Stock Ideas: Confluent - Leading a New Era of Data in Motion

Accelerating growth with Cloud growth @ 245% YoY and top-line growth @ 67% YoY

Confluent is a new software infrastructure business that’s pioneering “Data in Motion”. At first glance, you’d think this business was overvalued but when running forward valuations and compare it to future opportunity it quickly becomes justified, especially when you look at their accelerated cloud growth over the past few quarters.

Full disclosure, I have a position and what I plan on sharing in this News Letters is the long term business thesis, in depth DD, “data in motion” simplified, and business financials. Despite Confluent being a very technical investment, this will be geared more for the investor to identify/understand the business model, long term opportunity and the business case/risks. My goal is to save you time looking through hours of material and condense it to a 15-20 minute read for you, the reader.

The Business Thesis

Confluent finds them-selves pioneering a new category of “Data in Motion”. Essentially, this technology has existed for awhile but today, it’s in the very early innings of the long term potential. When thinking about Data in Motion, we must think infrastructure first and that’s exactly what Confluent is, a cloud first data infrastructure company.

The business value Confluent’s customers receive can be immediate, but more importantly, long term. Entire enterprises and applications can be built on top of Confluents platform. This leaves them in a very strong position especially as a majority of the competition is 5 years behind them.

Leadership also has a strong competitive advantage. Their CEO, Jay Kreps, was one of the co-founders of Apache Kafka at LinkedIn and went on to co-find Confluent. This is more important than you think because confluent was built on top of Kafka and is the standard today for ‘event streaming’.

There is a strong, generational, run way for growth as long as they maintain their strong market leading position.

Members exclusive thesis, research and due diligence below.

Apache Kafka

First, we must talk about Apache Kafka. This can get pretty technical, but you would be surprised how much we use it in our everyday life. In fact, it’s most likely responsible for the instant transactions and notifications we get when we swipe our debit cards and see the exact amount debit’d from our account moments later. Apache Kafka is the code behind this, called ‘event streaming’.

Event streaming, unlike legacy data depicts actions rather than items. Data used to be thought of as an object. Objects like: humans, cars, trucks, computer devices, etc. Kafka is the recorded action of the object in motion. Have you ever received a push notification from a friend who DM’d you on instagram? Or, how about receiving this email notification when it comes across your device? This is likely Apache Kafka. It takes an event that happened and makes it real time.

Another great example I can think of is a feature from SoFi (I bank use their products). Every time that I use my credit card, a few seconds later I receive a notification of the exact dollar amount used and what it was used on. This is likely Apache Kafka at work because I did not have to search for the data. It was constantly in motion till it came to me. This, in turn, provides a great user experience.

