Portfolio Update: New Stock Pick & Planned Moves

Portfolio Update: New Stock Pick & Planned Moves

Sharing my research on this renewable energy stock & updating my portfolio

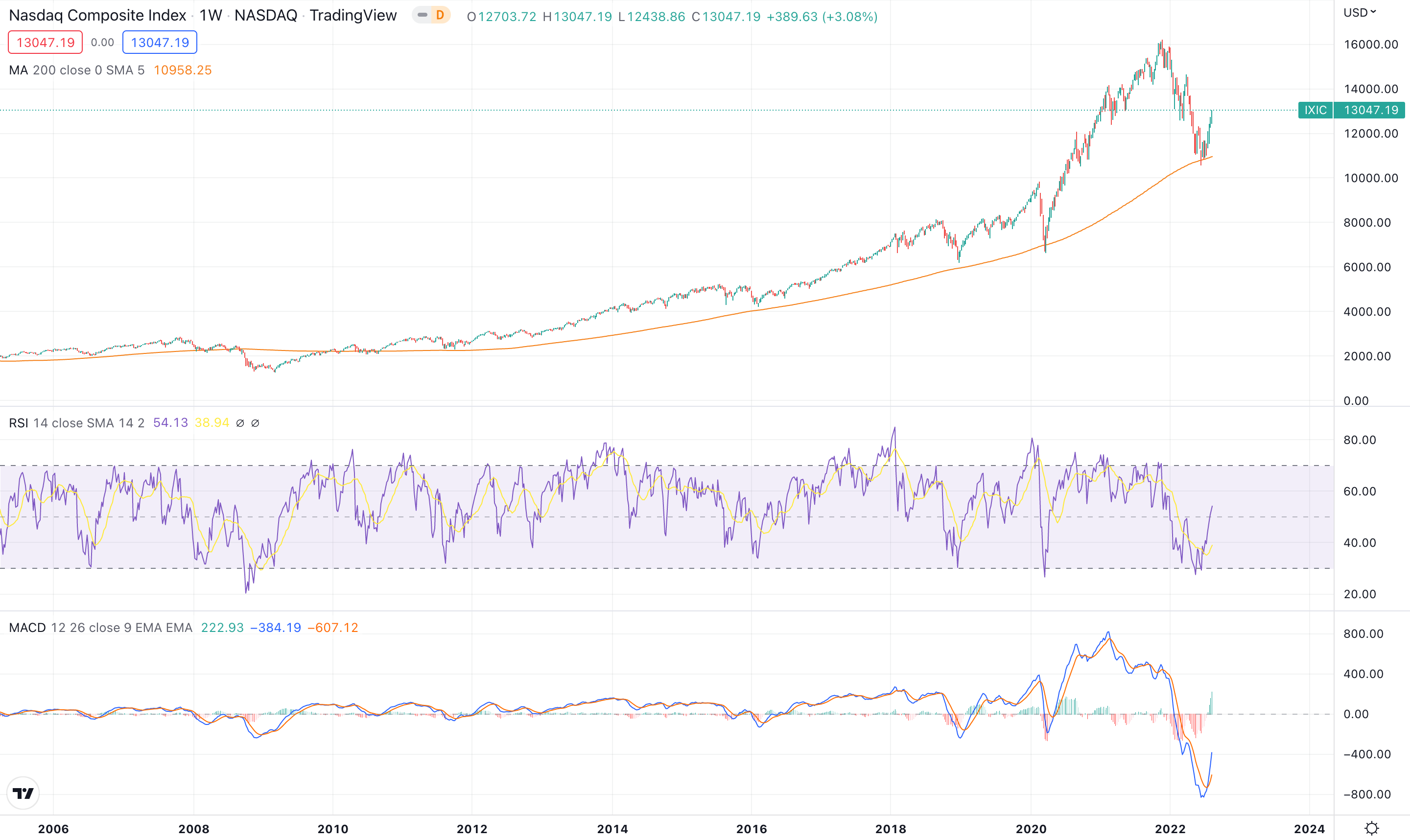

This last week was nothing short of exciting, I covered much of it here:

Inflation came in lower than expected, the markets continued their march higher and sentiment is beginning to shift. I have noticed that investors are seeking to understand a new narrative as to why the markets are marching higher. Readers of BluSuit’s Newsletter have been familiar with the narrative that is now becoming mainstream.

Markets are forward looking as they are beginning to price in a Federal Reserve pivot, or rate cuts (rather than hikes) for early 2023.

