Quarterly Earnings are in full swing for many growth stocks including many of the stocks that I follow, closely. Some of which, I have followed for years.

This will be the first publication of a series of SubStack’s during this earnings season

What I want to do is offer the unique perspective on the business model’s I’ve followed for so long and, of course, discuss some of the financial metrics. For this one, I will keep it complimentary but for the following insights offered, I will begin to move this to exclusively for the BluSuit member community.

The two stocks covered here will be Enphase $ENPH and Digital Turbine $APPS.

Digital Turbine

I like Bill Stone, a lot, who is the CEO of this company. A short history here, Digital Turbine is actually a very old company but use to be under a different name, Mandalay. Mandalay acquired Digital Turbine in 2014, where Bill Stone was originally the CEO. However, Bill Stone eventually made his way to CEO of Mandalay and changed the name of Mandalay to Digital Turbine. Funny story, right?

They are originally a patented software that is on many, if not all, android devices. This software installs apps onto android phones and offers advertising solutions. In 2021, they acquired three different companies:

Appreciate

Fyber

AdColony

The long term vision of Digital Turbine is to become an all-in-one solution for advertisers. The make money from the time the app is installed on a mobile device and now, will also monetize the advertising revenue on that app from there. The bull case here is that they own a unique relationship with the end consumer which will help with the secular trend of privacy challenges in AdTech due to being installed directly on many Android devices.

Quarterly story updated

I’ve seen progress but I’m also seeing things I am concerned about.

In this case, Bill Stone is definitely an enthusiastic CEO and a true visionary. He often speaks intelligently about the vision long term. The problem with this is that it can often distract retail investors because it becomes difficult to see what’s truth and what’s reality. In this particular instance, I’d like to talk primarily around the number one concern I have about Digital Turbines business.

