Portfolio Update: Am I Wrong?

Portfolio Update: Am I Wrong?

FOMC This Week, Market Expectations and Macro Picture

Everything, and everybody, is saying we are heading lower despite my call for June marking the lows to this bear market. Last week, after the inflation reading, I received many tweets making sure to emphasize that Core CPI was too sticky and that we were heading lower. Just by looking at technicals alone, it seems fairly obvious that they are right. Or, at least, that they should end up right.

In response, I took a short trade (I quickly covered with a .5% loss) to prepare and protect downside that could come from another leg lower. This reminds me of the time where I called for the market to crash in November and I decided not to hedge despite having my personal conviction leaning in a different way. I should have listened to my own conviction but the noise was strong. Regardless, I have learned some of the most important lessons I could have learned the past few months.

There is nothing about the past few years of market price action that can lead us to call it “normal” but no experience more humbling than the market top in November. It has changed my entire investment philosophy and stock picking process. More importantly, it changed the way I view the market and what determines the price action. It changed the way I view consensus.

A recent BofA fund manager survey showed that portfolio managers are more underweight equities that the credit collapse in 2008. This is a data point that we cannot ignore because this tells us something very important, many have already sold their positions based on Macro fears. In addition, the infamous put/call ratio, a notorious contrarian indicator, flashed a bottom signal as portfolio’s hedge for another leg down.

I understand the Macro fears, I really do. The market has every reason in the world to justify another leg down:

A Global Recession

Soaring, sticky inflation, with core CPI not slowing down

Federal Reserve raising rates to astronomical levels. You have to go back to pre global financial crisis to see the 2 year yield this high.

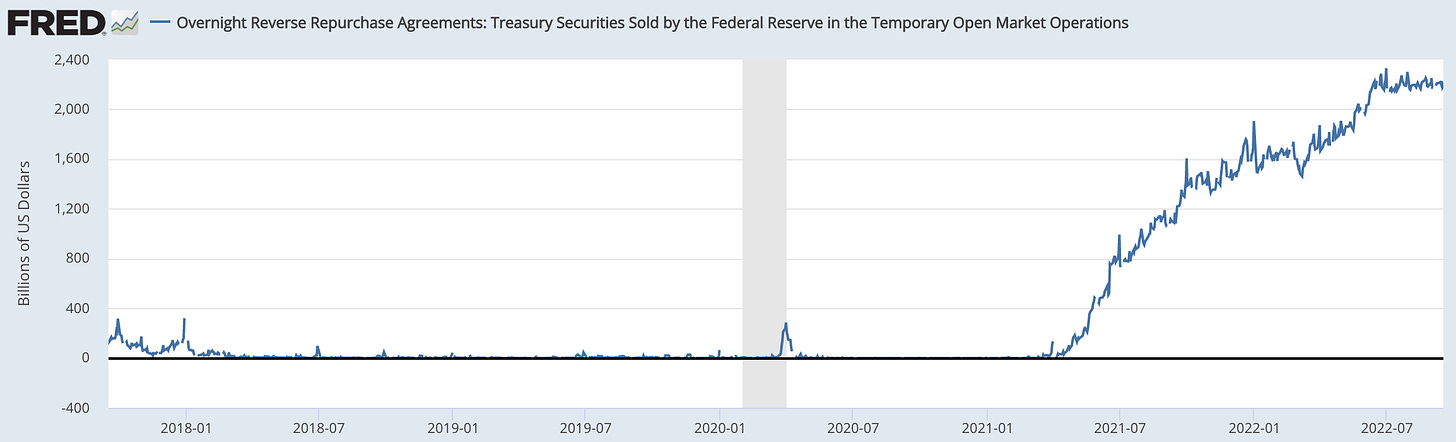

Quantitative Tightening (I will explain at a later date why this is a massive miss among narrative). We shouldn’t be concerned here till reverse repo market falls further.

Market Expectations are Unanimous

As I mentioned above, I become fearful about aligning my views with consensus.

The best way to view consensus opinion: Let’s say we have 100 portfolio managers in a room and we all ask them, “what do you think about macro and how are you positioning your portfolio?” Based on today’s assumptions (figuratively) we could assume that 70% of the portfolio managers are positioned defensively and 30% are positioned aggressively. 70% of these managers believe the global macro will deteriorate and corporate earnings will be terrible. The other 30% believe that earnings are staying strong and that inflation will fall under control.

