SoFi: Leading the Way for Digital Banking

SoFi: Leading the Way for Digital Banking

SoFi finds itself at the intersection of major secular trends

JP Morgan’s CEO, Jamie Dimon, released a share holder letter in April 2021 mentioning, “Banks ... are facing extensive competition from Silicon Valley, both in the form of fintechs and Big Tech companies,” like Amazon, Apple, Facebook, Google and Walmart, Dimon wrote, and “that is here to stay.”

Fintech companies, in particular, “are making great strides in building both digital and physical banking products and services,” Dimon said. “From loans to payment systems to investing, they have done a great job in developing easy-to-use, intuitive, fast and smart products.”

Although Dimon didn’t mention it directly, my familiarity with SoFi’s business model led me to believe that he was referring specifically to them. Many businesses have tried to create a “banking super app” but few have the broad capabilities under one platform that SoFi has. In addition to these capabilities, we cannot leave out how they own the infrastructure that many of their top competitors use and will continue to adopt.

The expected structure of this publication, for ease of navigation and reference for all of you, will be:

1.) The market dynamics, NEO Bank, Lending, and BaaS infrastructure

2.) SoFi’s position in this market

3.) Financial performance so far, guidance and current valuation

4.) Opportunities for sustainable long-term growth

Market Dynamics and Secular Trends

I often post about millennials and the secular shift of technological adoption. We truly seem to be in a very innovative period in America right now. Millennials are 2.5x more likely than Baby Boomers to adopt different banking solutions and 1.5x more likely than Gen X. The Millennial generation is focused on convenience, peer to peer transaction, electronically transferring funds between accounts, and many other digital products that makes money management easier and more assessable.

Where we find this solution is in Neo Banks and Credit unions. Neo banks specifically go beyond offering the simple, brick and mortar, banking solutions that older generations have had access to. Neo Banks typically focus on:

Payments and money transfers (SoFi, Money Lion, CashApp, Venmo, etc.)

Online personal and business loans (SoFi, Square, Upstart, etc.)

Investing and saving apps (SoFi, CashApp, RobinHood, Voyager, etc.)

Bill payment and expense tracking (SoFi, traditional banking apps)

The center of all this is the tech centered approach which creates ease of use, instant transfers, and more control over a financial journey. Millennials, if done correctly, have little to no reason to go down to the bank to get a loan, financial advice, transfer money, or set up a bank account. FinTech’s like Neo Banks or Blend Lab $BLND (a software company that powers banking apps) quickly addresses this growing demand.

As important as FinTech’s (and Neo Banks) have become, it’s arguably just as important to understand the infrastructure component. To draw comparison, we can bridge the gap with something we’re commonly familiar with such as AWS, or Amazon Web Services. AWS provides cloud infrastructure for other company’s to host their digital capabilities, and in some cases their entire business, in a seemingly limitless data rich environment. Banking as a Service (BaaS) is a lot like AWS or the infrastructure component of this products. A more exact definition I found about BaaS can be, “BaaS is an end-to-end model that allows digital banks and other third parties to connect with banks’ systems directly via APIs so they can build banking offerings on top of the providers’ regulated infrastructure, as well as unlock the open banking opportunity reshaping the global financial services landscape.”

Stripe is a perfect example of a BaaS company that many of us are familiar with. Behind the scenes, many of us have worked with Stripe but have never truly known. It is important to understand that Stripe is more focused on payment solutions on the backend, rather than products like PayPal being more on the front end. Back end and front end means customer facing or not, Stripe is now always directly customer facing.

