The Week Ahead And In Review

The Week Ahead And In Review

Catalysts, Business and Macro Data

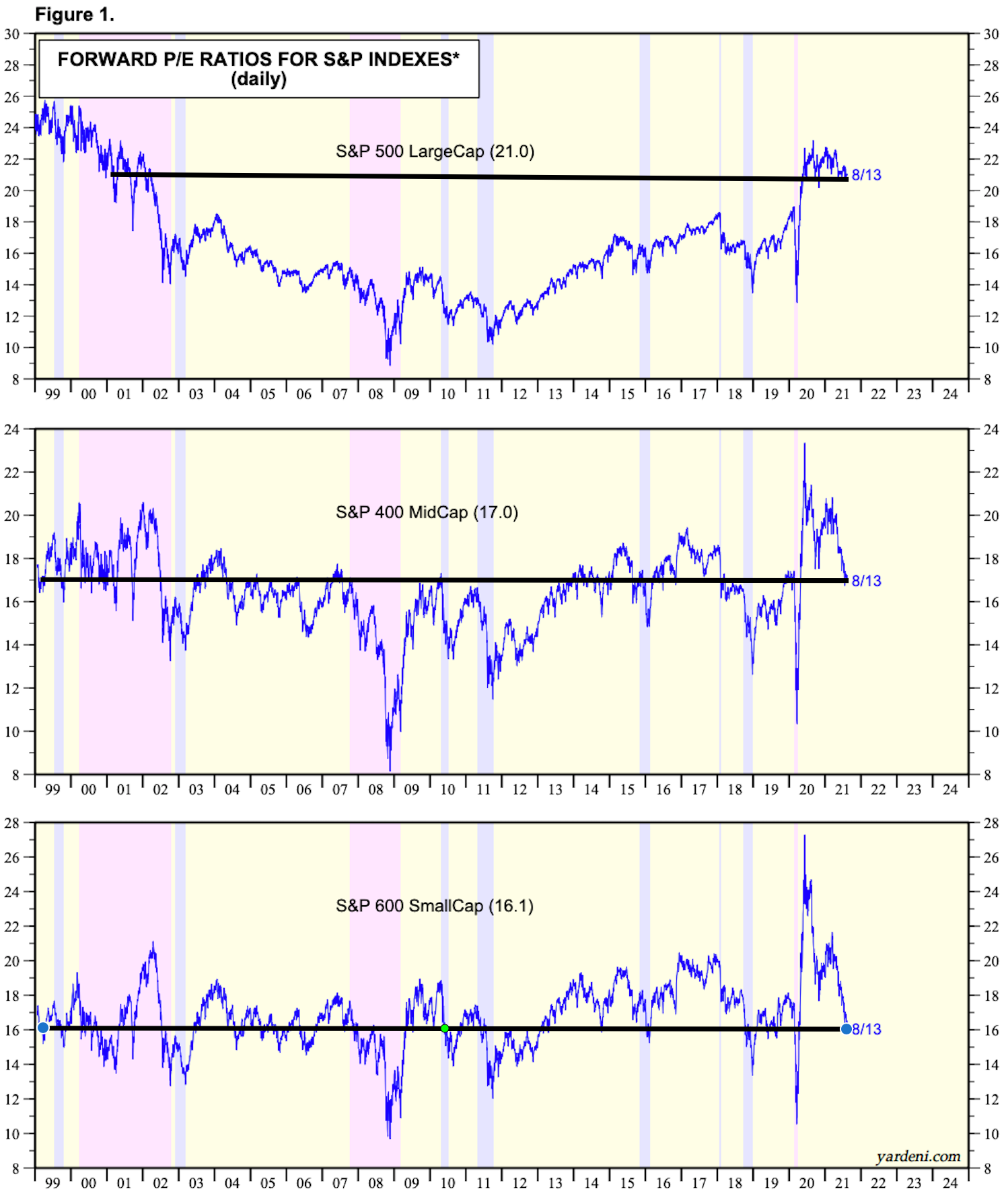

The Dispersion Between Large Cap and Small Cap

Last week was a volatile week, but I’ve become increasingly more bullish on small cap to mid caps. Retail investors seem to be beaten down and many, I’ve seen, have become fatigued and are convinced the financial markets are rigged. But I assure you, that’s not the case. However, inflation fears are real and small caps are most likely not going to catch a bid until this market cycle shifts.

The way I look at this, it’s truly just all a market cycle and this will soon end. I have to show you guys just how large this gap has come from a valuation perspective. It seems as if Wall Street wants nothing to do with small caps because of the extreme “risk off” nature.

