The Reason Why Interest Rates Impact Growth Stock Prices

The Reason Why Interest Rates Impact Growth Stock Prices

Defend your portfolio, don't get caught off guard and know what to look for

Congratulations, to you, the reader.

No, seriously, congratulations.

Macroeconomics and fiscal policy is a topic that interests those who seek fundamental understanding and a deeper knowledge about the environment we participate in and invest in. Charts will tell us a lot but understanding the internal workings of a company or economic environment will allow you to make quicker judgements and filter through the noise. In essence, it’s a lot like understanding what the weather is going to be outside. It’s the external conditions of which we participate in.

As stock pickers and investors, we can draw a striking similarity between betting on sports team to win during a season. In this case, the individual sports teams will have certain team composition, coaches and players that will make up the fundamentals of the team. Macroeconomics will draw a strong similarity on league policies. Would you bet on a team to win a championship during this years season if the league policies are preventing the players to play?

As an example, we could say COVID policies/protocols preventing sporting events to take place in 2020. If you knew COVID was coming (by paying attention to the macro), would that change your betting strategy? Would you bet at all?

Estimated time to read: 20 minutes

Interest rates are one of the most commonly discussed topics with many saying, “if interest rates go up, stocks (especially growth stocks) will see a multiple compression.” The purpose of this publication is to go toward the why this happens. But, in summary, you can really chop it up to two reasons:

Competition for yield when liquidity is scarce

Dimmer future economic and earnings growth

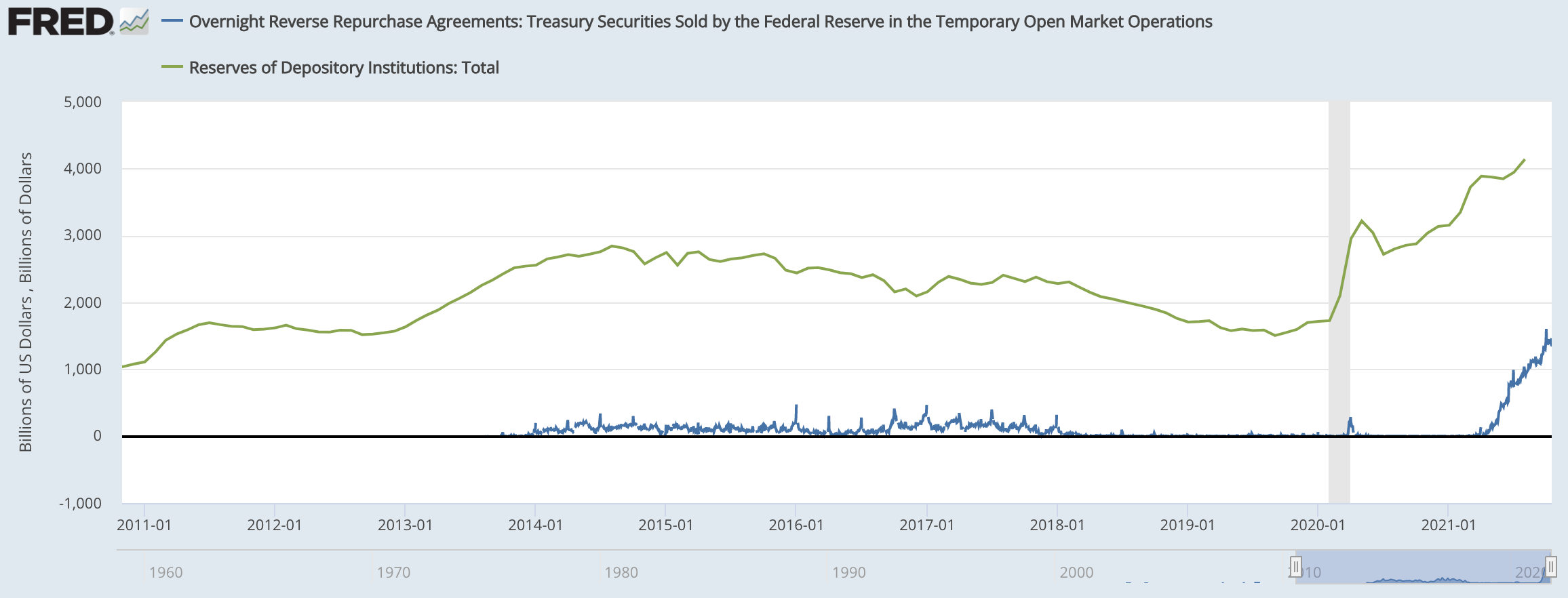

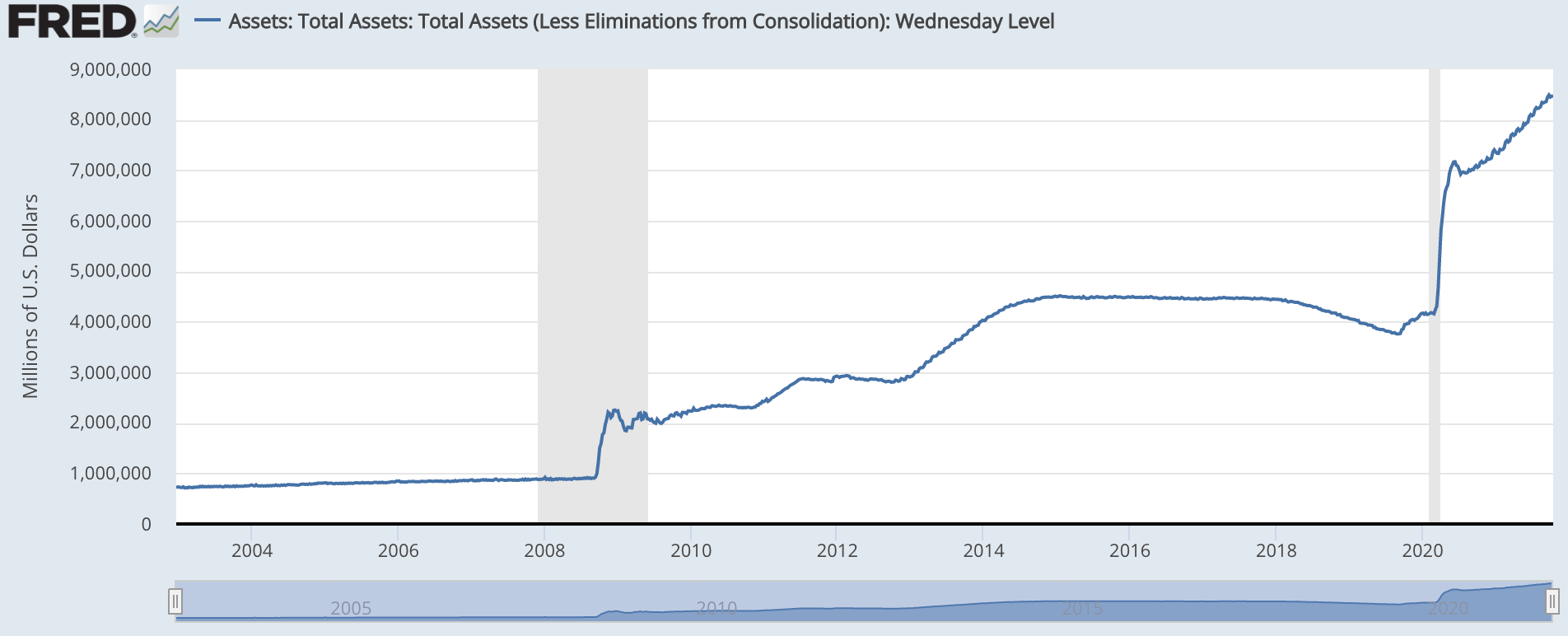

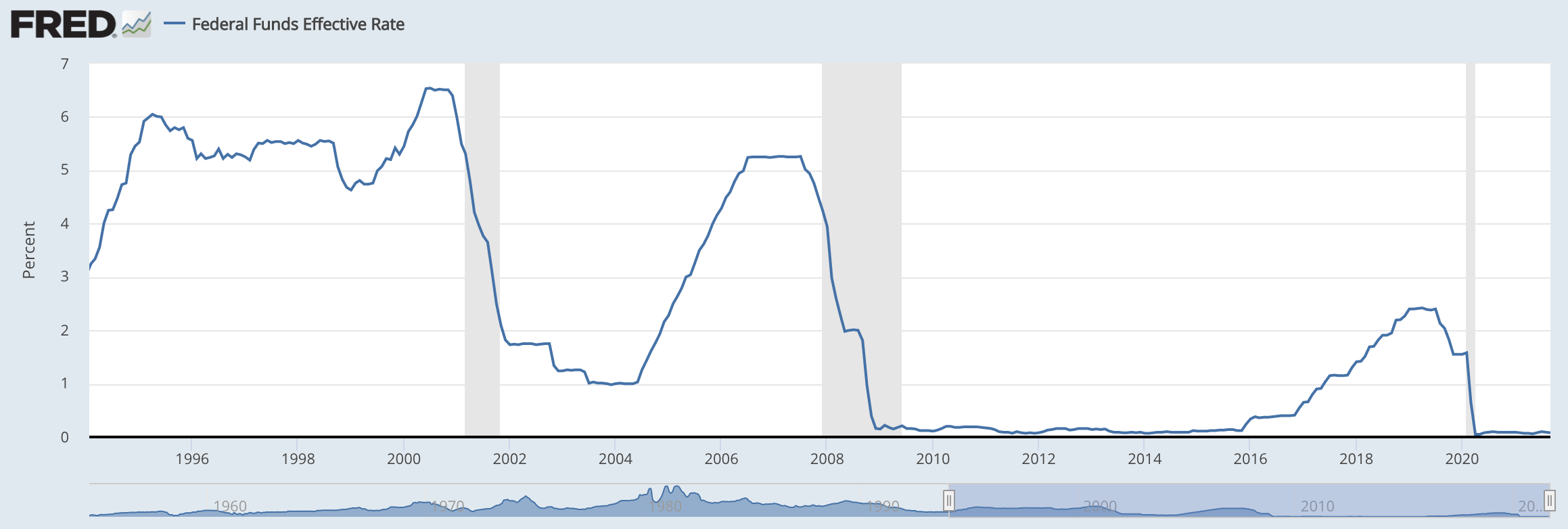

I will be focused on the latter of the two reasons because there is no shortage of liquidity in todays market. This is really reflected in the reverse repo market and bank reserves. The green line reflects reserves and the blue line is the reverse repo market. Basically this is roughly $5.5T sitting on the sidelines.

Talking about liquidity, bank reserves and the reverse repo market is for another publication. I will release that in the next Macro news letter for members.

Before we really understand exactly why interest rates influence stock prices there are a few things we must cover to fully grasp the concept of interest rates deterring economic and GDP growth, which impact stock earnings/multiples.