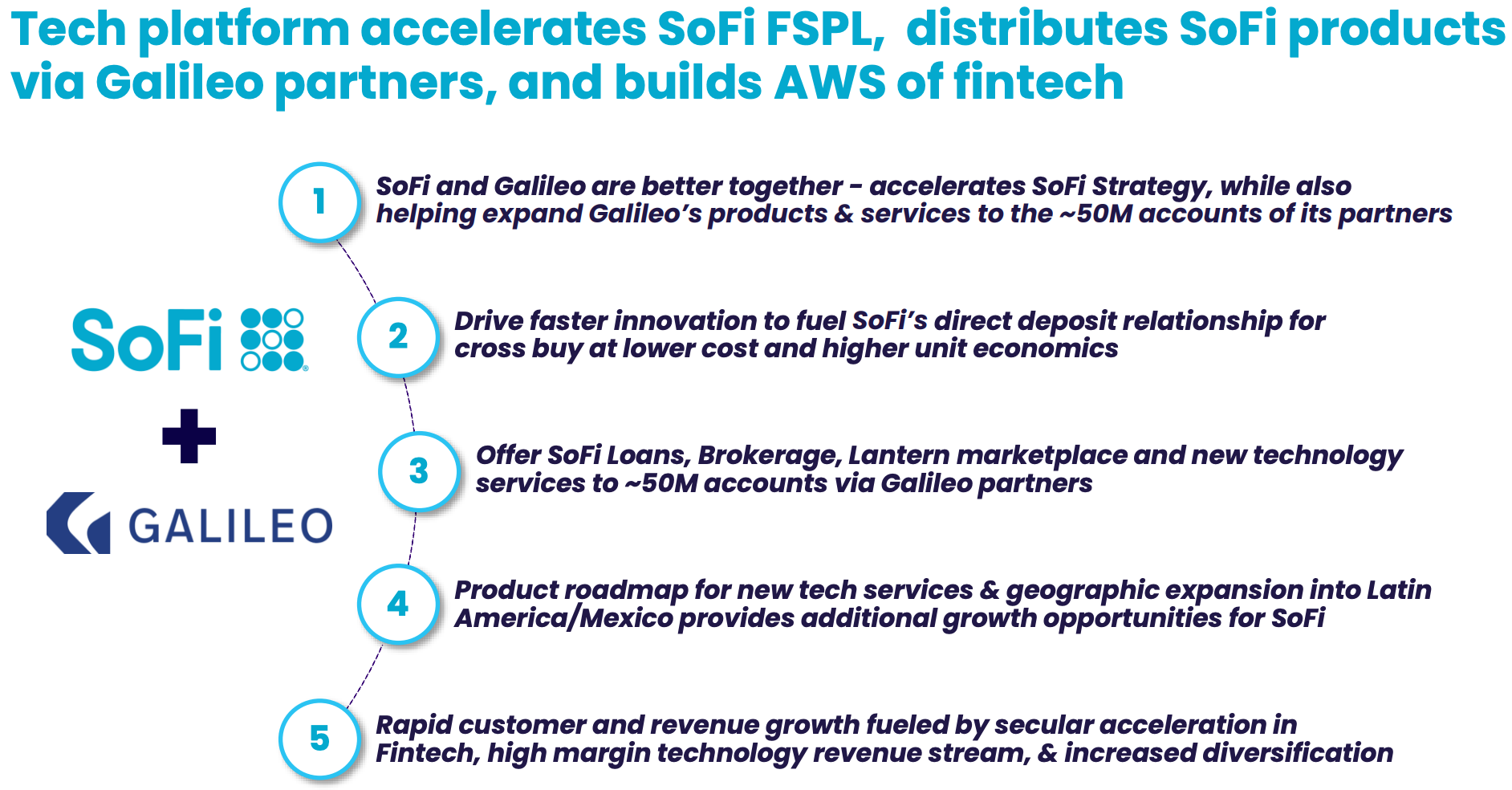

There is another component to BaaS and this is where businesses need a tech solution to host their API’s and customer facing solutions. This is where Galileo comes in. SoFi acquired Galileo in 2020 (this is only a year old) in a market shifting transaction.

SoFi Finds Itself in a Unique Position

SoFi is a leader among Neo Banks. Personally, as the author, I have tried various other solutions and have accessed the scope. Let me share my story briefly and the challenges I had.

A few years ago, I thought, “it would be easier if I could just manage investing, banking, my CC, loans, my credit score and spending habits all on one single app”. I had approximately 3-4 different banks for to serve this expansive need. I began looking around, first stumbling across Venmo where I could easily send and receive money digitally. This all but got rid of the need for cash. Next, I found CashApp that allowed me to invest in Bitcoin, store my cash, and even put money into other stocks. This was short lived soon after I found SoFi.