THEIR GROSS MARGIN KEEPS DECLINING

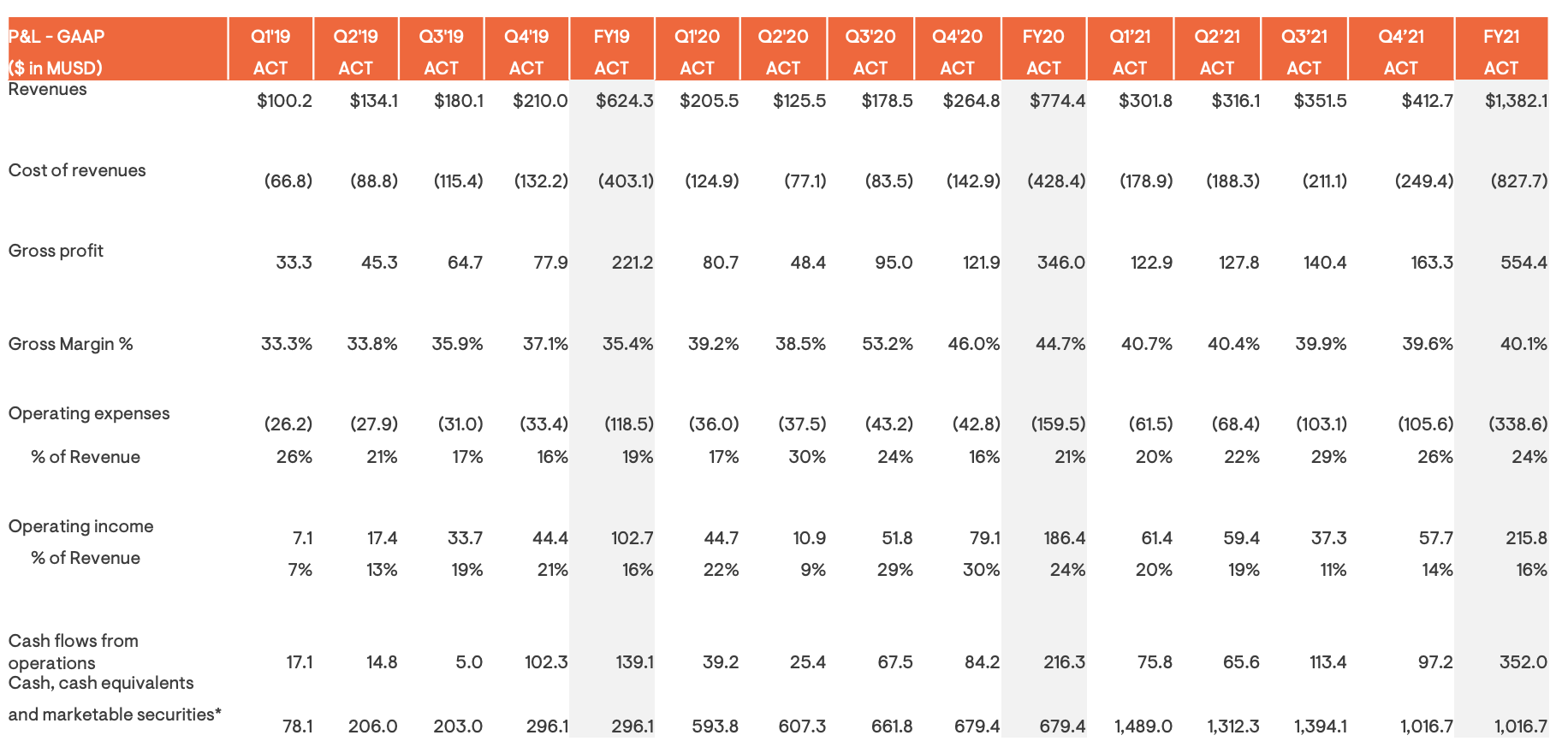

This is extremely concerning as an investor because this will hamper long term share holder returns. They are growing nicely with this latest quarter posting 38% YoY pro-forma growth. Pro-forma, in this case, is the reflection of growth in all acquired businesses into one. But, it’s becoming clear that their growth isn’t as efficient as it once was.

For the past three quarters I have seen their gross margin go from 33% to 31% and now, 27%. In their last quarter call, they mentioned they see gross margin stabilizing around 30% but this quarter it frustratingly came in lower than expected. This is telling me that something isn’t right with how they’re growing.

Debt continues to go up, this is equally or arguably more concerning

From their cash perspective, it rose (which is a good thing) to $115m from $95m last quarter. I believe their free cash flow was around $35m. But, this is over shadowed by how their long term debt once again increased to $341.59m from $244m. In addition, they mentioned that they had to expand their revolving line of credit.

I am ok with a profitable company having debt but taking out more debt and increasing their ability to borrow is a real problem. The reason why, it acts a lot like our personal financial situations. How do you feel when you have $10,000 in the bank and no debt compared to $10,000 in the bank with $1,200 in credit card debt and $30,000 in long term debt?

What this does is put pressure on business operations and restrains cash. Not necessarily what I want to see in a growth company.

Growth is projected to slow with the “long term vision” back peddled more and more

Their pro-forma revenue growth was 38%, I liked this. But, it appears that they’re suppose to see revenue growth decline this next quarter which is to be expected in what would be Q1 of most companies fiscal years. In other words, this is very normal to see in AdTech companies. But, what I’m seeing is that their vision is being pushed back.

Let me explain; the long term vision for apps is to be installed on every app and to have synergies between Digital Turbines organic software and the advertising businesses it recently acquired. However, this appears that it may take another year to actually see the results. Which, for me as an investor would normally be ok as long as I see the progress. But, currently, only 10% of their total revenue is from “synergies” (meaning how the combined businesses compliment each other). As an investor, I was hoping to see a more rapid adoption on this front and I’m thinking that they may have taken on too much too fast, which was a risk for the business.

I have exited my Digital Turbine position

The story is becoming cloudy, NOT because of poor stock price performance (I mean I still own Fubo lol) but because their financials are getting worse. In the investing world, CEO’s and management teams lie but the financials tell the truth.

Optimistically, if there’s a CEO that can pull this off long term it’s probably Bill Stone. But, the increasing pressure of the balance sheet and the rising competitive environment and, one of my favorite companies, PubMatic competing in a similar space. I think I will be comfortable watching to see how this story develops on the sidelines.