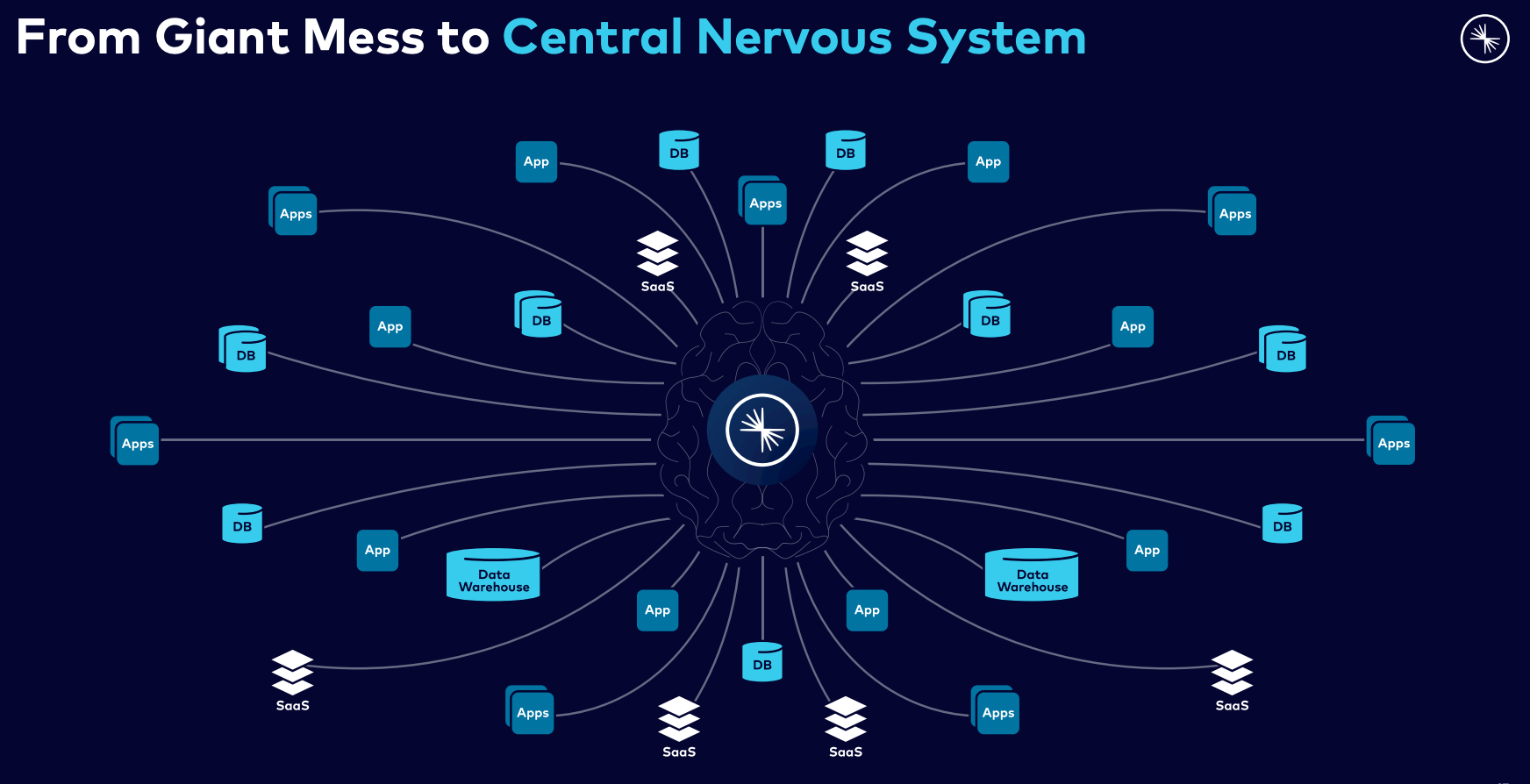

This is really best thought of as a “central nervous system” to the entire business. Think of Kafka as the electric pulses transmitting through our nerve receptors and Confluent acts a lot like our brain (I’ll break the confluent side more in a moment).

Data in Motion

Data in motion is best thought of as the continuous feedback loop of flowing data.

Imagine touching a surface. It could be hot, or cold, but either way we can tell really quick because as soon as we touch the surface our nerves tell us what is happening. This is a form of ‘data in motion’ because an action happens, we receive the information, and we react to that information that we received from our action. It’s a never ending cycle of receive and react.

Hopefully I haven’t lost you here

From a business perspective: Banks will use Kafka to track real time transactions, Social Media will deliver notifications of a message delivered to you, retail businesses can manage inventory real time, drug discovery can be accelerated with real time analytics, and so much more. Essentially, real time data flowing through a business ecosystem can be transmitted, interpreted and stored instantly. This creates a more nimble and fast moving business in the increasingly competitive business landscape.

Confluent is the Brain of the Central Nervous System

Confluent is built on top of Kafka and creates a platform to manage, secure, connect, and govern! This is important because Apache Kafka is originally open source and Confluent makes it easier to manage for organizations of all sizes.

As I mentioned under the business thesis portion of this letter, the long term opportunities are significant as well as the immediate value its customers receive. Clients of Confluent can naturally progress to the next phase of digital transformation. Businesses can both transform and build on top of Confluents platform to run customer facing applications and back end processes. What this means is that the full potential is hard to truly understand today because many of the applications that will be built from ‘data in motion’ have not been built yet.

When I envision the possibilities of Confluents platform I imagine businesses coming to life, interacting with environments and customers real time. New apps will be built for our phones and potentially new devices all together, all designed to stream data to the consumer real time. Essentially, it will be a world where everything is instant. Yes, even more than it is today.