The real question now, is this sustainable? In my opinion, if I only looked at charts and didn’t think about Macro or fundamentals I would say that we are in the beginning of a new bull market that can go a lot higher and last longer than what people think. Time will tell for certain but the momentum is clear, it’s up and to the right.

My Latest Stock Pick is STEM

I have been following this business for a few years now, since 2020, when it was actually a SPAC. The way I look at the SPAC craze today, (that existed in the 2020/2021 bubble) I knew there were a lot of terrible company’s that would show their true colors. One specific example is Skillz who was not transparent about their business model regarding how they actually recorded revenue. From a more optimistic view, there were destined to be long term winners that would emerge much like the Tech and Telecom bubble in 1999.

STEM is a Renewable Energy Company

Exposure to the renewable energy space is a must. I promise you that you need to think about which business will fit this bill the best for you over the next 10 years. The reason why, just look at the “Inflation Reduction Act”. It is a bill that is focused on making renewable energy less expensive over fossil fuels. However, the thesis is not necessarily rooted in just one bill, this is global.

Countries all over the world are focused on making a shift to renewable, technology driven, energy solutions. Aside from STEM 0.00%↑ , another business I have talked about was Enphase ENPH 0.00%↑, which is worth looking at for exposure to this market. TSLA 0.00%↑ is also another "renewable energy" play, a business I own, that is likely the first of many energy companies to emerge as a major winner over this decade.

STEM’s Business Explained

Stem is current a $2.4B company, which is small and can offer massive upside if things go right. First rule of thumb when finding multi-baggers is to make sure they can actually double or triple. In this case, we are talking about STEM reaching to a $5B to $10B company. This is more than possible.

