Portfolio Update: Explaining Inflation

Portfolio Update: Explaining Inflation

Inflation: Where it came from and what it means for your portfolio

Economics typically works with theory. By theory, I mean we can only theorize what happens over here when we pull xyz lever. Typically, from there, the data and numbers drive the cause and effect relationship that happens in both the macro economy as well as the effects in the banking system. Eventually, this all trickles down to your portfolio, your portfolio performance and how you manage it.

This weeks NewsLetter will be centered around inflation, why it came now rather than for the past 10 - 15 years, as well as where I am at with my portfolio construction. As a 31 year old, my focus is on building a retirement portfolio and I share my every move. Today, I will be discussing where I am at today as well as how I plan to build it in the coming years. Specifically focusing on the long term balance I seek for my investments through various phases of life.

Members have access to my macro/micro research, portfolio construction strategy and the Discord Group where they have access to other like minded investors to collaborate and strategize as well.

The format this week will be as follows:

Inflation, where it came from and how central banking impacted this

My portfolio, the recent out performance and what I am going to be focused on next (ETF integration)

The Economics Behind Inflation

I went to school for Business after I was done with active duty service in the U.S. Marine Corps. Since then, I quickly picked up that many of the “finance teachers” in the education system do not fully understand/conceptualize the topics they are teaching. Particularly when it comes to economics, financial and business theory. When we look around, there are few economists in the world that truly grasp the mechanics behind the economic engine and how the central bank influences macroeconomic/market forces. Milton Friedman was not a teacher, but a student of economics.

Milton Friedman is a renowned American economist who won the 1976 Nobel Memorial Prize in Economic Sciences. As of recent, I have constantly had his teachings ringing through my head every time someone mentions the cause/effect of todays inflation. Truly, everyone is wondering and speculating the causes of why we could possibly have inflation after 14 years without it. What have we heard so far?

“Putin’s price hike”

Supply chain challenges

Labor shortages

Demand shock, etc

The narrative behind the causes of inflation have included everything but the actual root cause in the first place.

Key Terms to Know:

Quantitative Easing (QE) - the act of the Federal Reserve (American Central Bank) buying U.S. Government Treasuries and Mortgage Backed Securities (home loans)

Quantitative Tightening (QT) - the act of the Federal Reserve decreasing its ownership of treasuries or MBS’s (mortgage backed security)

Monetary Policy - The Federal Reserve set policy on interest rates and market forces

Fiscal Policy - The U.S. government, both Congress and Executive branch, set policy on taxes and spending

