to provide liquidity to the financial system in times of need.

The problem here is that as time progressed, the Federal Reserve began playing a bigger and more important role in the economic/market cycle. After 1913, we had a few major cataclysmic events that fundamentally changed (evolved) the role the Federal Reserve plays.

World War I: 1914 - 1918, the Federal Reserve effectively financed the war by conducting a form of QE (or open market operations)

The Great Depression: 1929 - 1939, actually the lack of policy by the Fed is what led to the prolonged Great Depression. It wasn’t until the Federal Government began deficit spending, coupled with the Fed buying government debt, that created the environment to pull us out of the Great Depression

The 1940’s Hyper Inflation: A period of expansion in the America post World War II with many soldiers returning home and excessive government spending financed by the Fed from the war. In other words, the Fed created a ton of money and the U.S. government’s liabilities expanded rapidly.

The Great Inflation of the 1970’s: “Guns and Butter” a period where America entered into the Vietnam war and entered into a policy of, ‘do we feed our people, our troops, or both?’ U.S. government deficit spent on the war and various social policies which created a rapid growth in money supply.

1980’s - 1982 Fed induced recession: A period which Paul Volker raised rates to 20%+ to combat and kill inflation. This was the worst recession since the Great Depression where unemployment ran up to 10%+. This is what we will talk about today.

“Easy Money” Alan Greenspan 1987 - 2006: A period of great economic growth, low inflation, innovation and “easy money” where interest rates followed a secular decline.

2008 Global Financial Crisis aka “The Great Recession”: A collapse in the housing market and debt bubble that was fueled by decades of easy money policy. The Federal Reserve had to step in and pump massive amounts of liquidity into the financial system to prevent the second Great Depression.

2020 COVID Crisis: A global pandemic fueled monetary and fiscal response that spurred the highest rates of inflation since the 1970’s. We are currently writing Federal Reserve history today.

The Wall of Worry Made Simple, Narrowing on History as our Guide

The reason why I outlined many of these major events is that each played a fundamentally important role in today’s economic/market cycle and how today’s financial markets have evolved to become centrally planned. Do you notice how I stuck primarily with the Federal Reserve’s policy, inflation and response to inflation/deflation?

The only thing that matters in today’s economic and market environment is monetary and fiscal policy. If we discuss various events like Russia/Ukraine, Energy, Chinese Debt Bubble, etc. we (as investors) should maintain focus on what really matters and the question that controls the performance of our investments. “What is the Government and Federal Reserve going to do in response to xyz event?”

Beginning in World War I, the Federal Reserve has evolved to monetize both U.S. government and U.S. consumer debt. This has played a major role in how the economic and business cycle has been defined by relating it to the booms and busts of the credit cycle. Put simply, the Federal Reserve raises and lowers the cost of “credit” (debt) to expand and contract economic activity.

This directly impacts our businesses, the performance of those businesses and the macro economic environment as a whole. If our investments have:

Cyclically sensitive products/services

Highly leveraged balance sheet

Liquidity issues

Cash burning operations, etc

It directly impacts the price action of our investments and the risk appetite other investors have toward them. So let’s focus back on the key question we were asking:

“How do we know what news impacts our investments?”

It’s the Federal Reserve, Monetary and Fiscal Policy that impacts the short/medium term direction to our investments. They control the risk investors take, the economic growth/contraction and liquidity available in the system to allocate to our various investment vehicles.