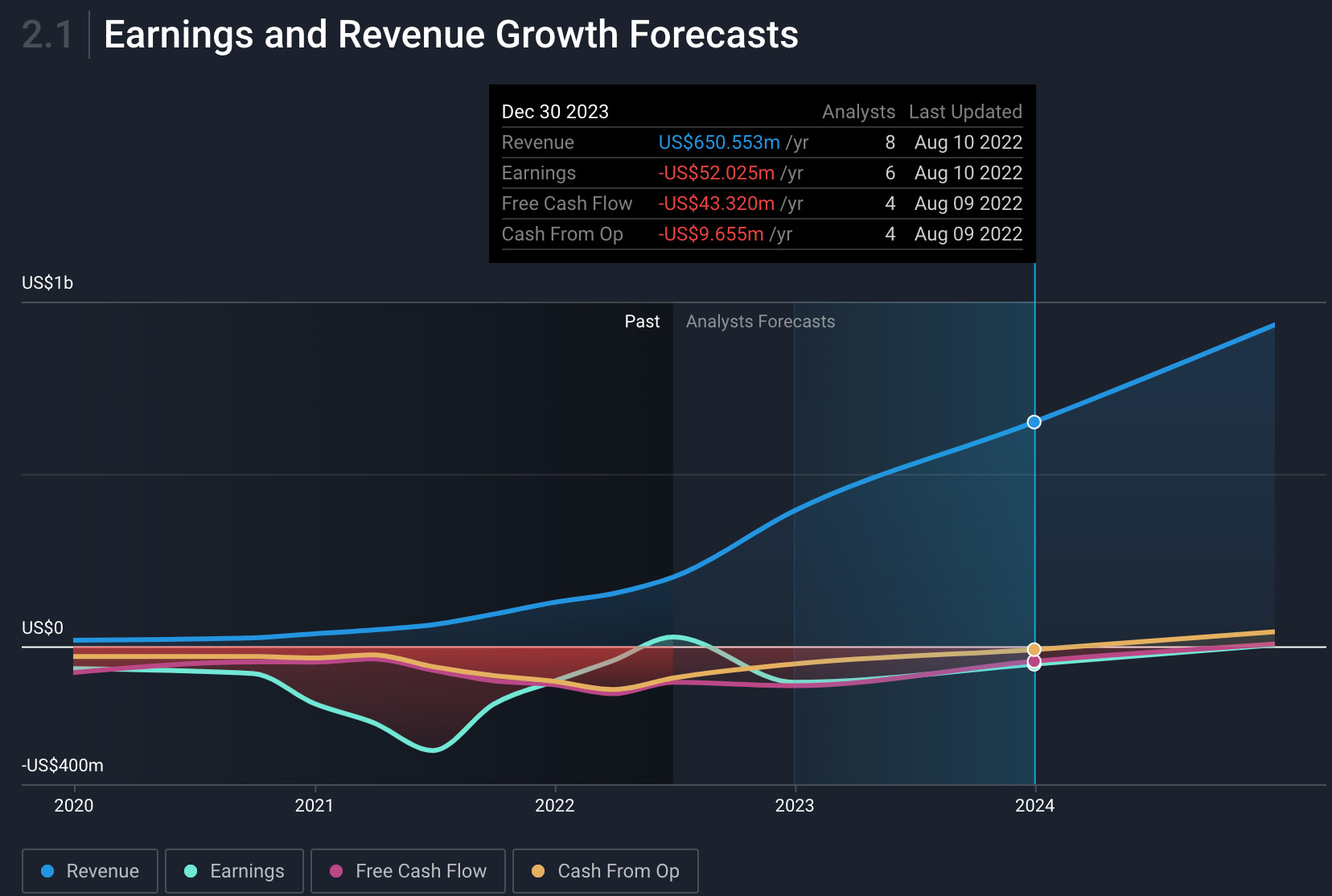

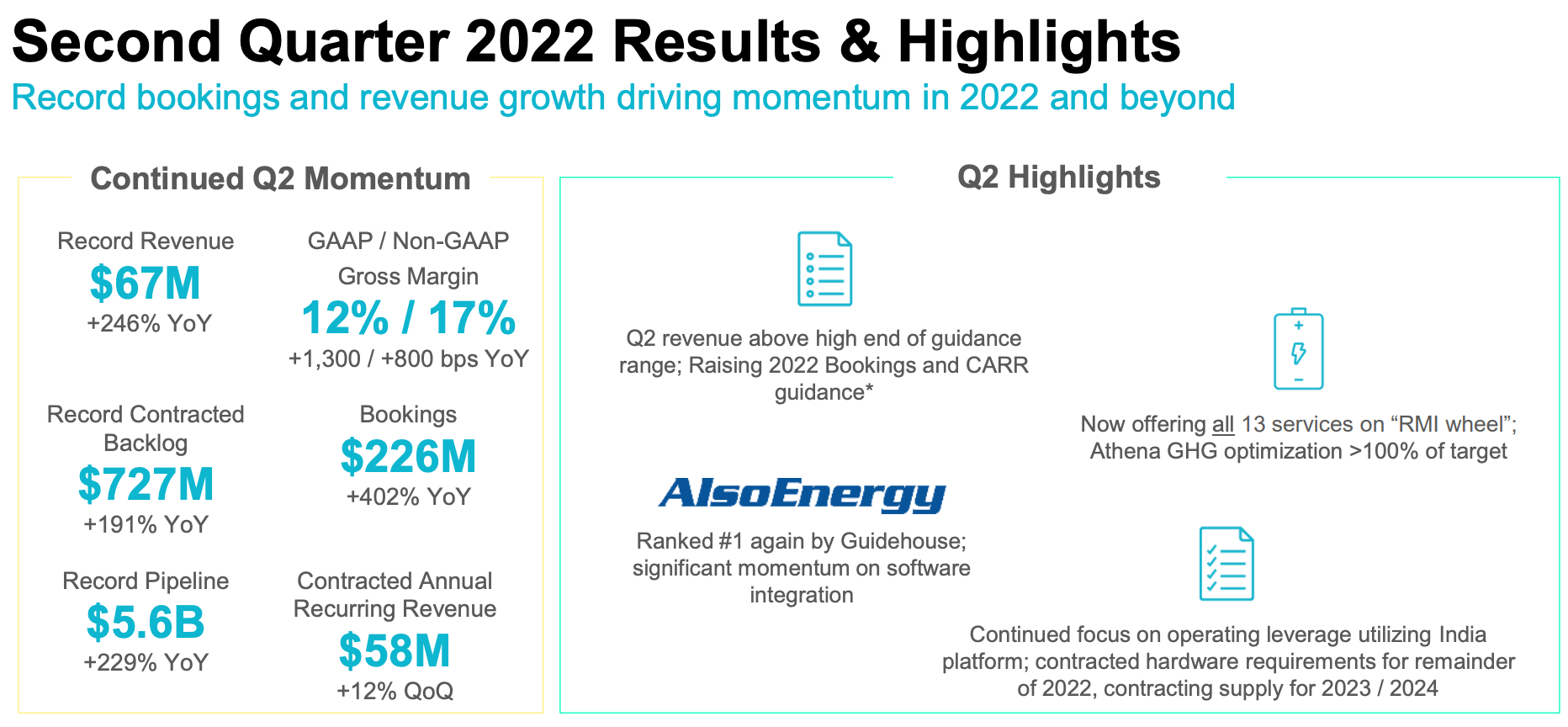

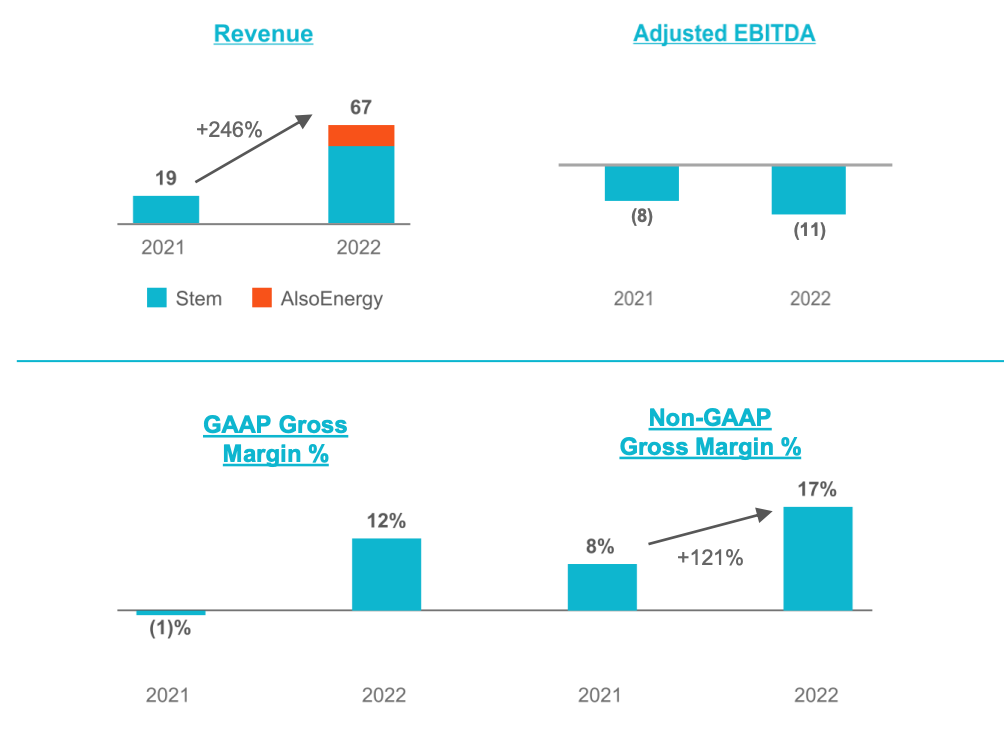

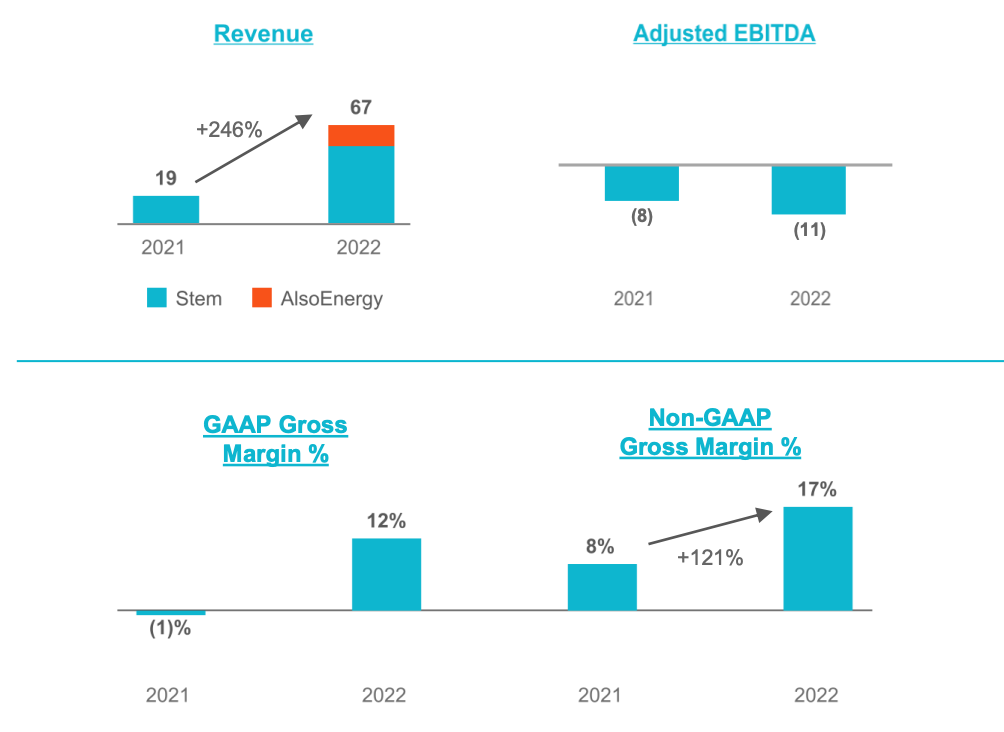

They are currently growing 246% YoY with a massive back log of projects that offer substantial visibility into future revenue growth. Expected full year revenue this year is approximately $400m which puts this business at a P/S of 6x this years sales. For next year, analysts have them doing $650m which is about 4x forward P/S (I think this is conservative because of their backlog, I’ll explain more in a moment).

They are currently losing money but have been scaling to operating break even. Since De-SPAC’ing I have watched them go from negative gross margins (last year) to expanding gross margins to be positive. This is predominately driven by their business model and exactly how it’s structured.

STEM is in the Business of Energy Storage and Optimization