The Constant Battle of Inflation vs Deflation

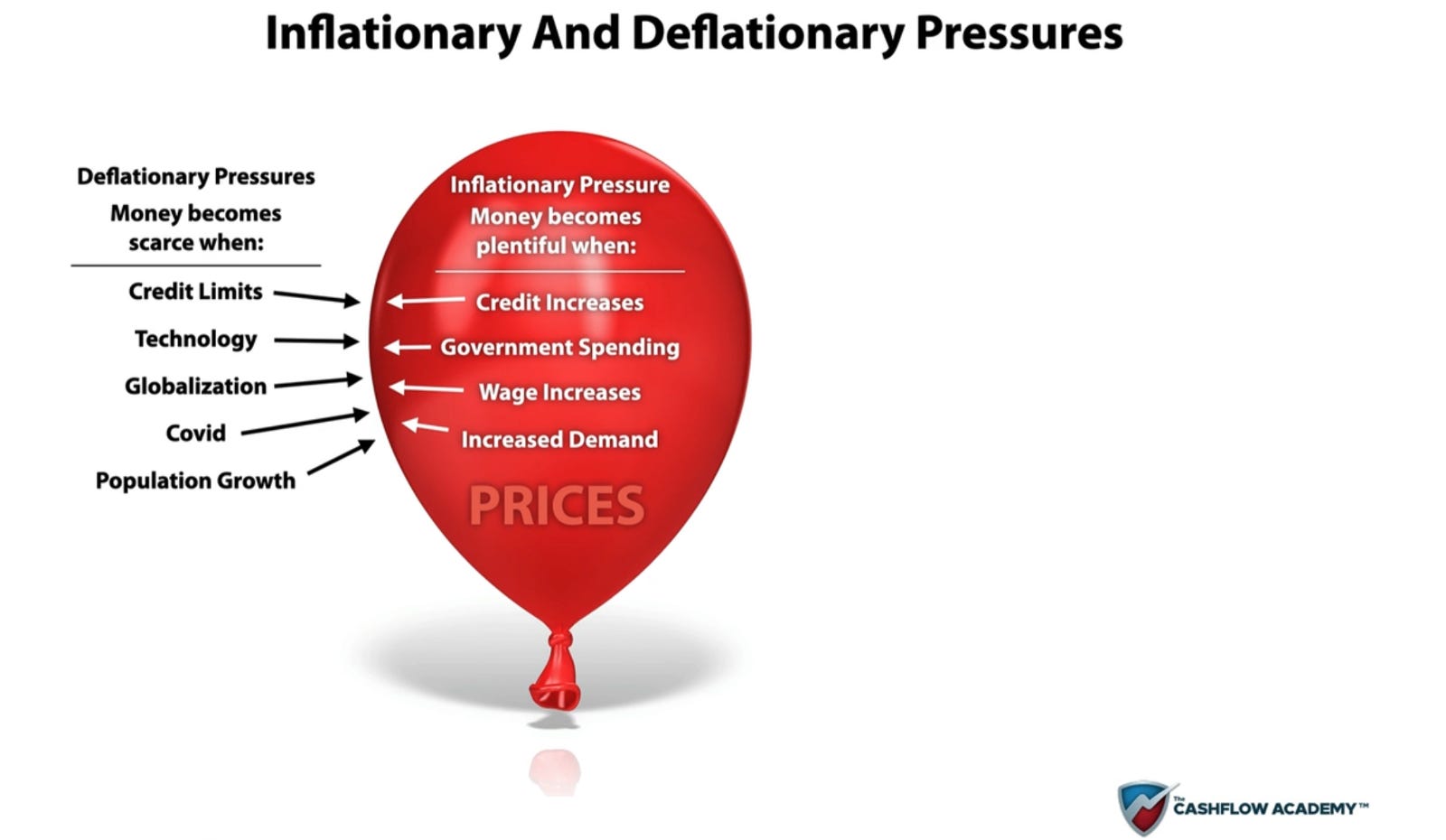

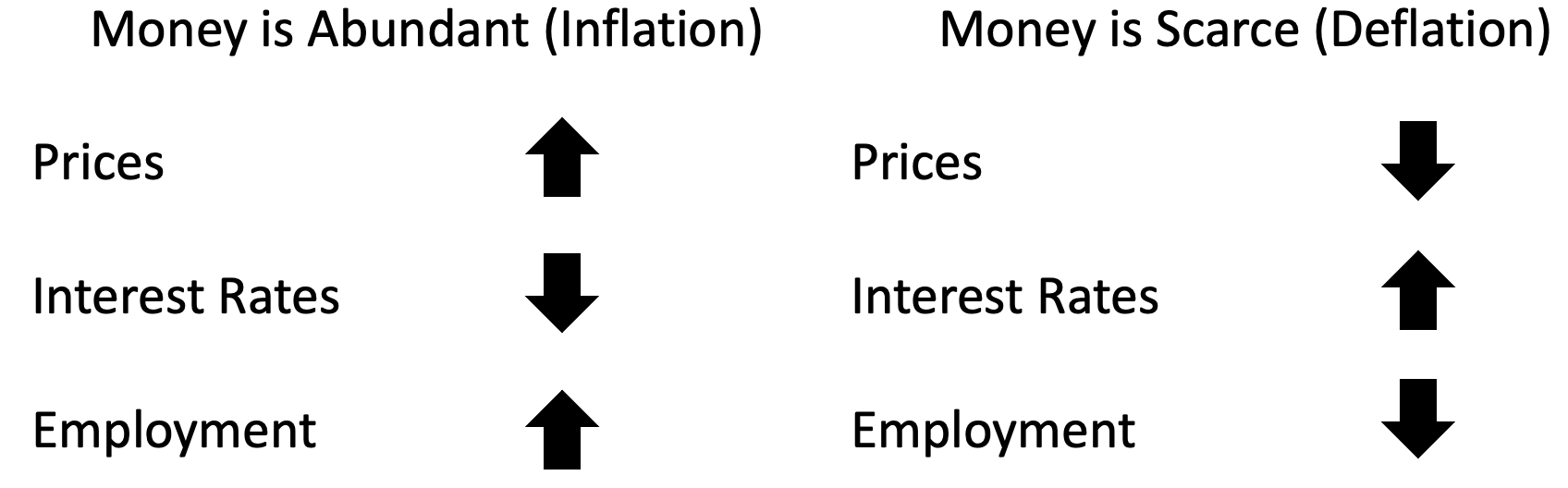

Despite contrary belief, inflation is actually a really good thing for stocks. It’s only in deflationary environments (over the past 20 years) that stocks sink. The actual concern is over what the fed will do in response to inflation being higher than usual.