Paul Volker, Jerome Powell and What Changed During Jackson Hole

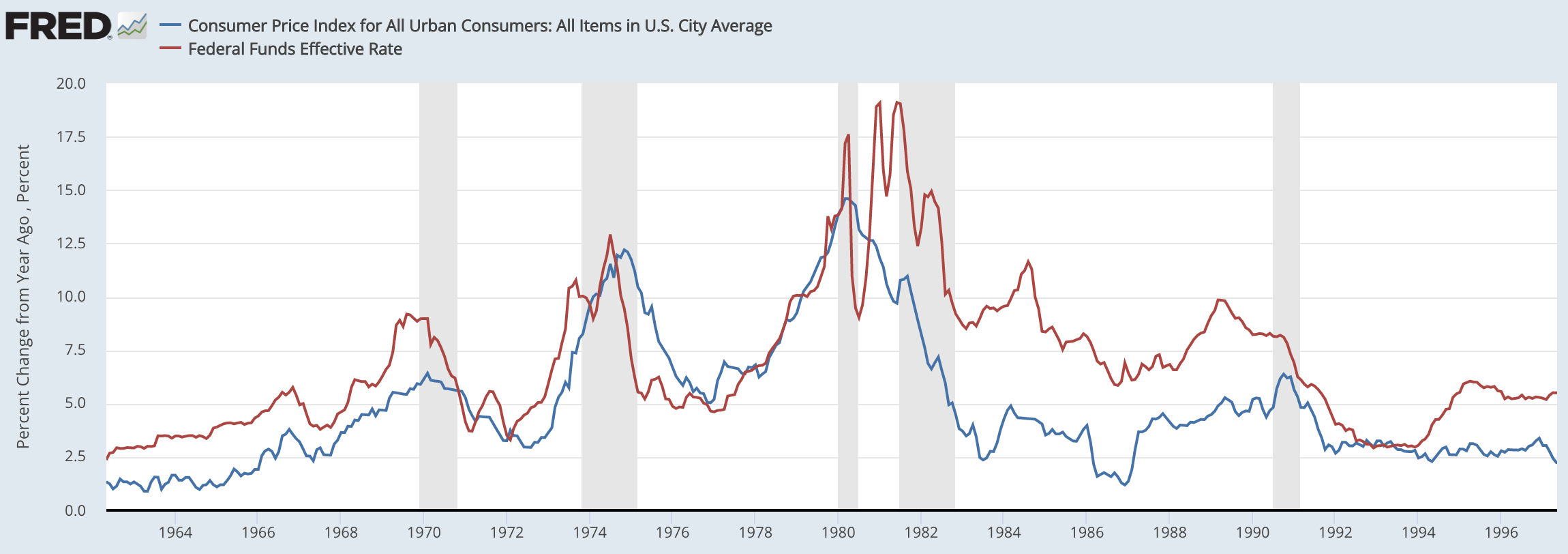

The time period we can best learn from today is is the late 1970’s and early 1980’s, when Paul Volker took the Fed Chair position. At the time, Jimmy Carter was the U.S. President and he nominated Volker for one mission and one mission alone, get inflation under control. He was the man for the job.

The theory that Paul Volker had was that the stickiest part of inflation was not inflation itself. Inflation structurally should cool off over time, especially if you promoted an economic recession or slowed money growth. By referencing Milton Friedman:

If inflation is only a monetary phenomenon; then monetary policy or fiscal policy should correct it. Historically this was not the case in the 1970’s as the Federal Reserve provoked a series of recessions beginning in 1969 and finally ending in 1983. Looping back to Paul Volker, recall how I mentioned that Volker’s theory on the stickiness of inflation is not structurally inflation itself.

It wasn’t until a devastating recession began in the 1980’s that sent unemployment sky high, all the way up to 11%, that inflation finally came down and stayed down. The thinking here from Volker was that inflation needed to be CRUSHED by tight financial conditions by raising interest rates to nearly 25% at one point. What made this policy unique was that he didn’t just think monetary policy needed to be tight, he led with the philosophy that it needed to stay tight as to crush the expectations of inflation.

Jerome Powell Crushed Inflation Expectation’s by Crushing Hopes of a Fed Pivot

Often you will hear Jerome Powell talking about the expectations of inflation “being anchored”. These expectations are exactly why he came out so hawkish, and aggressive, directly stating that he may need to raise rates even higher and keep them there (just like Volker did) to crush inflation. If we are going to compare Jerome Powell to Volker, or during the 1970’s, we should look at exactly how far the Federal Reserve is willing to go to crush inflation if they feel like it’s enemy number 1.

Paul Volker served as the Fed Chairman from 1979 - 1987, where the stock market actually went up during that time! Included in this time period (1980 - 1982) was the second to worse recession (at the time) since the Great Depression.