Financials

Confluent gets dinged a little on this one for me, because they’re not profitable yet and most likely wont be profitable for quite some time. From the analyst estimates I have access to, they are not projected to be profitable within the next three years. I rarely look too much into company’s that are not profitable unless there is something truly different about them. What does bring encouragement is that they have no debt and about $1B in cash; which will leave them with years of runway to grow and capture as much marketshare as possible prior to doing another equity offering.

They estimate their total addressable market to be about $50B today, but growing at a CAGR of 22% from 2021 to 2024. Confluent is currently operating internationally and the total revenue mix is approximately 65% U.S. and 35% international.

What’s most impressive is their revenue growth and how it is broken down. On a top-line basis they are growing approximately 67% YoY but this DOES NOT show the full picture for the revenue break down, especially when considering valuations and financial modeling.

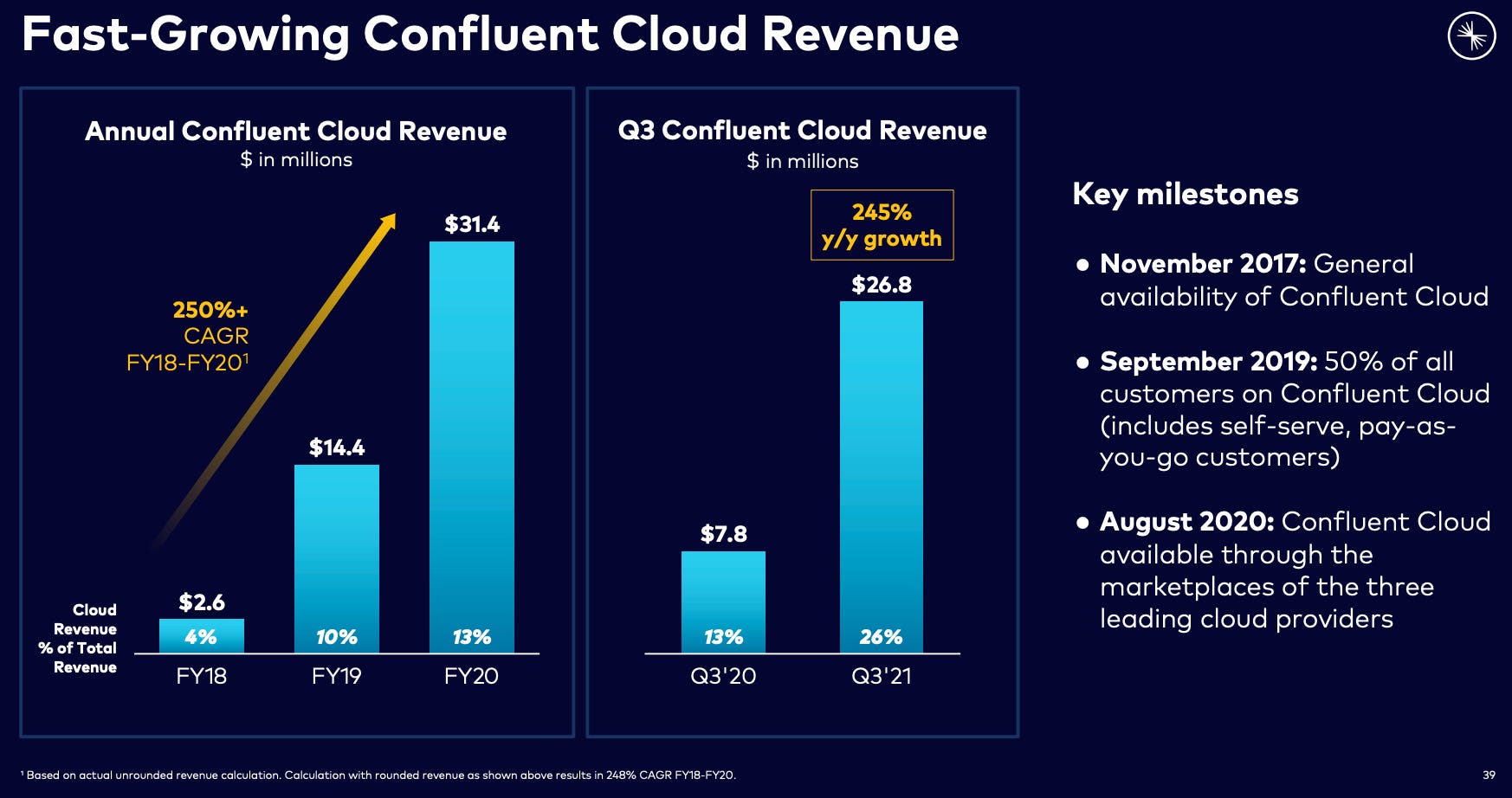

We need to focus on their cloud revenue specifically. Their cloud product was launched in 2017 and has experienced exceptional, accelerated, revenue growth with a 250%+ CAGR over the last THREE YEARS. Confluent Cloud has a consumption based revenue model, similar to Snowflake’s, and now consists of 26% of their overall revenue growth.

The primary difference between their cloud offering compared to their platform is managed vs self managed. Many customers prefer a fully managed solution.

This quarter’s revenue was $102.6m, which means that cloud was approximately $27m and platform was approximately $75.6m. They mentioned that they anticipate cloud becoming their primary source of revenue. To get a better understanding of what sort of growth we could anticipate in the future, we have to break down the growth of each segment.

Cloud three year Q3 revenue projection at 200%, 175%, and 120% for 2022, 2023, and 2024 respectively would be: $54m, $148.5 and $327m.

Platform three year Q3 revenue projection at 35%, 30%, and 25% for 2022, 2023 and 2024 respectively would be: $102.6m, $133.4 and $167.

This means that top-line would be approximately $157, $282, and $494 for the 3rd quarter. Let me emphasize how this is broken up to Q3 only. This would represent YoY growth of 53%, 80% and 75% showing accelerated revenue growth from todays financial metrics for Q3.