I’ll continue to follow this story but don’t feel comfortable keeping my cash in this business for now.

Enphase

This is a developing story for me. The reason why, with the price of oil and energy increasing exponentially it is becoming increasingly apparent that the cost of fossil fuel will drive an accelerated adoption of renewable energy, or solar. I have been dying for exposure to renewables and Enphase is emerging as a clear winner. Stem is also in view but this is also a developing story.

Because this is developing story, I will briefly touch up on their business model. Over time, I will be able to speak about their history and have a clear understanding of long term vision. I love what I see at first glance and their financials are stellar.

They have their own semiconductors when it comes to microinverter (a device that changes solar power to useable power). But, they’re not primarily a semiconductor play. They have their own renewable energy infrastructure. A few products they have:

Battery’s for energy storage

Semiconductors (as mentioned above)

A software platform with recurring revenue (Enphase Enlighten)

IoT devices to collect data to transmit to the cloud

Portable energy storage devices

EV Charger

Think of them as an all-in-one renewable energy company that’s focusing on the future of energy and energy management with their software. This includes solar, battery, EV, load control, and software (even an app).

I’ll write a longer, in-depth, publication at a future issue

Quarterly Results and Conference Call Highlights

On the call, it was a completely different tone than Digital Turbines. I can usually pick up when management speaks with confidence compared to trying to defend their results and not being fully transparent.

In this case, there were a few key things to touch on with various aspects of their business. These were the most impactful:

Batteries were restrained by supply chains but, they see it easing substantially

Revenue grew 55% YoY

U.S. revenue grew 74% YoY

Europe grew 100%+ YoY

Asia grew 80%+ YoY

Q1 demand, in the first few weeks, is extremely strong. Guidance is for $420 - $440m vs $410m consensus.

They plan on increasing their prices for batteries to compensate for inflation

What’s exciting is that they’re expanding services to various governments and larger organizations. A few highlights of new partnerships and clientele are:

New clientele adoption in both government and commercial enterprise in Australia

Arizona public services now a client for battery pilot grid services program

Partnership announced with Semper Solaris. Semper Solaris is a leading contractor for installation of solar and renewable energy solutions and is one of the largest in the nation.

From a trend perspective, specifically with their margins it is very positive with this latest quarter.

On a longer term basis you can notice consistent revenue growth for the past 3 years and it’s still growing. More importantly, it’s very profitable! Operating profit between 10% - 20% is very reasonable with 55% growth.

Their balance sheet is A+ as well with current assets at $1.4B and cash equivalents around $1B. Their short term debt could be paid off tomorrow if they wanted and their long term debt is more than serviceable with their current cash flow, expanding profitability, growth, demand and scale.

From a cash flow perspective, we can see:

Operating cashflow at $97m

Stock buy backs of $300m

Purchase of “marketable securities”, this is a cash equivalent as its a highly liquid asset

Free cash flow of $84m

I have entered an Enphase position with the proceeds from my Digital Turbine position

This is a no brainer. I already have exposure to AdTech with PubMatic, who I anticipate should have a good quarter (again) and arguably a better business model. In addition, I don’t have exposure to renewable energy.

Enphase is becoming a clear leader with strong financials to support their long term vision and goals. It’s very obvious there is ample demand for their semiconductor microinverter’s and heavy exposure to all renewable energy secular trends. In addition, they should gain adequate exposure to the EV boom from their latest acquisition of ClipperCreek.

I highly suggest investors consider enphase and to look into whether they fit into your portfolio long term.

Stay tuned for upcoming earnings reports!

We got DataDog, Cloudflare, Confluent, and InMode, which are top of mind, on Thursday. In addition, we have Twilio reporting tomorrow on Wednesday.

I will cover DataDog, Confluent and InMode’s earnings. I anticipate many investors will cover Cloudflare because it’s a FinTwit favorite.

Stay Tuned, Stay Classy,

Dillon

Share this post