As a world, we are transitioning to renewable energy solutions. The problem is that when it comes to solar or wind, energy is not always accessible. The Sun is only up for so long and the wind only blows so much, storage of the produced energy becomes a need-to-have.

STEM fills this need by offering both the hardware needed to store the energy and the software needed to manage it. Yes, you heard that right, they are a hardware and software business.

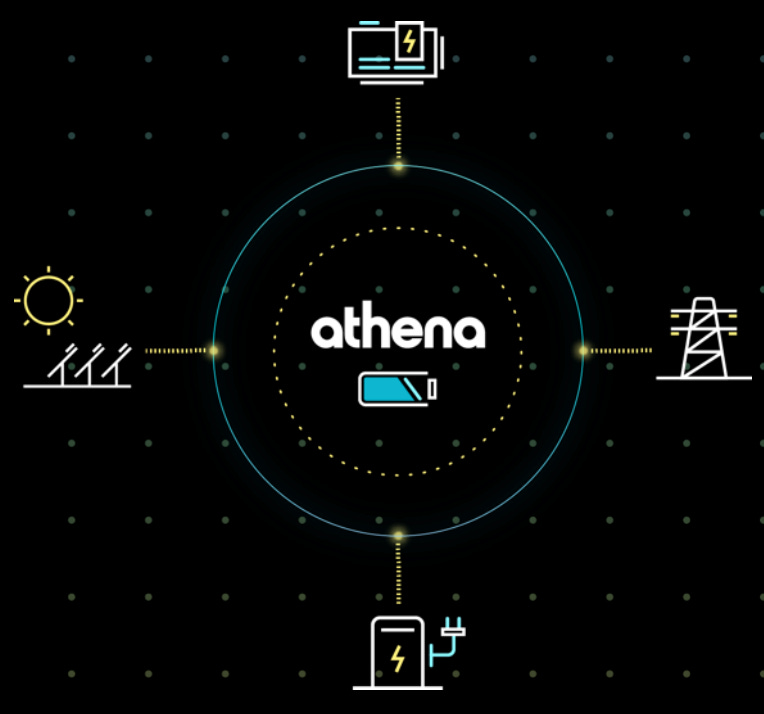

Athena, their software platform, is at the center of everything they do. Athena manages energy storage to optimize consumption to prevent wasteful output. A few solutions they have include:

Solar Storage

EV Charging and Energy Management

Utility Infrastructure Grid and Energy Storage

Utility Cost (bill) Optimization

Battery and Energy Storage

Think of it like this to simplify; Stem is in the business of helping utility companies, private enterprises, and government manage their renewable energy grid. They sell both the hardware component to storage and the software to better optimize it. A few of their customers include some of the largest companies in the world.

The Thesis and Long Term Potential for STEM

When I analyze any business, I do speculate to some degree, as most investors should. We need to ask ourselves the question, “where can I see this business going over the next 3, 5, or 10 years?”

My Thesis for Stem is that their business model today offers a very unique ability to innovate into something much bigger than what they are today. They specialize in the hardware, software (governance) and services of renewable energy storage. The are subject matter experts in the industry of tomorrow, making them uniquely positioned to become a massive energy player later on down the road.