SoFi goes above and beyond their financial product offering. They offer all the products a traditional bank does and more. It’s also significantly easier to manage and transfer money between all product offerings due to a single app. More importantly, as I seek to expand my investment portfolio into real estate, SoFi allows me to instantly access and monitor my credit score (an ability to gauge access to rates & leverage), budgeting and spending habits through various analytics.

As you can see, I need to cutback my September spending to get back into budget. Not having to take the time building (another) excel spread sheet and having this is invaluable to anybody conscious about their finances/time.

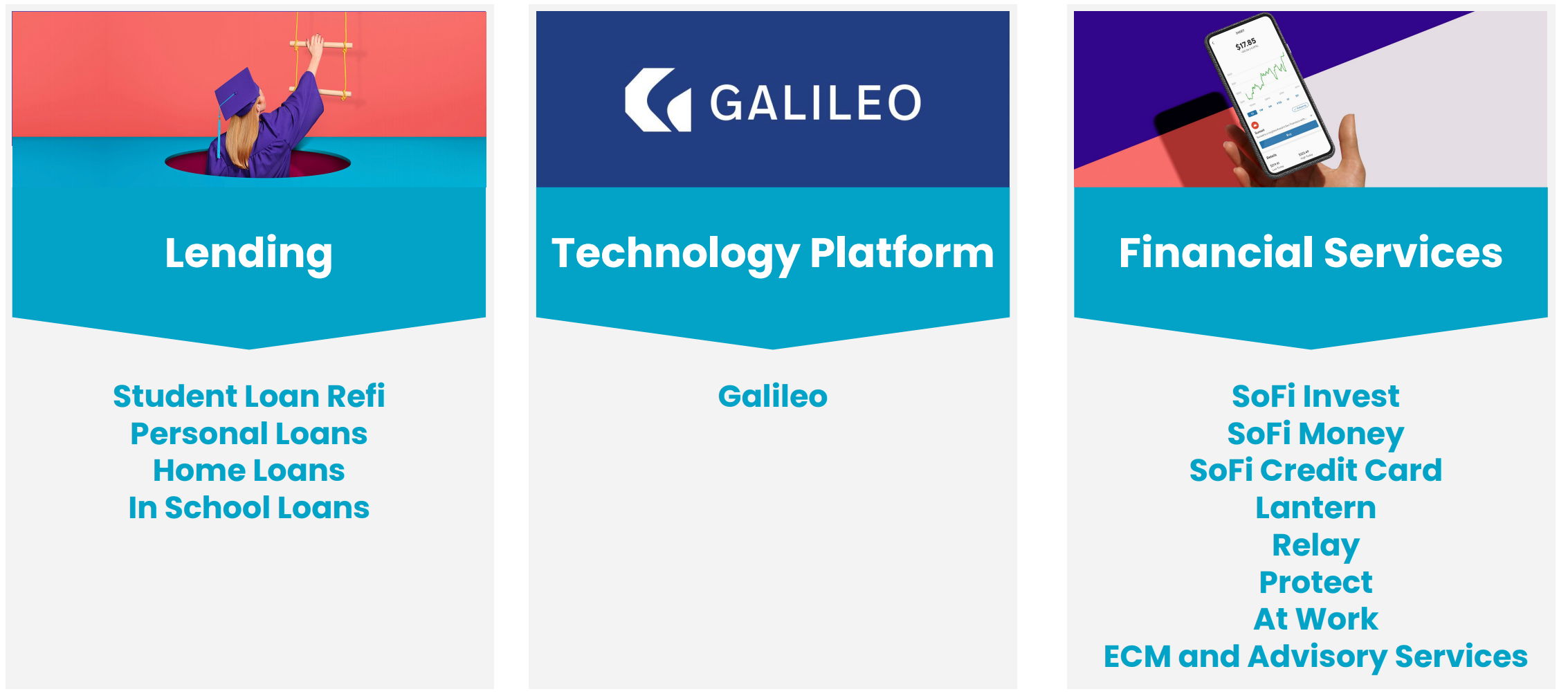

Financial services aside, it is important to mention that they have three Pillars to their overall business model.

I wont touch up too much on the lending portion because this is their slowest growth. Originally, this was their bread and butter where they first began. But, as they grow, it’s their slowest growing segment and almost a complimentary service (although still the dominant stream of income, for now). The most important product, that truly brings their unique position to life, is Galileo.