If it looks like this isn’t right, it’s because it’s not. The valuation contraction we’ve seen in 2021 in small caps is so extreme, it’s larger than the COVID crash and the 2008 financial crisis from top to bottom. What this means is that if you started investing at the beginning of 2021, you’ve experienced a small cap bear market. Many of your favorite businesses are not bad businesses, the market has just completely disregarded small caps. However, we were in a bubble to start the year largely driven by stimulus and excessive speculative liquidity (*cough* *cough* $GME).

The take away here, there’s some serious opportunity in small cap stocks and there may be a lot of risk in large caps. I think I have mentioned this before, although not popular, where I said large caps are overvalued. It really has a lot to do with this. Can small caps fall more? Yes, they could. But, you’re absolutely right I will buy as small caps fall because that’s where the opportunity is. When the market reverses, real gains will be made.

Upcoming Earnings On I’m Paying Attention To:

Snowflake: This was the most exciting IPO of 2020 and unfortunately has not been trading at a good valuation due to the speculative euphoria that accompanied 2020. The interesting thing, this business has still performed and lived up to its expectations which is why the valuation is still so high. I think the markets this time will be less forgiving. If there is not a beat on the top and bottom line, this business can receive a hair cut from a valuation perspective. If there’s any sign of slowing growth in guidance, that will be detrimental as well. However, I am a major long term believer in this business and it has multi-bagger written all over it. Patience will be key, and this earnings will be very telling.

Revenue expectations: $256.76m

EPS expectations: -$.15

Full year revenue guidance: $1.15B

Peloton: An absolute retail favorite with a cult like following with the users and stock holders. I am not investing into PTON for the same reason I am not invested into COOK (Traeger). I love the brands, I think they’re exciting and they’re cool. However, that’s the problem, it’s cool. Cool fades and there’s no real moat with either business. PTON also heavily competes with Gym’s. The reason why I’m watching this one, I want to be proven wrong but this is the ultimate indication if the stay at home stocks were just that, stay at home. Expectations below:

Revenue: $923.52m

EPS: -$.34

Full year revenue guidance: $4.01B

A few honorable mentions with earnings this week: Salesforce (CRM), Workday (WDAY), Marvell (MRVL)

Impressive Earnings Season’s That Have Gone Unnoticed

I don’t think enough people are paying attention to three stocks that absolutely crushed earnings and made major moves this season. I think investors should review these earnings reports, as I have added these stocks due to how big of a deal what they reported was.

Zoominfo: ZI released absolutely crushing earnings and it’s important to note that by no means is this a cheap stock. However, they’re at the phase now where they’re on autopilot and should be considered in retail investing portfolios. There are a few businesses out there that can grow 50% YoY and be profitable, and expand that profitability. Especially in the SaaS space.

Revenue: $174m, beat by $11.59m up 56.9% YoY

EPS: $.14, beats by $.02

Revenue guidance: $182m - $184m up from $171.43, EPS $.11 - $.12 in line with $.12

DraftKings: People are really, really, really sleeping with this business. They’re growing the top-line exponentially but the narrative is almost always the same, “their S&M expense is too high”. The thing to know here is that it’s not like Skillz where they’re expanding investment into S&M and they’re not seeing results. This is working, very successfully and they keep raising revenue guidance. Also, by 2023 they anticipate that their investments today will be successful and they will reach profitability. Also, they acquired Golden Nugget Online Gaming. This is a BIG DEAL. The reason why, expanded demographic reach. DKNG has historically a male dominated audience which has a very niche demographic. By acquiring GNOG they can implement their successful marketing and management strategies and expand their reach into a broader iGaming market that attractions the female demographic. This expands their addressable TAM and gives them an opportunity to become the worlds dominating and premier player in iGaming and sports wagering. Also, this NFT market place is extremely interesting.

Revenue $298m, beat by $50.78m up 320% YoY

EPS miss Non-GAAP of -$.26, misses by $.18

Full year revenue guidance raise to $1.21B - $1.29B vs $1.18B

eXp World Holdings: This really isn’t well understood but it’s one of my highest conviction investments. EXPI is a real estate tech company but rather than the tech approach RedFin or Zillow take, they’re focused primarily on the broker. This is a cloud software business that provides real estate agents the infrastructure they need to enable their success and provide market leading compensation and stock incentives. In addition, they announced solutions to expand into lending and building an iBuying model where the Agent leads and provides customer service. They are focused on the Agent where the other players focus on removing the Agent. My bet is on Agents staying relevant now and in the future with many Americans largest purchase.

Revenue of $1B beats by $271.18m, 183% YoY increase

GAAP EPS of $.24 beats by $.15

$.04 dividend declared for all shareholders

Stay calm, stay tuned, and stay classy. I think the market is bound to reverse at some point.

Dillon