The Software, Athena, in particular offers a massive growth vector for years into the future. The hardware component to their business will eventually become obsolete (in the next 10 years) as more battery manufacturer’s inevitably meet demand. I sort of look at this like the TV Market. At first, there were only a few players and then over time, more emerged.

When it comes to Athena, they have a unique first mover advantage in product development. Over time, I anticipate Athena becoming a much larger portion of their overall revenue because the problem it addresses is not just unique to the hardware Stem sells, it’s universal for all storage solutions. The hardware offers a competitive fly wheel approach that often leads to more software sales. It is important to note that STEM’s leadership mentioned that they are seeing increased demand (nearly 10x) for just their software.

STEM Financials

The growth story (business model) is excellent but no story is too good to overlook the financial portion of their business. Think of financial statements as the “health report” to the business. It tells us, as investors, what our returns are and can be well into the future on a numerical perspective. Typically things I am looking for when it comes to their financials:

Solid growth, signaling strong consumer demand for the product

Well managed cash flows and strong cash position

Little to no debt especially if the business is currently unprofitable or not generating cash flows

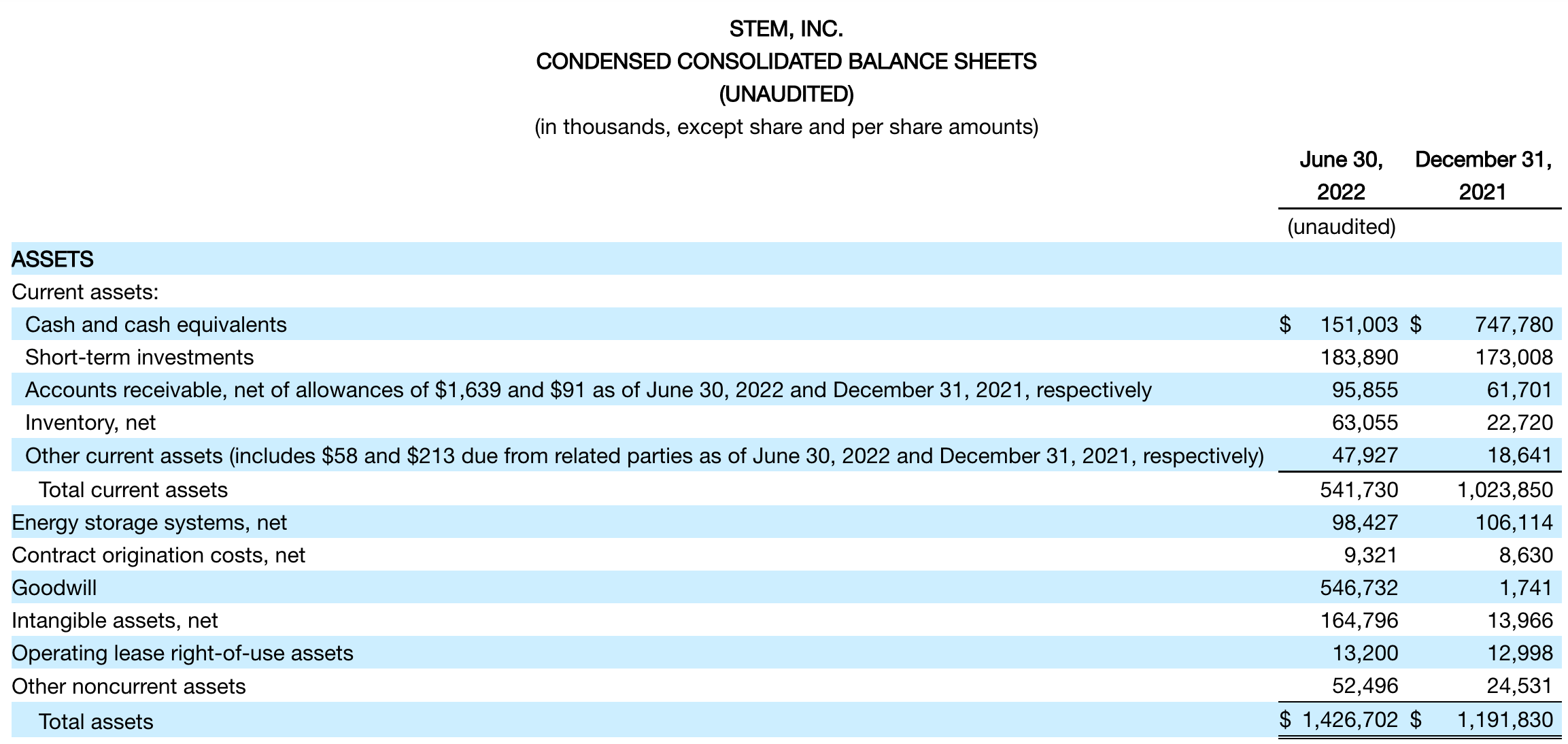

STEM checks all these boxes. Looking at the balance sheet we can see that their cash and cash equivalents exceed $300m while their current debt is about $15m and long term debt around $67m. This means that as long as they can control their cash flows (until profitability), they have more than enough room to execute their strategic vision.