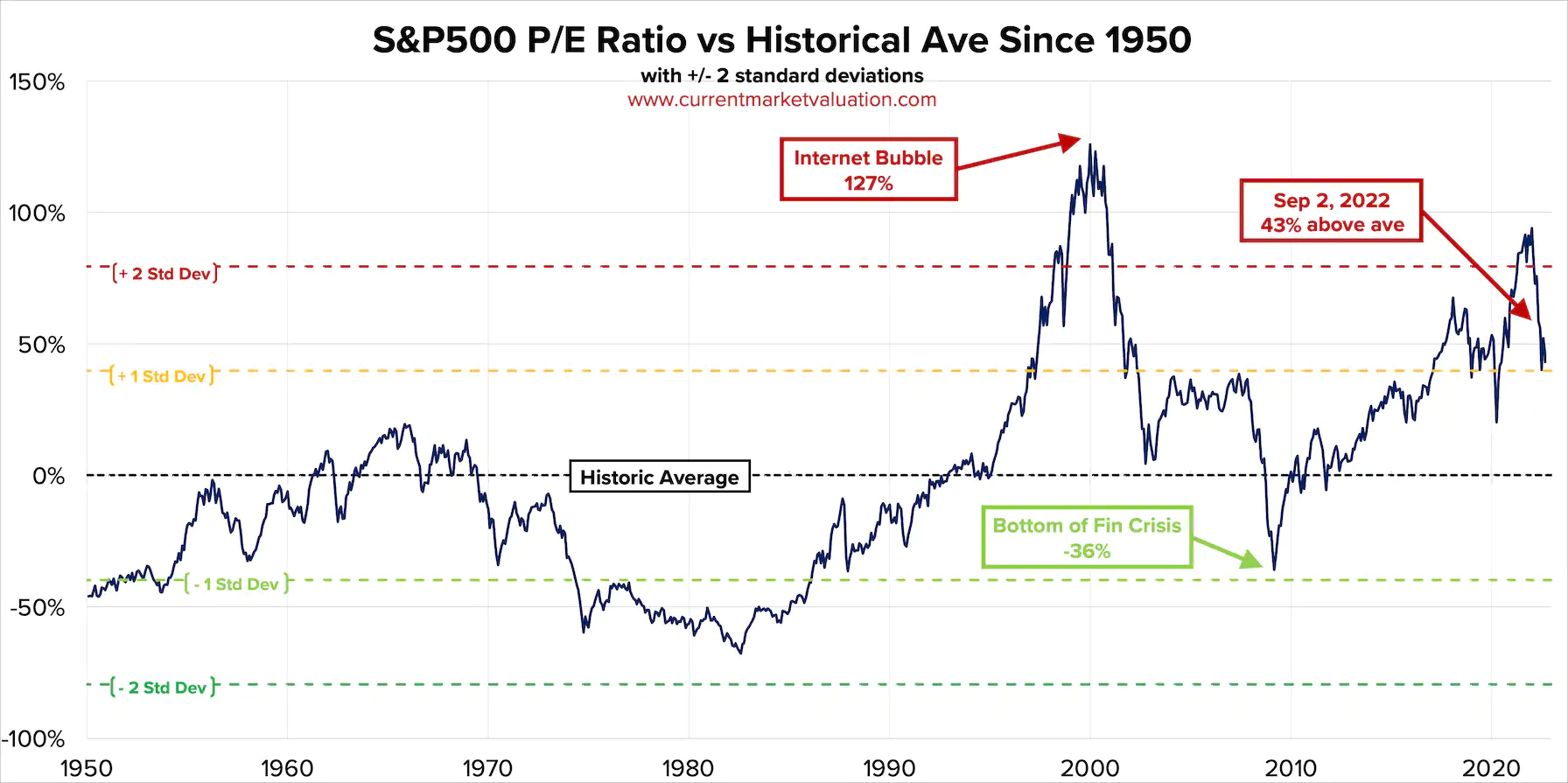

Looking at the chart above, we notice that the time period that truly crushed investor returns the most was the recession lasting from 1973 - 1974. The reason why the returns were terrible during this period had to do with the starting valuation of corporate equities compared to Volkers time. Today, we can see that we have extremely high valuations on a historical basis.

Jackson Hole was the Beginning to Pricing in a Meaningful Economic Recession

Jerome Powell came out and basically said, “inflation is enemy number 1”, and even mentioned, “house hold pain”. This idea of “pain” was something I have never heard (or been aware of) a Fed Chairman say since the Fed was so set on combating inflation in the late 1970’s/1980’s. During this time, we can see that the historical P/E ratio was nearly 2 standard deviations below the historical mean. Basically, during Volker’s time, the stock market was already cheap and businesses can only get so cheap considering they are productive assets. Today is different because today, stocks are still historically expensive.