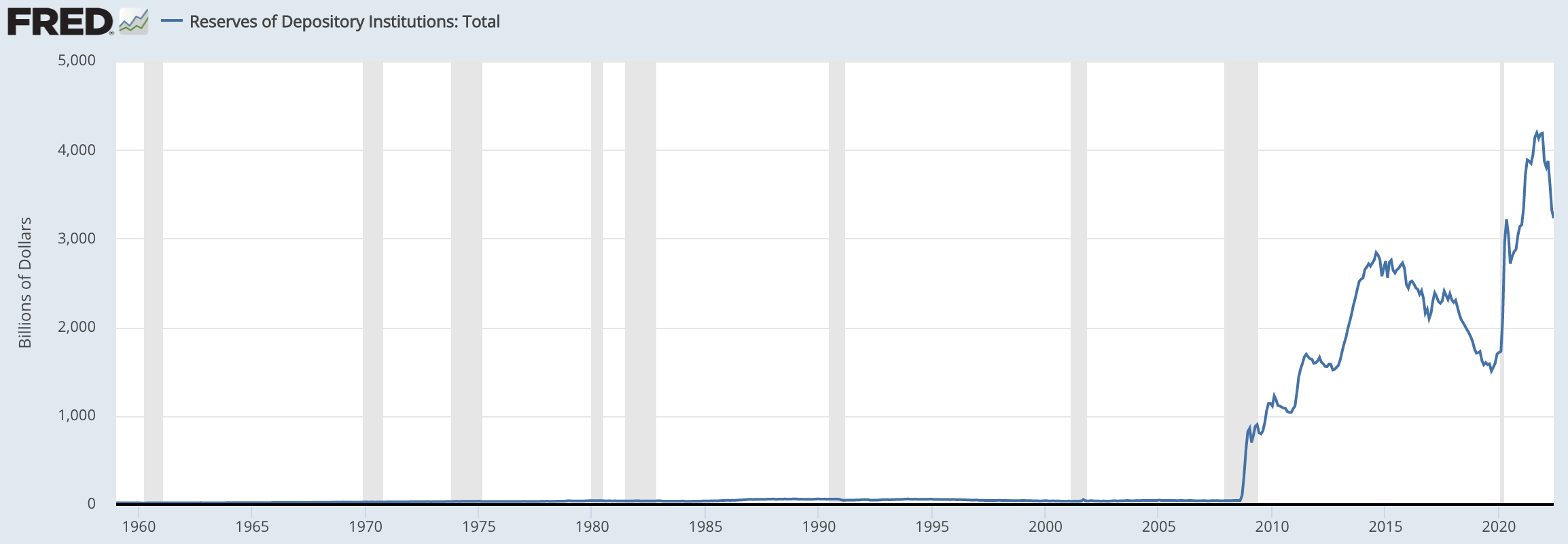

We Have Conducted QE 4 Times Since 2008, Only One of Those Times Created Inflation… Why?

I made this chart a few months ago to show the cause of QE on the financial markets. Knowing that QE pushes asset prices up is a key party to understanding what I am going to discuss.

Back in 1929, we witnessed the beginning of the Great Depression in the form of a bursting stock market bubble. However, it wasn’t the stock market bubble itself that created the Great Depression, it was the collapse of the banking system that created this bust.

See, what happened in the 1920’s was rampant speculation on the future of America. We even had a term for it called “The Roaring 20’s”. It was a time of rebirth of the American Economy and a cultural revolution. The idea was that “American business would remain dominant on a global scale for years in the future”.

What Americans did during this rampant period of speculation was actually take debt out (margin) that bet on stocks going up. The bursting of the bubble created a rapid devaluation of U.S. stock market asset prices. When the asset prices declined, Americans were forced to pay back their margined out loans, but, there was a problem. Americans borrowed money against collateral like their homes, stocks and other assets.

Collateral is an asset that can be used to borrow against. Your home is collateral, treasury bills are collateral and so are your stocks (even today).

When the rapid devaluation of all assets began (in 1929), people needed to sell more of their assets to pay back their debts. This created a cascading effect where Americans needed to sell more, and more, of their assets to pay back their debt. However, there is a point where their assets have devalued so much that they couldn’t pay back their loans. What happens when people can’t pay back their loans?

What I am talking about right now is called a credit super cycle, it’s essentially the unwind of debt within a financial system. When debt begins to unwind, what’s actually happening within the system is that banks are losing large amounts of money.

In the case of the 1930’s, banks lost so much money that they need to suddenly close their doors because they went out of business! When large quantities of banks go out of business (like in the 1930’s), this created the infamous term of a bank run.

A bank run is when people literally run to the bank to try to pull their money out of the bank before it goes out of business.

Bank runs create a problem that fuels a vicious cycle. It fundamentally creates distrust within a financial system which cascades to a stall economic activity. Think of it like this:

What happens if someone needs a loan for a home?

What if businesses need a loan?

What if someone just needs to borrow money in general to buy anything from their vehicle to just “stretching out” their payments?

Credit (the access to borrowed money) is fundamentally what drives nearly all economic activity. Sure, we can think to ourselves that credit is to blame for two catastrophic economic cycles but it also allows everyone to buy their homes, their cars or for businesses to fuel future activity. Debt, or credit, can quite literally be used as an investment as long as the return exceeds the interest. If credit availability comes to a halt, economic activity nearly ceases to exist.