As mentioned above, they acquired Galileo in 2020 and the reason they did this had to do with the synergies between the two. As they moved away from lending and began creating financial services, they quickly realized they didn’t have the ability to create all the products they needed/wanted to create within their platform. However, their partner, Galileo, did. This quickly enabled SoFi to create a unique competitive position/advantage, drive innovation faster, and enhance operating margins.

Galileo acts as the AWS of digital banking where some of the leading FinTech players use its banking infrastructure and API’s such as Robinhood, Dave, Money Lion, SoFi and Wise. They specialize in providing digital banking products and card issuance. What this means is that they can help other businesses build on top of their infrastructure and help manage the debit/credit cards they may issue to their clientele.

When you combine Galileo and SoFi’s financial services solutions, what you get is a super FinTech that specializes in providing the banking products while collecting data from other players to provide best in class financial services for SoFi clients. In comparison, Square’s Cash App outsources it’s cards to another player, Marqeta $MQ. SoFi doesn’t need to do this, they already own the necessary infrastructure.

SoFi Financial Results

SoFi’s financials are being disrupted be policy pressures, specifically the CARES act. This suspends student loans at a 0% interest rate and disallows any collections on defaulted student loans. A portion of SoFi’s lending business is student loans. This disruption is by no fault of their own.

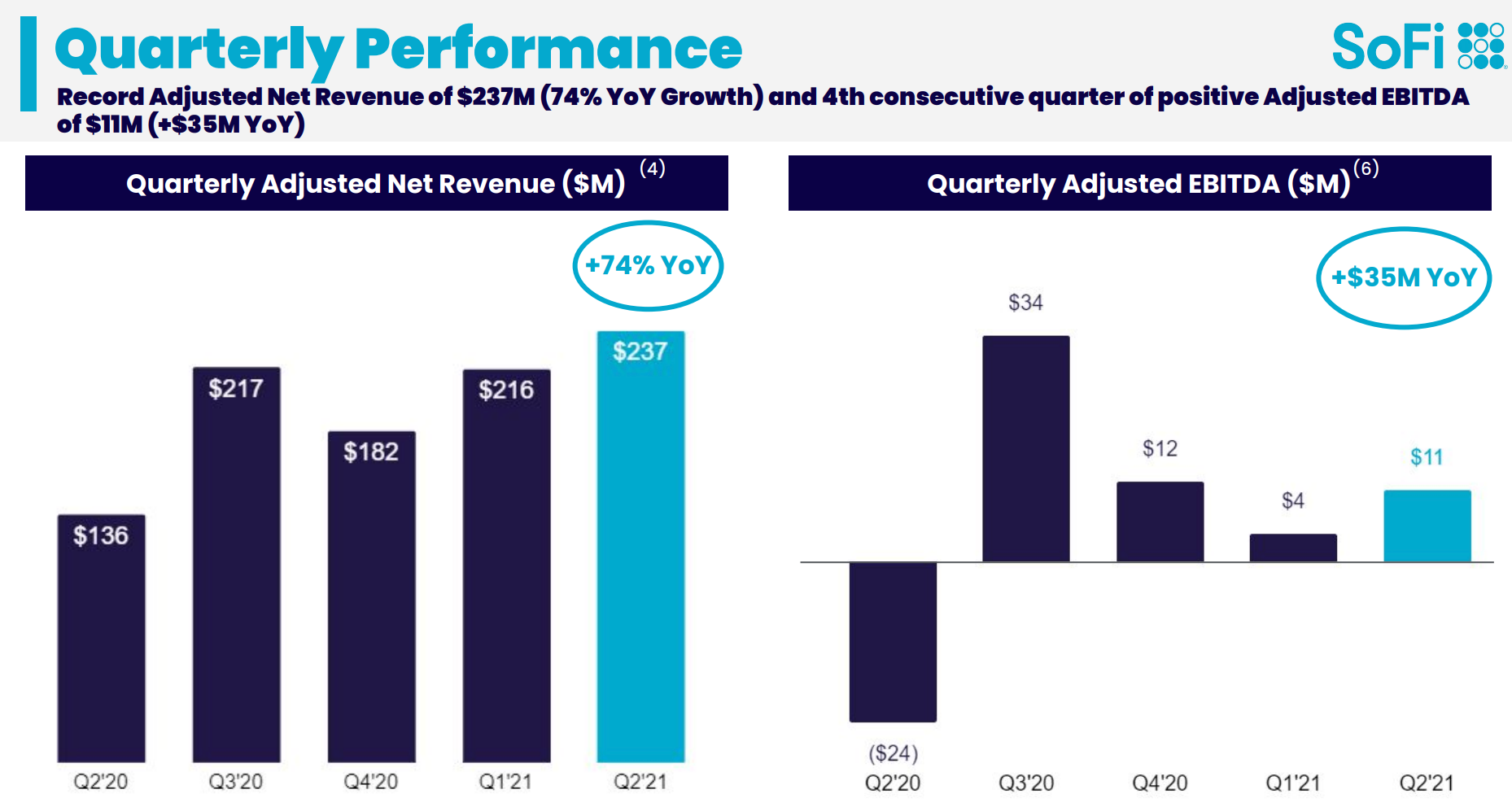

Despite this disruption they still met and exceeded Q2 financial guidance for revenue but did have to decrease Q3 guidance. They did re-iterated full year revenue and EBITDA guidance, due to out performance outside of their lending segment.