In today’s economic environment there are many different deflationary forces of which are really driven by the forces in the image above. Population growth may strike you as a surprise but when you think about it, if there’s a limited money supply, and more people come into the picture that means that the dollar will become more valuable. A more valuable dollar = deflationary, a less valuable dollar = inflationary.

There is a constant battle at the Federal reserve, who is the central bank to the United States. Their job evolved over recent years to manage money supply, inflation, deflation and drive economic growth. The Fed has a few tools that really influence the inflationary and deflationary pressures in our economy.

Reserve requirements

Interest on reserve balances

Federal funds rate

Discount rate

Open market operations (QE)

Reverse repo’s

In a perfect world, inflationary and deflationary pressures are perfectly in balanced. When balanced, this creates economic and price stability. The tools they have adjust liquidity, access/availability to credit, market prices and economic growth.

It has not always been like this. What we’ve seen since the dollar left the gold standard in 1971 is that the dollar and the value of the dollar can be manipulated. For example, in 2020 we closed all economic operations in the United States sending us into a deflationary cycle.

People couldn’t work, GDP contracted, and the stock market crashed. However, the difference this time is that our recession only lasted 2 quarters making it the fastest crash and recovery in stock market history. How did that happen?

With the deflationary economic cycle being triggered by business and societal shut downs, an economic melt down was all but certain. However, the Fed (in response) and the U.S. government counteracted the deflationary forces with massive inflationary forces like unprecedented government spending/stimulus and extreme amounts of open market operations (quantitative easing, a.k.a. money printing). Think of it like a balloon that was deflating but in response, you just pumped a s&*t ton more air into it to keep it inflated.

In response, stock prices and home prices soared along with economic activity which is a direct result to the supply chain disruption that we have today.

The Evolution from Capitalism to Creditism

It’s important to know that we no longer truly exist in a pure capitalism environment and no, we’re not really “socialist” either. We’ve evolved into a completely new systems that really began in 1971 (gold standard revocation). Going back to the COVID lockdown example, when combating deflation, it’s important to know and understand exactly what happened and how that inflation happened.

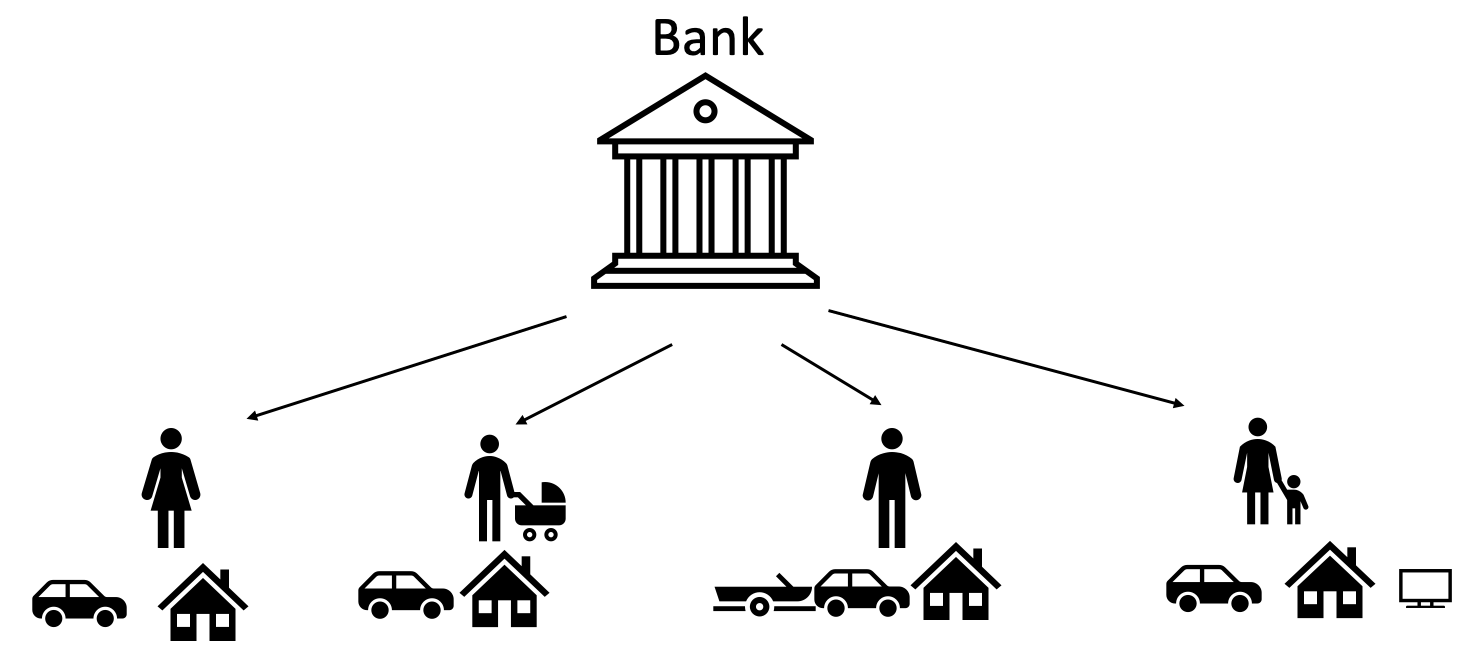

Credit growth, or debt, is what has been driving our economy forward for years. This has everything to do with how our economic system works when it comes to lending/borrowing and economic growth.