When people began to default, banks went out of business which led to a fear people would lose their entire life savings. In many cases, people did lose their entire life savings because banks did not have enough liquidity available to pay everyone back. Let me stop here because this is precisely the point I am trying to make here, it’s the banking systems lack of liquidity that created the 1930’s Great Depression. If people didn’t run on the banks or if people didn’t borrow against their homes/stocks to buy more stocks then the Great Depression would have never happened.

QE Explained - In an Easy to Understand Way

The Federal Reserve plays a very important role within our economic system. They are designed to create stability from the very natural cycles that exist within traditional capitalism. The reason why they were made in the first place (formed in 1913) was as a result of multiple banking crisis and severe economic downturns that occurred in the 1800’s. One could argue that in the 1930’s they didn’t do their job as “free markets” were the hard held philosophy.

Nearly 80 years later, the 2008 global financial crisis resembled a very, very, very scary resemblance of the 1929 stock market bust. Except this time, it existed within the housing market. Same exact concept, two different asset classes. People once again borrowed against collateral in the anticipation that the asset price would forever go up and never down. The Global Financial Crisis was the beginning to the next credit super cycle. It was supposed to be the next Great Depression.

The Federal Reserve Knew They Needed to Do Something

Looking back, central banks and policy makers had the historical framework and economic history to know exactly what to do this time around. They needed to flood the banking system with a shit ton of liquidity to prevent another banking run that could evaporating the nations money supply and the Federal Government needed to effectively patch the financial black hole of the evaporated money supply that came in the form of defaulting mortgages.

When loans default, that money effectively disappears from the financial system.

Let me introduce you to Bank Reserves. Bank Reserves are essentially an account that Federal Reserve Banks (think JP Morgan, Citi, Wells Fargo, Morgan Stanley, etc) keep at the Fed. The purpose of these bank reserves are to act as liquidity to eventually lend out or give to the American population if hard cash is in demand. In other words, the more bank reserves a system has the more liquidity it has. If a bank run happens again nothing will happen to the functioning of the banking system this time around. There will be enough liquidity.

Bank Reserves are also important for transactions among other central banks, the repo markets, and the treasury market. More on this at a later date.

Above, you can see the chart of bank reserves since the 1950’s. Do you notice how in 2008 we see a massive move up in the total reserves? This was by design, it was created through quantitative easing.

Quantitative Easing is the Federal Reserve Buying Debt

When the Federal Reserve goes on the open market, typically they are buying U.S. treasury bills. For those who aren’t 100% familiar with T-bills, they are little I-owe-you’s from the Federal Government that say they will pay you xyz amount for a specific interest rate. The Federal Reserve, or U.S. central bank, will quite literally go onto the open market and force Federal Reserve Banks, like JP Morgan, to sell them their treasury bills in the form of bank reserves.

This means that banks no longer carry U.S. treasury bills, they now carry bank reserves which is excess liquidity stored at the Federal Reserve. This creates a cascading effect through the financial markets that pushes the prices of all asset prices up (including real estate and stocks).

Let’s Go Back to Inflation, Does QE (Federal Reserve) Create Inflation?

Let’s go full circle here. All the information above was necessary to make a very important point. As Milton Friedman ended up saying:

Quantitative Easing Only Increases the Amount of Liquidity AVAILABLE for the Banking System

Full stop…

I gotta emphasize this point. Quantitative easing ONLY increases the amount of liquidity in THE BANKING SYSTEM. The quantity of money available in the banking system is NOT the usable money in the economy. That means that you (the reader) and I do not have access to Bank Reserves. In fact, those bank reserves do absolutely nothing 90% of the time. They just sit there. It’s money that is waiting to be used. Money that is waiting to be used is not inflationary.