Their top-line financials from Q2:

Q2 revenue of $237.2m (+74.2% YoY) which beat by $18.6m

Adjusted EBITDA of $11m, beating guidance by $9m - $19m

Lending rose 13.9% YoY with revenue of $172,232

Galileo rose 122.9% YoY with revenue of $45,297

Financial services rose 243% with revenue of $17,039

Q3 guidance:

$245,000 - $255,000m in revenue

-$7m - $3m in Adjusted EBITDA

They key take-a-way’s here; Galileo and the Financial Services portion of their business is growing exponentially but lending has made it appear like it’s not performing up to standards. This is directly correlated to the CARES act, which temporarily suspends student loans (a big portion of their lending business). The underlying business fundamentals are rockstar and should not be ignored. It’s hard to grow any business by 100%+ year over year.

Long term, the trajectory appears that Galileo and Financial Services will become the dominant portion of their revenue. With a crowded lending market, they compete against Upstart, native banks, and the millions of others (just kidding, not millions but a lot) this doesn’t seem like their exponential opportunity for long term revenue growth but will still a primary portion of their revenue.

Opportunities for Continued Growth

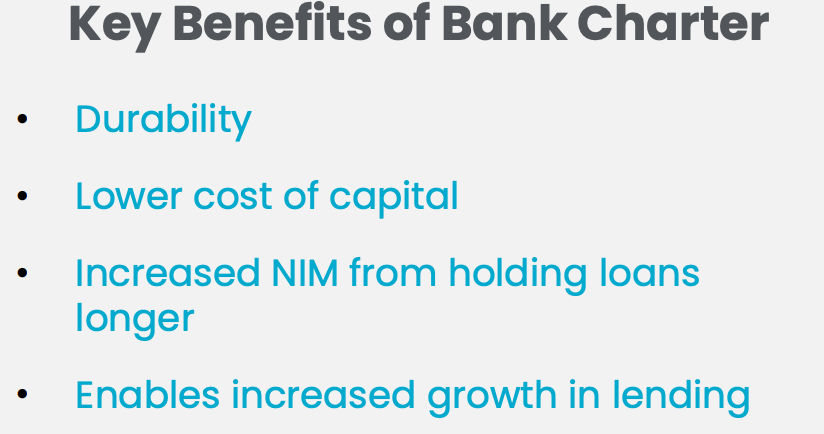

1.) Bank Charter

SoFi applied for a bank charter. They announced in March that they were going to acquire Golden Pacific Bank. This is absolutely game changing as it bridges them from just being a “Neo Bank”, to a full functioning bank. This furthers SoFi’s competitive differentiation by bringing down loan costs, increases interest offered on “SoFi Money” and can conduct normal banking operations without the traditional Brick and Mortar model. One would believe that this would competitively differentiate itself away from Neo Banks as well as traditional banks, offering a full service digital solution.