Note: As a reminder, referencing an image above, analysts have STEM projected for operating break even by 2024. This is approximately 6 quarters from now.

Obviously with any company that’s losing money, they must be showing growth. The reason why this growth is important is that it allows businesses to reach operating scale. Recall above I mentioned two important details:

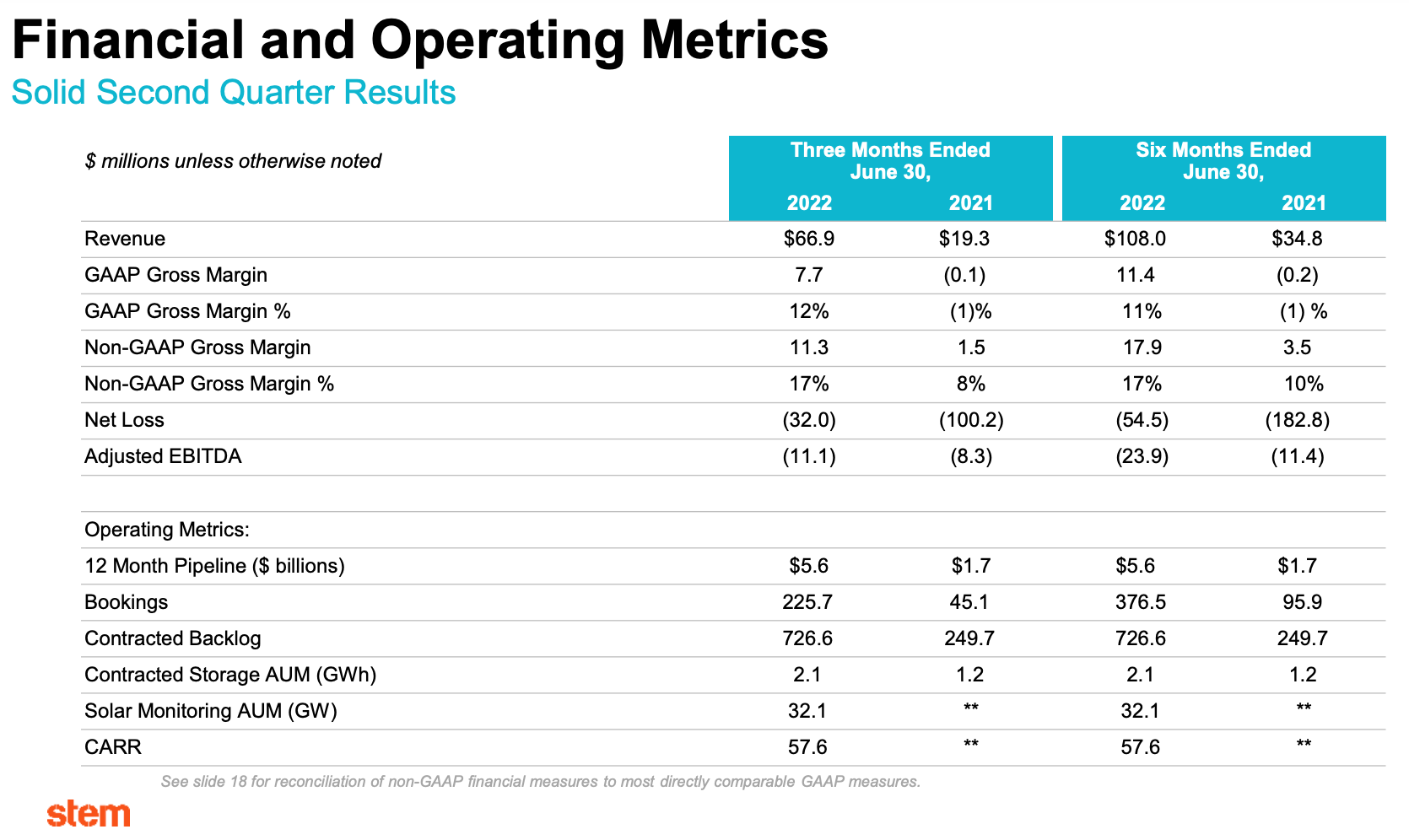

Software revenue, in the image above it shows gross margins at 80%. This means that as they sell more software, this will allow them to reach operating scale and break even with cash flows/profitability.