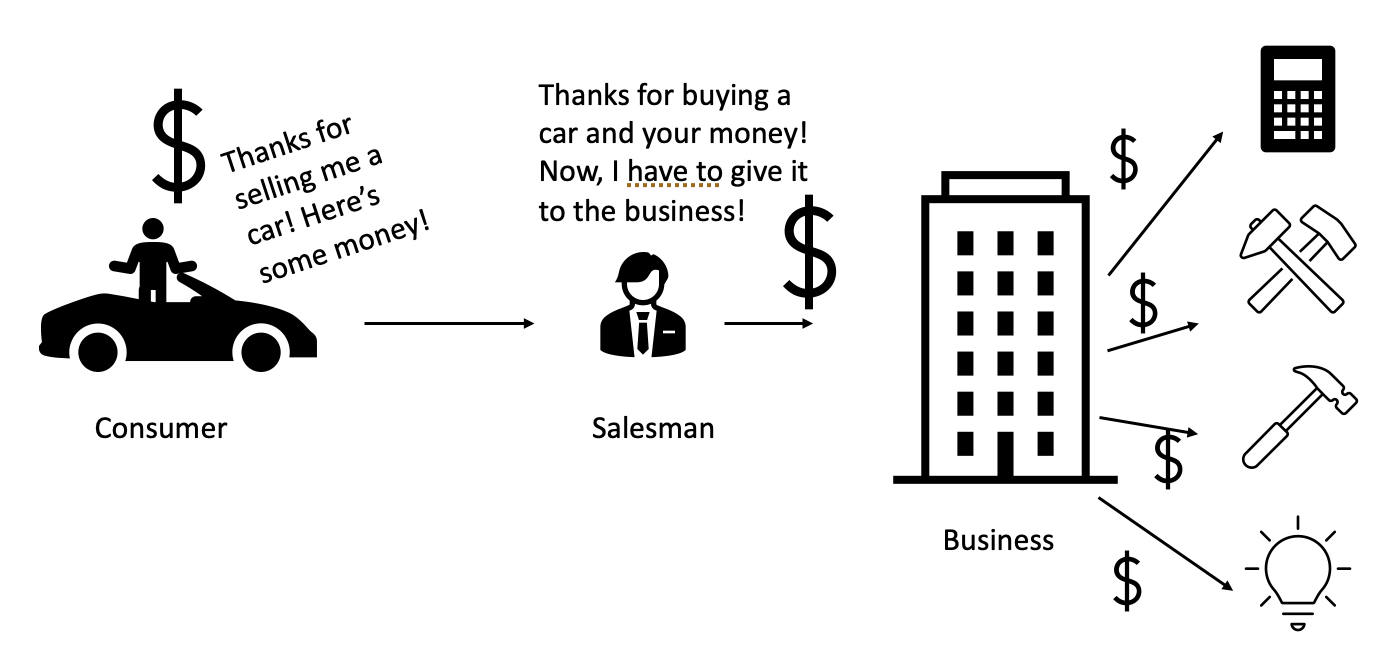

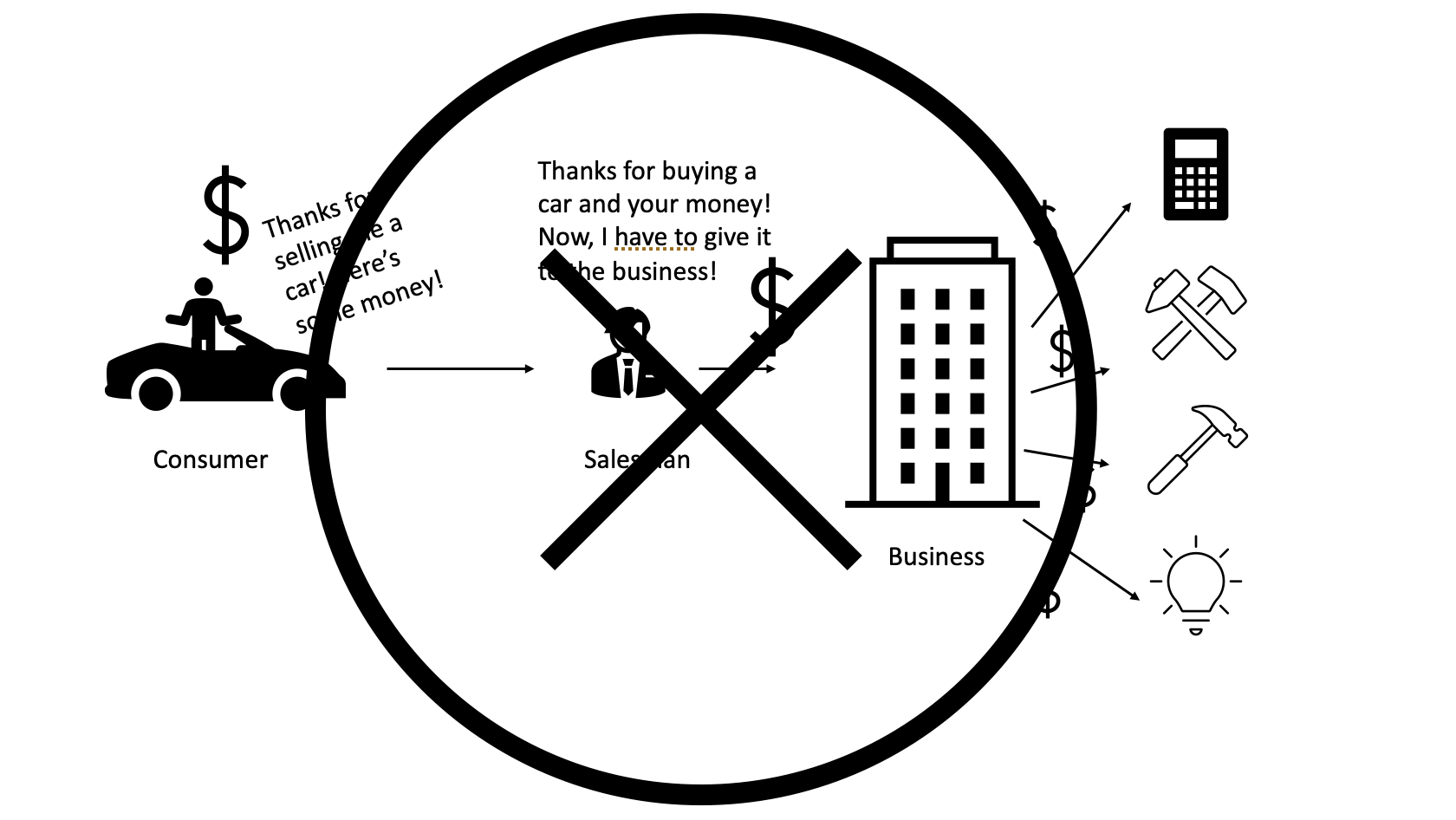

To provide a very simple example, let’s say we have to buy a car. The car we want is priced at $50,000, but we only have $10,000 to put toward a car. The accessibility of credit facilitates the transaction as we’re able to finance $40,000 of it. In turn, the banks will collect interest where they will profit off lending us money and we will work (produce) to pay that money back.

But, a couple other things happen at the same time. When we’re able to purchase that car, the salesman makes a commission. Also, the service representatives now have a car to service and the parts department also has a car to provide parts for. It doesn’t stop there, that same money goes into paying electric bills, cleaning bills, property taxes, an accounting department, etc. Essentially, the availability of credit to enable that transaction provided jobs and the ability to pay for various other services. Don’t forget that the bank profits as well, which provides more jobs, and eventually is reflected in the share price which facilitates with the expansion of the stock market.

Basically, this is one giant system and this system is called our economy. Our economy is completely run on credit and the availability of credit. Your debt and my debt is what makes this entire system function. The expansion of your debt, my debt, and more importantly the government debt expands economic activity.

Let’s focus for just a second on government debt, specifically the expansion of government debt and the COVID crisis.

In this system, there can only be so much debt that the consumer or the private enterprise can handle because we have the pay that debt back, or we’ll default. However, the government does not need to pay their debt back. They simply finance it through issuing more treasury bills, or bonds. In return, the Federal Reserve buys U.S. Treasury Bills to fund the U.S. Government debt. This is exactly what quantitative easing is and this is exactly why Jerome Powell announced he was going to buy $120B/month during the pandemic lockdowns.

The Federal Reserve owns the money supply and can print however much it wants. In theory, as long as the Fed keeps buying U.S. Treasuries, the U.S. Government will never run out of money. However, there is a consequence to expanding the money supply by buying Treasury Bills and that is inflation.

In 2021, we’ve experienced inflation like we haven’t had for a long time. Current CPI data suggests that we’ve experienced 5.4% inflation on a year over year basis. This is a direct result to the government stimulus and asset purchases by the Fed, which leads us to interest rates.