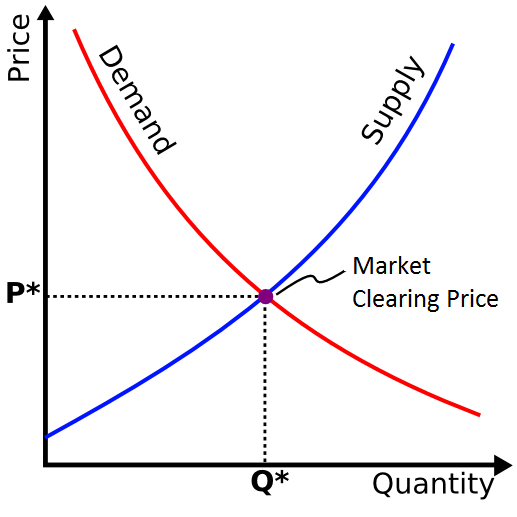

What Milton Friedman mentions is that “inflation can only be produced by a more rapid increase in the quantity of money than in output”. Above, I included the supply/demand chart that is the core too nearly all economic theory. Supply and demand always meets equilibrium in all aspects of the economy. If you rapidly increase the supply, price goes up. If you increase the supply of dollars (blue line) and keep demand the same (red line) the blue line moves upward which increases price.

Inflation is simply the rising prices of goods, assets and services.

Dillon is Out of His Damn Mind, He Just Said QE is NOT Inflationary Because it Doesn’t Increase Money Supply

This is true. QE does NOT increase money supply. It does, however, increase the prices of assets but it does not influence the prices of goods and services because it’s not actually producing usable money that’s in circulation in the economy. Does anyone remember what the purpose of bank reserves are?

“The purpose of these bank reserves are to act as liquidity to eventually lend out or give to the American population”

QE is the purchase of debt. More specifically, government debt. Debt is the creation of money.

Debt, or Credit, is the Creation of Money

This topic of money creation in itself justify’s a whole independent publication. I am going to focus primarily on inflation here, get to the point and emphasize two factors of money creation that are important to lead to my ultimate point.

Money that banks lend out create a compounding effect

The U.S. Government creates money through deficit spending

Low Interest Rates Create Inflation

This is the slowest way of money creation because it requires two pieces of the equation, supply and demand (as always). What I mean primarily by this is that when you go to the bank and you get a loan from them to buy a house you are actually participating in the money creation effect. This is how it works.

Let’s say you want to go to a bank, you need $400k for a home

What people don’t know is that $400,000 the bank lent to you actually didn’t exist before. I can go significantly more in depth here to explain the inner workings of the banking system but the topic here is the inflationary component. The key purpose here is that money is newly created and it goes into the economy to spend. This money goes to multiple different industries.

All of these industries above and many more not mentioned are dependent on you, the borrower, to agree to purchase the home in the first place. Imagine the amount of jobs created just by the real estate industry alone. All of this is dependent on the amount of money people are willing to take out, based on their monthly payment, that is 100% dependent on the interest rate of that loan. Let’s do some rough math, we are buying that $400,000 home at 3% vs 6% on a 30 year fixed rate. What’s the monthly payment?

3% interest monthly payment is $1,686 per month on a 30 year fixed

6% interest monthly payment is $2,398 per month on a 30 year fixed

The value of the home is exactly the same, $400,000, but it’s the cost to borrow that has changed. In this case it’s about $700 more a month just because interest rates fluctuated.

When the Federal Reserve lowers interest rates, this incentivizes borrowing. The increased borrowing picks up economic activity, which leads to more money in circulation, which leads to an increase in inflationary pressures.

Everything up until this point has been crucial to understand to finally get to the point of inflation and why we have it now.

The U.S. Federal Government’s Excessive Need to Spend is, and has Always Been, the X-Factor to Inflation.

In many cases I have come to realize that, for some reason, this topic often offends people. Politics, in many cases, is the root of all poor decision making. Often times the “popular” thing to do in the eyes of society is the wrong thing to do in the long run. What I am talking about specifically was the U.S. governments response to the COVID-19 pandemic.