In our example above, we can assume that the majority (70%) are positioned short/hedged or just in cash. But, the markets are still trading at stable prices from lows made in June. How are you going to convince the other 30% to join the other 70% because it’s necessary to have more sellers than buyers in a market. Obviously this is a very rough example but the point is all the same. In a market, you have a given amount of buyers and a given amount of sellers at any point in time. When the majority have already sold, or already bought, the opposite is typically what happens. It’s basically human behavior.

The Vast Majority IS BEARISH

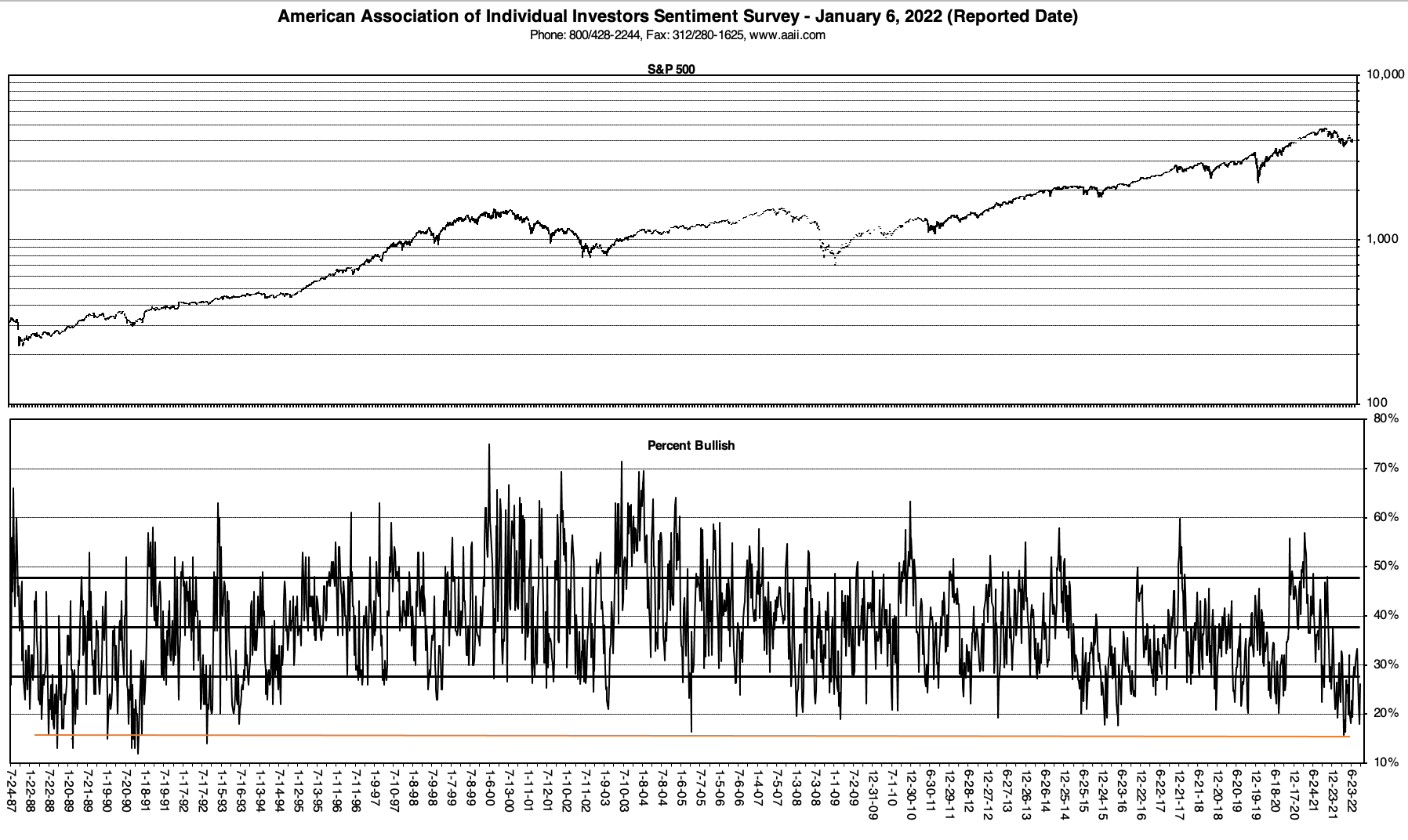

Over the past few years we have seen incredible market swings from COVID low to February 2021 with the high the markets experienced. In February and November of 2021, both situations had unanimous consensus that everything would keep going up forever. Analysts where revising earnings upward (see below) and extreme bullish calls on a market with a forward P/E of 23x this year were a daily occurrence, S&P 5000 was the consensus call. They couldn’t be more wrong. The Federal Reserve was no exception to this commentary with “transitory inflation” being a regular occurrence.

Today, the opposite is true. We now have analysis revising earnings downward as future earnings expectations dwindle. If you notice that the downward earnings revision in previous market cycles marked major market lows. When putting hard data on sentiment, the AAII investor sentiment survey shows us the clear picture.

It’s Not Just Sentiment, it’s the Rate Hike Expectations

This is, perhaps, the most confusing aspect to all of this. Has anyone picked up on how the market has NOT undercut lows despite both the 2 year yield and 5 year yield marching higher? Here’s the 2 year yield again:

The 5 year

The 10 year yield shows a similar story.

On my previous Newsletter I mentioned that the market moves down for 2 years:

A move downward on the equity risk premium

A revision downward on earnings

The confusing market of this to me is that the S&P, as well as the NASDAQ, have yet to undercut lows despite everything working against the major indices? It may be too early to tell but it would appear that a majority of the macro today has been priced in. The only reason why I say this is that the equity risk premium should ideally be lower than June due to yields being higher and earnings revision moving downward.

FOMC is This Week and We Are Priced for a Terrible Outcome