How the Federal Reserve Influences Money Supply, in Turn, Controlling Inflation

I will publish a different article that focuses predominately on how the Fed controls liquidity through its 6 mechanisms. In this article specifically, I am focusing on the Federal Funds Rate and Interest on Reserves.

Before I talk about Federal Funds Rate and Interest on Reserves, it must be known that interest rates work inversely to economic growth. Specifically when it comes to prices and employment. Essentially, as interest rates go up it becomes more difficult for consumers to borrow. This creates a cascading effect through the economy. Let’s go back to our car dealership example.

Let’s say we have two scenarios, scenario 1 we have low interest rates and scenario 2 we have high interest rates. In both examples, I still only have $10k to put down on a car but it’s $50,000. I will still have to finance the $40,000.

Scenario 1, my interest rate is 1.9%

Scenario 2, my interest rate is 4.9%

The challenge this creates is that it limits the amount I can borrow in order to not be over leveraged on a depreciating asset. If we were to break down the monthly payment of financing $40,000 with both interest rates it would look like:

Scenario 1, financing it for 60 months, my monthly payment would be $600

Scenario 2, financing it for 60 months, my monthly payment would be $753

That $153 per month is a VERY big deal for a lot of Americans. That’s $153 less to spend toward gas, insurance, or going out to eat. In addition to this, I may not even be able to purchase the car. Of which, the salesman no longer makes a commission, the services representative doesn’t have a new car to service, and it goes on and on.

More importantly, the car dealership needs to sell the car but can’t because rates are too high! So, in turn they have to lower their price which will decrease their profit and potentially lead to lay offs. This is DEFLATION.

Simply put, this contracts economic growth because I wasn’t able to get the loan (contracting credit growth) or I would have had to spend less in other areas.

The Fed controls interest rates in two ways:

Expanding money supply (liquidity)

Raising/Lowering the Federal Funds Rate

As mentioned above, I will cover later how the Fed controls liquidity and what it means for the markets. In this particular case, I will stay on topic with interest rates which is heavily influenced by the Federal Funds Rate.