I will be as unbiased as possible and only explain the economics behind the response. I am not debating on what was right, what was wrong, or what we should have done. I am only explaining why we are experiencing inflation now.

The Federal Reserve’s QE Program vs U.S. Government Borrowing

Remember, QE is only the act of exchanging U.S. treasuries for bank reserves with Federal Reserve banks like JP Morgan, US Bank, Citi, or Wells Fargo. The actual act of money creation is derived from borrowing, credit creation, or lending. So what happens when the U.S. Government borrows money? There were two major stimulus programs during the COVID-19 pandemic:

$2T COVID-19 relief and economic package

$1.9T American Rescue Plan

Let’s recall the example above where we talked about what happened when you or I borrow $400,000 to build our home.

This created money cascades through the economy and boosts economic productivity. Typically, this form of money creation is slower but there is a much more aggressive way to stimulate economic activity. During periods of geopolitical or economic turmoil, you create a wave of liquidity that acts like a tidal wave sweeping through the economy.

There were FOUR other instances before the COVID-19 pandemic that the U.S. Government did this, three times of which created inflation for the following years:

World War I - Inflation from 1916 - 1920

World War II - Pulled us out of the Great Depression but created an inflationary decade till the 1950’s

Vietnam War - “Guns and Butter” the U.S. Government spent too much to support the war

2008 Global Financial Crisis - The infamous Wall Street bailout

3 of those instances, during war periods, created years of inflation that followed. Let me emphasize that I do understand the oil crisis of the 1970’s that many people pin on inflation. While yes, I do agree this likely played some role, we are sticking to the core philosophy that Milton Friedman mentioned. Posted above but as a reminder:

It’s not just U.S. economic history that supports this. It is hundreds of years, thousands of years, even dating back to the Roman Empire that supports a governments insatiable appetite for spending being the root cause of inflation.

Why 2008 Was Different

2008 is an anomaly in the sense that the government printed money but did not create an inflationary decade. Most other periods for hundreds, thousands, of years where the government printed large amounts of money it resulted in inflation. You ask yourself, what was it about 2008 that was different?

2008 was different because we were experiencing a severe deflationary event where money was being defaulted on, destroyed, vanishing from existence through the collapse of the U.S. housing market.

Just like in 1929, money disappeared and vanished. That’s hard to think about because in most cases people think of money as a piece of paper you walk down to the store to use in exchange for some milk and cookies. However, let’s pull up the example I used above where I mentioned that when you borrow $400,000 from the bank it didn’t actually exist before.

During the 1930’s when credit was disappearing, or in 2008, people couldn’t pay their loans back. This means that the money that would have been in circulation going to all these different industries…

Vanishes over night, it disappears. The Real Estate agent no longer gets paid the invoice they issued. The furnishing companies don’t get their money back either, neither do the landscaping people. What this cycle does is that it creates a black hole in the economy.

The only way to fill that deflationary black hole is by having the Federal Reserve absorb the dead money and have the U.S. government shove liquidity in the system to absorb the deflationary shock. Basically, you put a bandaid on it, kick the can down the road and deal with it at a later time.

In Summary

The inflation that we experienced was a result of too much money being pumped into the economy. The government got it right in 2009 where the spent just enough and did just enough QE to patch the holes that existed in the U.S. economy. However…

The stimulus that was passed in 2020 & 2021 became politically, not economically, charged

A portion of it was certainly necessary. However, it has become clear that it was too much. Now we managed to increase our deficit by $5T+ and the only way out is to inflate our way out of the debt, likely leading to another decade of inflation.

This is a good topic for a later SubStack. Let’s get to the good stuff, what am I doing with my portfolio and what does this mean for assets? How do you protect your wealth?

My Portfolio Strategy

Keep reading with a 7-day free trial

Subscribe to BluSuit to keep reading this post and get 7 days of free access to the full post archives.