This is What We Know, Don’t Know and What We Can Do

Here’s the thing, we can look back into time to learn certain lessons of the past and apply them today but they are not always perfect remnants of what will happen. As the saying goes, “history rarely repeats itself but it often rhymes”. What we can do is identify how this, inflation, rhymes with the past and apply past stock price action to today’s portfolio strategy by adding and subtracting certain variables. In this case, let’s break it down.

What We Do Know:

Inflation likely sparked (once again) by excessive government spending and easy monetary policy

CPI is currently 8.5% but projected to continue coming down

A recession, by technical terms, is already here (two quarters of negative GDP) and we are not out of the woods yet

COVID pandemic and economic disruption is the catalyst that sparked the response from governments and central banks

This last earnings season (released from businesses) was not terrible but not great. There is definitely weakness.

What We Do Not Know:

For the past 10+ years, since 2008, we have been in a deflationary environment. What is secular and what is cyclical? Meaning, is inflation a secular or cyclical component to our economy today?

How much did the COVID lock downs and supply side constraints influence inflation?

Has inflation really peaked?

Jerome Powell is not Volker, how much economic pain is Jerome Powell willing to put us through? His reputation, legacy, and how he is written about is everything to him.

There are no history books for how an economy behaves post a once in a one hundred year pandemic, followed by an unprecedented liquidity event and stock market bubble. History, in this case, truly does rhyme in many ways but it’s not identical. There is a strong scenario here where we actually have hit peak inflation and COVID acted more as a cyclical shock to an ongoing secular deflationary economy.

I do hope we are still in the middle of a secular bull market but don’t know if this is the beginning of a secular bear.

In my opinion, these questions are better left to the history books. I am thinking as a portfolio manager, as I assume many of you are as well. The question becomes, what can we do about the circumstance we are faced with?

What We Can Do

2018 - 2020 sparked a new kind of investor and I don’t believe this is bubble talk. What I am talking about is a structural, innovative, shift in the financial markets as a whole. We have witnessed the rise to the retail investor and many individual investors have access to data that professional fund managers do on Wall Street. Heck, I follow about 5 Ex-Wall Street gone Main Street Investors.

1.) We, as investors and traders, get better and learn faster

If you don’t know macroeconomics, we have to learn it. Read this Newsletter (and many others) that keep their investor base in the loop.

If you don’t know technical and fundamental analysis, it’s very important to know. There are many folks online willing to do this for free, just to help, that post their charts and strategies for free.

A few recommendations and Twitter follows:

@FiredUpWealth - Business Fundamentals

@MacroAlf - Macroeconomics

@PatternProfits - 20+ Year Technical Trader

@Saxena_Puru - Trend Following, Trading, and Secular Growth Stocks

@DavidWooUnbound - Political and Macro Environment Analysis

Richard Duncan - No Twitter but put his name in YouTube, he is there. He’s a Macro Economist.

This is a small list, there are so many other great follows out there.

2.) We listen to the Federal Reserve policy and position our portfolio’s appropriately

Listening to Jerome Powell and other Fed members is valuable in its own sense. We need to let the central planners, plan, and we maximize our opportunities where we have them. One day the pivot will come and we want to be positioned to capture it.

3.) Not hold our selves back as investors, as traders, by bucketing ourselves into only one camp but still knowing the game you are playing.

I have found portfolio managers that incorporate all three aspects of money management:

Technical Analysis

Macro Trading

Fundamental Analysis

Perform better. I have noticed that they do the fundamental analysis to take advantage of good businesses at cheap prices but initiate trades around their portfolio using technicals analysis while being aware of the Macro just seem to “get it” more. It is important to understand the game you are playing but continue to grow and evolve as a portfolio manager.

What I am Doing and My Short/Long Strategy

This is the section I keep exclusively for members as a way to gain additional insight into what I (alone) am doing. I don’t have my series 65 (yet) and the best advice I can give is only by sharing what I am doing to give investors something to think about. I document every trade, and my performance, every week.

My Portfolio Strategy

Keep reading with a 7-day free trial

Subscribe to BluSuit to keep reading this post and get 7 days of free access to the full post archives.