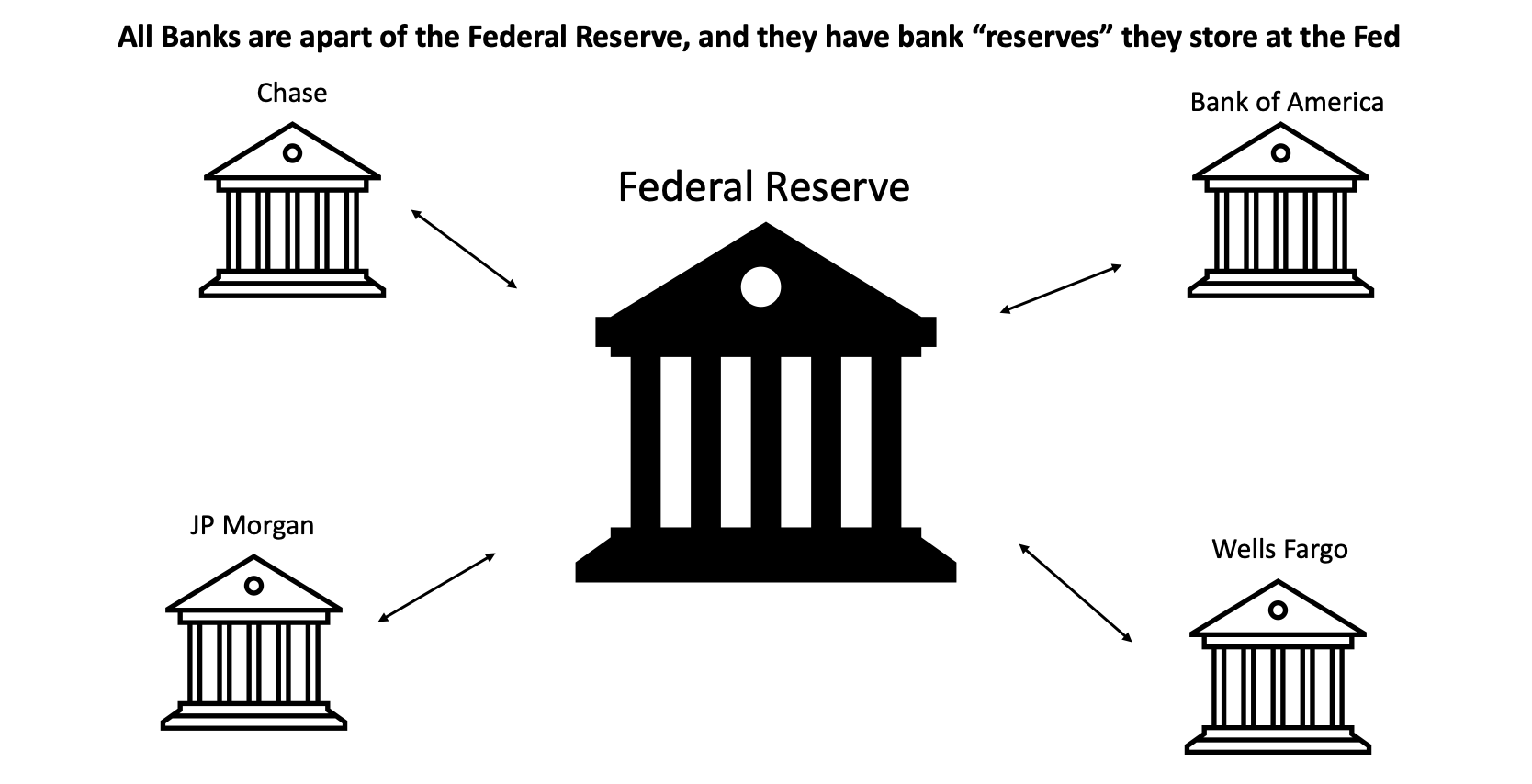

The Federal Funds Rate creates a baseline for where interest rates can be at. When we mention that the Fed is going to “hike rates” we’re directly talking about the Federal Funds Rate. This is related to the “reserves” that banks hold, or are required to hold, at the Fed. The Fed incentivizes banks to do this through paying interest on the amount of reserves they hold at the Fed.

Reserves are like a bank account of cash that banks hold at the Fed.

This interest is the Federal Funds rate.

Remember, Banks are for profit organizations. They must turn a profit and they must make money on money. The safest place they can put money to make more money (assets) is at the Fed because the Fed controls the money supply. It’s essentially a zero risk investment. Banks are incentivized by profit, they are always looking for areas to put their money to have a return on their assets and find yield.

Long story short, if the Fed increases rates this directly competes with other types of loans they would otherwise do like:

Vehicle loans - refer to our car example

Personal loans

Business loans

Home loans

These other types of loans are riskier than storing money at the Fed, therefore banks are less likely to commit to them without a certain amount of yield. They are faced with the decision to put their assets into the Fed with essentially a risk free return or commit to a riskier loan to individuals in the economy. Because they need a greater return to justify the risk they’re putting up for consumer loans, this raises interest rates.

Now That We Understand How The Federal Funds Rate Competes With Consumer/Business Loans, Let’s Bring This Back In Full Circle

Let’s recap a few key points to drive this all home.

Economic growth is directly related to credit growth. We must see credit expand to see the economy expand.

The Federal Reserve controls interest rates by raising or decreasing the Federal Funds Rate. They essentially create competition for liquidity when rates go higher. Banks want to have the best yield for the lowest possible risk. Why would they lend money to a riskier individual if they could lose it all?

Our entire economic system is no longer Capitalism but an evolved form of it through Creditism.

Creditism is only made possible by the Dollar not being backed by Gold and the Federal Reserve controlling the money supply.