They have a backlog that offers extensive visibility into future revenues

First thing we can take away from their financial results is that they grew 246% year over year, that’s earth shattering growth. More importantly, there are two other metrics they report on that can give us certainty as investors that future growth will reliability continue:

Bookings: This is booked “business” (future sales) in a given quarter. Basically, as businesses sign contracts this is sold future business that cannot be counted as revenue yet but will be as services are fulfilled.

Contracted Backlog: This is business (future revenue) that has been sold, under contract, and needs to be fulfilled but cannot be counted as revenue just yet. Today, they are having hiring challenges to meet the demand they are seeing in the market. This is a good problem to have. It tells us they have a good product. It’s easier to fix supply issues than demand issues. Tesla TSLA 0.00%↑ has this similar issue and has had this issue for about 5 years now.

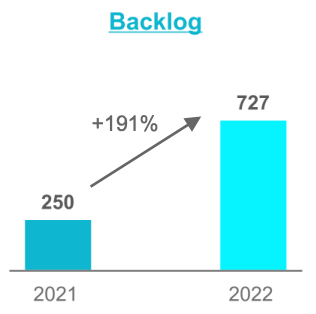

The best way to think of these metrics is that bookings lead to contracted back log which leads to revenue on the income statement. This backlog has grown 191% on a YoY basis.

Something important to note is that backlog can become a business challenge. If we see revenue slow but backlog grow, this will tell us (as investors) that they are having execution issues as a business. This execution risk is the biggest risk I see to the business today.

As Financials Progress, This is What We Should Watch

We need to see continued revenue growth and, in particular, pay attention to software growth. This software component is crucial to their ability to reach profitability.

Their cash burn and cash position. They have a limited runway for cash till they become profitable. If they continue scaling effectively, this shouldn’t be a problem. However, in earnings releases the headlines will rarely say “slowing growth and increased cash burn”. As investors, we much watch their quarterly cash burn remain consistent or improve while still seeing revenue growth.

Backlog and bookings continue to grow but making sure at the same time that this number is not becoming too disconnected. It will be a problem if the bookings, revenue growth and contracted backlog start showing an imbalance.

Debt, we must watch to see if the business takes out any long term or short term debt. Typically when a cash losing business takes out debt this can signal that they wont reach profitability by their projected date. As it stands today, they have enough cash to reach cash flow break even. They shouldn’t need to raise debt or sell business equity.

Adjusted EBITDA and Gross Margin Expansion. From an EBITDA (Earnings before Interest, Taxes, Depreciation & Amortization) perspective, we want to see this number become a lower % of overall revenue. In the below image, we notice the adj. EBITDA loss grew to $11m but as a % of overall revenue this declined because sales increased substantially (246% YoY). Gross margin % is equally as important as well. This tells us the software component to their business is becoming a larger portion of the overall revenue which will lead to better cash flows, EBTIDA and eventual profitability.

Conclusion on Initial STEM Analysis

I have began a position in STEM, which is a decent % of my overall portfolio. After a few days of analyzing this business (following since they de-spac’d) I have found that STEM offers an attractive risk reward at this valuation.

They offer a very unique exposure to renewable energy, ESG (global climate initiative) and the secular shift to energy storage/management. I look at them as the necessary tech infrastructure to businesses to help them meet their expectations set by the government. For example, if Amazon wants to change its entire delivery fleet to EV trucks, STEM can assist and help them accomplish their decarbonization goals with their storage solutions and Athena. They already work with UPS and META, I can’t imagine more businesses are ready to adopt their solutions.

The biggest risk(s) I can see today are execution and competition risk. The renewable energy market is a very young, fast growing, market with many players. I anticipate many mega winners of tomorrow will be focused on energy technology and energy storage. STEM must execute on its vision, over coming short term challenges presented in any macro environment and continue to improve their software offering. Today, these risks are not very apparent as management is, and has been, executing on everything they have said they are going to do which has given me confidence to take a stake in the business.

I look forward to keeping all of you up-to-date in my analysis of STEM

My Portfolio: Changes, Strategy and Rebalancing

Keep reading with a 7-day free trial

Subscribe to BluSuit to keep reading this post and get 7 days of free access to the full post archives.