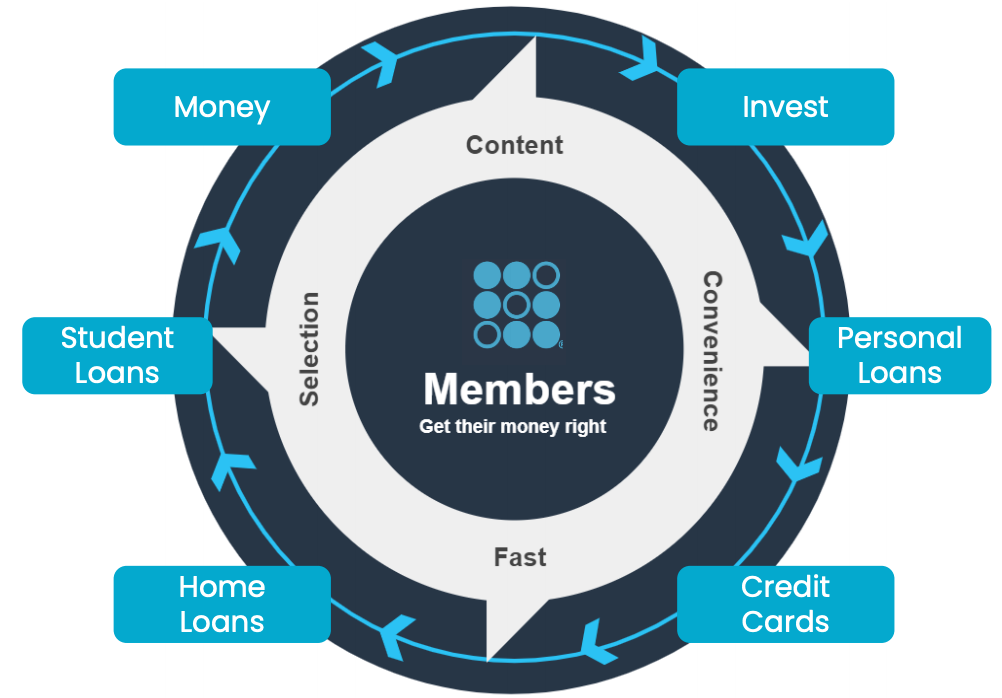

2.) FinTech Flywheel

The idea behind their model is that once they attract a customer to one of their products, they believe and have found the member continues to expand into different categories of SoFi products. Personally, this was a case for me. I do not have any loans, but I run a SoFi money account and a Credit Card.

There are two visuals they provide additional context on the historic growth between this correlation of member and products.

Member growth represents the amount of people using their platform. Product growth represents the number of products members are using. The consistent accelerated growth of 100% for the past 4 quarters for the products image is a direct correlation to their expanding service portfolio. This is likely a further catalyst for growth as they continue to add more and more products, especially the services allowed/enabled by a bank charter.

3.) Galileo Growth

Galileo has a substantial further opportunity to drive growth. In the risk portion of their 10-Q, they outlay that Galileo only has a few customers. I like to look at this as a risk and an opportunity. The have a long runway to continue to obtain marketshare as the global Digital Banking market is expected to reach $1.6T. They currently operate only in the U.S. but Latin America and Asia expansion is in the near future.

In terms of the synergies that can exist between the two platforms (described above), this transaction is only a year old. Typically major acquisitions take years to fully realize the full potential of the business combination.

Conclusion

SoFi has a very strong competitive niche when it comes to being a pure play “digital bank”. Remember, at the beginning of this publication, Jamie Dimon CEO of JP Morgan mentioned they believe FinTech’s present a massive competitive risk to them. When it comes to the complete solution from infrastructure up to an all in one customer facing product, all of it being digital first, SoFi is the leader.

If you found value in this publication, I encourage you to join many others in participating in the BluSuit community. You will gain access to many of the most interesting, high growth and innovative IPO’s coming to market with first mover in depth research. In addition, I share my portfolio management strategy and other exclusive content.

For example, tomorrow, I plan on releasing members only “week ahead” publication that will cover important catalysts, FOMC meeting technical patterns and IPO’s I plan on adding next week.

Keep in mind, I plan on continuing to add complimentary publications for all of you! I love sharing what I can!

You know this means to…….

Stay Tuned… Stay classy…

Dillon