The economy is deteriorating, fast. Housing is slowing and consumer purchasing is slowing. Commodities are rolling over and every leading indicator to inflation is showing a downward trend while the Federal Funds Rate is 2.25% - 2.5%. Now, the markets are pricing in for another 200 basis points of hikes over the next three months?!

September expectations is .75bps

By December the market is pricing in 200 bps as “likely”

It Took the Fed to Raise Rates to 2.25 FFR Over the Course of 6 Months. The Markets are Now Pricing in 2.00 more in Basis Points as Inflation is Slowing and a deteriorating Economy in HALF (3 months) the Time!

At some point we gotta ask ourselves what is realistic and what is peak hawkish expectations. To me, this seems extremely unrealistic and seems to be a major peak in expectations while inflation IS going down. I’d understand if inflation wasn’t slowing, but it is, despite core showing to be relatively sticky.

According to Volker’s philosophy he raised rates to restrictive territory and kept it there. Jerome Powell is attempting to treat the 1970’s inflation like that of today. We have to ask ourselves, as investors and traders….

If the Federal Reserve Goes too Far, they Risk Needing to do QE Again (while cutting rates) to Bail Us Out of Deflation

Our economy is structurally different and if inflation begins to melt, unemployment rises, and deflation becomes the theme, the Federal Reserve will have to pivot HARD. It seems crazy to me that the Markets are pushing the Fed to do more, and more, and more till something breaks. The FOMC would be smart to keep raising but not at the consequence of doing QE again, this would defeat the entire purpose.

Add in a stimulus happy Federal Government, we would see the cycle of inflation begin again. We cannot let this happen. Deflation can’t be the solution for inflation and inflation cannot be the solution for deflation.

If Jerome Powell Doesn’t Come Out and Hike 100 BPS, the Market Will Rally

Let’s take a look at what the market has done after every Fed meeting this year. Every Fed meeting is marked by a black line.

After every single meeting this year, the market has rallied except during May’s meeting. I can’t help but believe this time will be any different as we head into FOMC with extreme hawkish expectations, consensus hedges and equity positioning lower than the Global Financial Crisis among fund managers.

I am Taking a Different Approach With My Portfolio and Maintain Focus

Let’s take a look at how I am positioned.

Keep reading with a 7-day free trial

Subscribe to BluSuit to keep reading this post and get 7 days of free access to the full post archives.