Stock prices perform the best during controlled inflationary environments. They perform well because gradual, controlled, inflation means that the economy is growing. If the economy is growing that means that the GDP is growing. If the GDP is growing that means corporate earnings are growing. At the end of the day, no matter what anybody says, earnings drive stock prices because this is the real, fundamental, return investors have and can track.

If interest rates are raised, this effects stock prices two ways:

Credit contracts, which can slow economic growth. Slower economic growth means lower than expected earnings.

It creates competition for contracting liquidity (this will be focused on in the next publication) among risk vs risk-free assets. Large investors think the same thing as Banks. Why would they put $1B into a risky small cap stocks if they can just buy T-Bills for a 2.5% yield? They’re more focused on preservation of wealth rather than building more wealth.

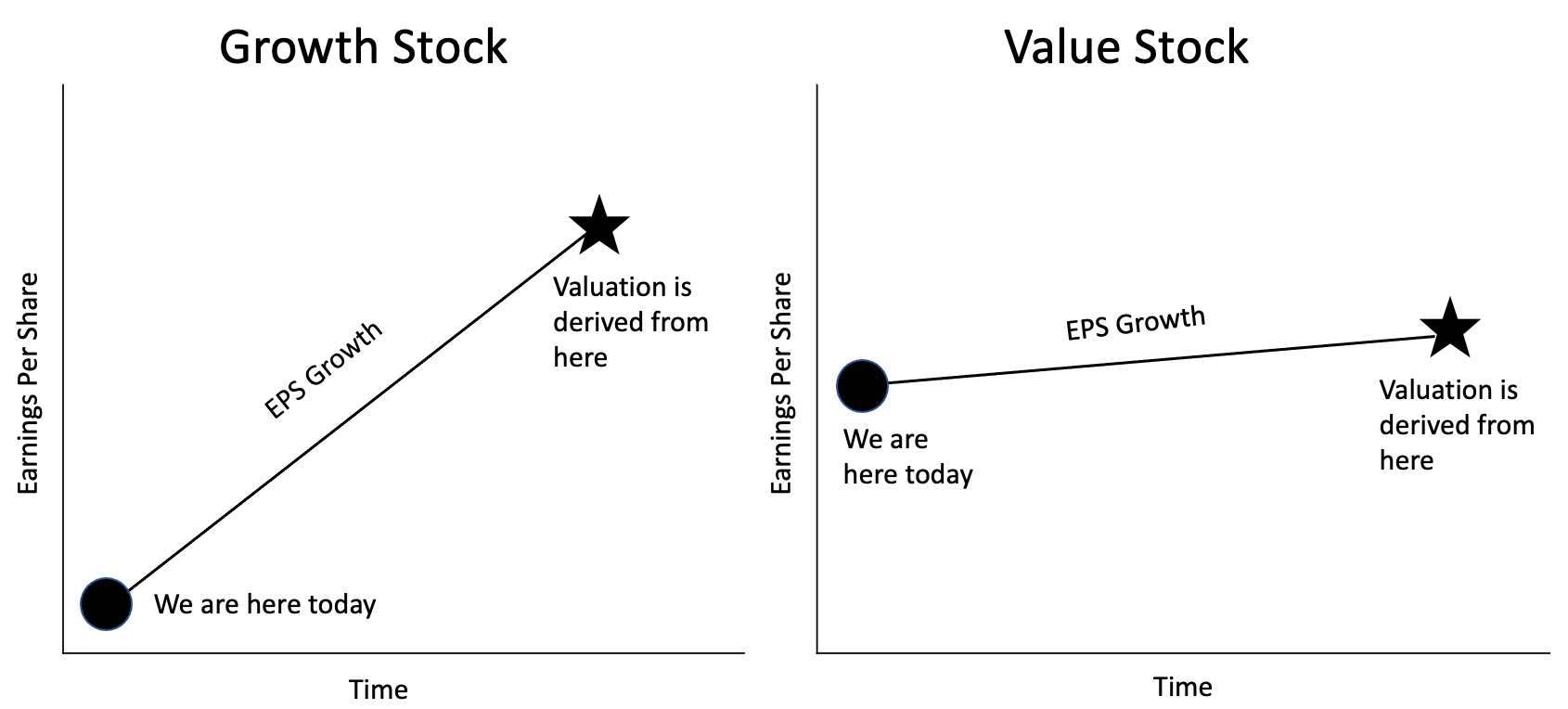

When talking specifically about growth stocks, valuations are pulled out of the future. Earnings are real returns. Every investor puts up an amount in the anticipation of earning their money back over a certain period of time.

With growth stocks specifically, because the multiple is derived from the future, interest rates drastically impact the projected multiple in the future. They especially impact the future expected earnings if the overall cost of capital drastically increases and effects the broader economic environment and expected GDP growth. Remember, Credit Growth = GDP Growth. If there’s a low cost to borrow, credit growth will continue to expand. The value stock on the other hand, with its slow earnings growth, remains relatively stable with an expected EPS return consistent. It does not need to change its future expected multiple.

Conclusion

If you found this publication helpful, I encourage you to become a member to see the next news letter which will be focused on how the Fed controls liquidity and how that plays a detrimental role in the markets as a whole. Essentially, the reason we’re able to support such high valuation in the market today is directly due to liquidity and expected liquidity in the future.

I always have so much more content planned for you guys because I love to do this. Remember, as always…

Stay tuned, stay classy,

Dillon

Well written and good analogies to help me understand. Thanks. Glad I signed up for free trial and will let renew.

Excellent article on an important subject to understand. I actually just listened to a great podcast on current macroeconomics forces and creditism for those who want to hear more. Money Tree Investing - Oct 1st Episode with Richard Duncan. It's available on Spotify. Who knows, it may be what motivated this article. Good stuff, thanks.