If we were to put this into a full year basis I wouldn’t be surprised to see them grow to $577m next year, nearly $1B in 2023, and $1.5B - $1.75B in 2024. At today’s valuation, this would be them at 21x P/S for 2023, still very expensive, but I’m not sure when they would stop growing rapidly due to their unique market leading platform.

Summary

Today, about 60% of the Fortune 100 uses Apache Kafka. This is up from roughly 30% 1-2 years ago. You could imagine, with Confluents robust enterprise capabilities, that there are addressable opportunities within that 60% of the fortune 100. In addition to the immediate opportunity, I cannot see data slowing as the consumer needs more of an instant response.

From a competitive stand point, there are a few look alike’s out there. Confluent mentioned they are keeping an eye on them but doesn’t see any immediate threats. Gartner has Amazon Web Services, Apache Software and Cloudera as their top competitors. However, these are not necessarily competitors and more alternatives. Alternatives in this perspective is similar to you wanted a hamburger but there is only hot dogs around, so you eat that anyway lol. Confluent is the enterprise platform for data in motion.

When it comes to risk, due to the valuation, competition should be consistently monitored as new players come on the map. There is little room for error or business interference. I could see a slight valuation contraction in the event of any sort of business disruption. Another big risk I see is their margin profile. Because they are not profitable or EBITDA positive, this will likely lead toward a very volatile stock. Stocks can move up and down violently without a P/E ratio and earnings floor.

The sum everything up, Confluent is an extraordinary company that’s pioneering a new data infrastructure. I would be surprised if it trades down to a “decent valuation” due to its leadership, opportunity and business performance so far. I am happy holding a position here and would likely add more if it dropped from my current cost basis.

Feel free to ask any questions if you have any!

Don’t forget to join our Discord if you haven’t already either, it’s a great way for the whole community to collaborate and shoot me a text if you wanted for any reason.

I always have content planned for you guys and I love sharing this stuff with all of you.

Stay tuned, stay classy

Dillon

Nice write-up! That cloud revenue growth is sweet sauce. I have a small starter position as well.

What really sold me though is "Alternatives in this perspective is similar to you wanted a hamburger but there is only hot dogs around, so you eat that anyway." Talk about a wide moat! A hot dog when you wanted hamburger? An absolute tragedy. 🤣